ii. MINERAL INDUSTRIES

Iran is rich in mineral resources, but until recent times no systematic geological survey and inventory was made to determine the extent and quality of its mineral wealth. For example, the occurrence of chromite in Iran was only determined in 1940, and the enormous copper reserves at Sar-Čašma only in 1967. Although metals have been mined in Iran since prehistoric times, commercial exploitation of the known resources, which are mainly located in inaccessible locations, was discouraged by the lack of cost-effective infrastructure (good roads, ports), water and energy resources, financial resources, efficient mining and processing techniques, and adequate labor resources as well as by security considerations and the lack of a clear and pro-active government policy. As a result, Iran hardly exploited its mineral wealth, which was no major problem when Iran was still a pre-industrial society that used little metal. In fact, metal imports amounted to less than 1 percent of total imports at the end of the Qajar period indicating its relative minor role in the economy. Traditionally, some small, but rich deposits of iron, lead, copper, sulphur, and red oxide as well as some other minerals had been mined, often only intermittently. Coal only began to be mined in the 19th century, mainly to provide raw materials to modern industrial schemes (Floor, 2000, pp. 303-8; Floor, 2003, pp. 186-269; Wullf, pp. 1-17).

At the end of the Qajar period, only a few iron and copper mines were operating, while there was no Mining Law. As an essential part of Reza Shah’s (r. 1925-41) development plan, several mining operations were undertaken. He also established a Department of Industries and Mines to manage the sector and to interest national and foreign companies and individuals in the exploitation of Iran’s mineral wealth. The first Mining Act was adopted in 1938. Although individual investors operated some mines, the major operator in the sector was the State. Several coalmines were developed (including those of Šemšak, Zirāb, Dililim, Golanderud, Garjara) to supply the steel works and the modern factories that were planned. In 1947, coal production amounted to 150,000 tons per year, which were produced from small, horizontal shaft mines operated by the Industrial and Mining Bank on behalf of the State. Some 2,000 workers were employed. Because there were in most cases no roads in the mountainous areas where the mines were located, mined coal, for example, was transported in panniers on camels to the nearest motor road. This resulted in high costs and made coal mining uneconomical, the more so since cheap petroleum and fuel oil were available. The only other major mining operation was that of copper ore, of which 1,000 tons was mined per year. The ore was hand-cobbed, hand-sorted, and crushed in a jaw crusher. At the Damanqāl copper mine, which was the largest in Iran in 1947 and considered unprofitable at the time, “the smelter consists of a reverberatory oil-fired furnace capable of taking a charge of 25 tons of 7 per cent copper ore and 5 tons of limestone to produce about 2 tons of matter containing 85 per cent copper copper. Production in 1327 [1948/49] amounted to only 13 tons of copper” (Zāhedi, pp. 64-69). In addition, sulphur (600 tons), red oxide (10,000 tons), and arsenic ore (500 tons) were produced by state-owned companies. There was some production of borax for local demand, while the sodium carbonate plant at Aminābād produced 1,000 tons per year and employed 150 workers. No iron was mined in 1947; the last iron mining operation at Semnān was discontinued in 1941 (Roberts, pp. 21-22 (Overseas Consultants, Inc., IV, pp. 173-84; Gupta, pp. 31-40).

As part of its economic program, the government of Iran aimed to develop the country’s mineral wealth. To that end a Mining Act was adopted in 1952 (revised in 1957), which divided mineral resources, which are the property of the State, into three categories: (1) construction materials that the quarry owner or anyone able to get a concession from him may exploit for their personal use. In case of commercial production, a license from the government needs to be obtained; (2) metallic and non-metallic minerals and precious stones, whose exploration and exploitation were subject to greater control by the Ministry of Industry and Mines; and (3) petroleum and radioactive materials, which were the exclusive property of the State. In 1961, a Chamber of Industry and Mines was established to advise the government how to best develop the sector.

At that time only a few minerals were mined, such as antimony, arsenic, chromite, coal, iron, lead, lead-zinc, manganite, nickel, red oxide, salt, turquoise, and zinc, of which lead and zinc were the most important in monetary terms. The government owned almost 80 percent of the mines; many were closed, and others were leased to private companies. Several minerals were only exploited for export, because, apart from copper, there were no smelting or refinery facilities in Iran. However, these mines were sensitive to changes in the world market ; when prices of chromite, lead, and zinc dropped in 1960-62, their output also was decreased. In fact, many mining companies closed their mines or reduced output, and asked for government support. In 1962, of the total of 1,024 mines in operation, 690 (67 percent) were closed down. The mining companies complained about inadequate roads, transportation, and port facilities and reduced government financial assistance. Consequently, there also was a steep decline in the demand for mining permits. The result was a feeling of doom, and Echo of Iran (1963) even wrote, “Apart from oil, our mining and quarrying activities are shrinking to those of chalk, lime, and other aggregates.” However, by 1966 there was already a slight improvement to be seen. Export for some minerals rose, the number of mining licenses issued increased by 18 percent, and government financial assistance and investment rose by 85 percent and 140 percent, respectively (Echo of Iran, 1963, pp. 247-50, 560; 1965, pp. 294-96; 1966, pp. 145, 373-79).

In 1967, the Sar-Čašma copper mine was ‘discovered’ as well as many other rich deposits of important minerals (such as zinc, lead, nickel, cobalt, and tungsten), which gave a major boost to the mining sector and the government’s confidence in pursuing new options and policies. The government had invested in improvements of the port facilities of Bandar-e ʿAbbās, and it canceled all exploration agreements in that year as well as all permits for exploitation when excavation had not yet started. It was surmised that this was done to promote Iran’s industrial growth, for the government had decided to build large zinc and lead smelting plants with Russian assistance (Echo of Iran, 1968, pp. 92, 325). As a result of the improved economic conditions and a better database, foreign private investment in the mining sector increased slightly from 64 million in 1963/64 [1342] to 159 million in 1967/68 [1346], an annual increase of 17 percent. However, the same problems as before continued to constrain development in the sector (lack of government credit, experts, and road, port, and mine facilities, and a Mining Act that was confusing and did not provide sufficient incentives to the private sector). The government therefore allocated more funds in the Fourth Development Plan to develop the mining sector, in particular for copper and lead smelting plants and more exploration (Echo of Iran, 1969, pp. 248, 299, 319). Although a steel plant was built at Isfahan, there was neither coal nor iron ore in that province. Therefore, mines in Kerman province needed to be developed (see below).

In line with its general industrial policy, the government announced that smelting of iron, copper, and steel would remain a state monopoly, although the private sector was allowed to be engaged in related industries. It also took direct control of the turquoise mines at Nishapur. The government wanted to ensure that the country developed its own raw materials to meet the requirements of its expanding national industry and to reduce, if not eliminate, the import of raw materials—a policy that is still being pursued at present. To promote further mineral development, it was also announced that those who invested in mining operations would benefit from a mining tax exemption for a period of 50 years. The exemption only applied to those investing in the mining of lead, zinc, copper, and chromite at a high rate of refining; other mining activities were excluded from this exemption (Echo of Iran, 1974, p. 232). This was in line with the government’s emphasis on exports as part of its policy to diversify the economy and make it less petroleum-dominated. However, the Industrial and Mining Development Bank of Iran (IMBDI) hardly invested in the mining sector. In 1973-74, only 1.5 percent of its loans were made to mining companies and those mostly to quarrying. Of the 111 mining companies that applied for a loan that year, not a single one received a loan (Echo of Iran, 1975, p. 236).

After the Islamic revolution of 1979, most private mining and mineral processing facilities were nationalized. Production suffered due to the economic recession, followed by the outbreak of war with Iraq in September 1980. The new government nevertheless realized the importance of the minerals sector for the economy. In 1983, it revised the Mining Act, which provides for a Supreme Council of Mining to classify mines, the rate of production, employment in the mines, investment, geographical location of the mines and related socio-economic and political considerations. The law distinguishes four categories of mines: (1) construction materials; (2) metals, ornamental and precious stones; (3) petroleum; and (4) radioactive materials. Only the state is allowed to operate Category 2, 3 and 4 mines. A revision in 1985 distinguished between small and large Category 2 mines, to open the door to private sector companies. Implementation of the law is the responsibility of the Ministry of Mines and Metals, except for Category 3 mines, which are supervised by the Oil Ministry. To make investment more attractive, the Ministry provided greater facilities to the private sector for Category 2 mines, including credit. As a result, some 65 percent of these mines are operated by the private sector. Because of the shortage of Iranian geologists, the law made allowance for the recruitment of foreign experts, and for joint venture partnerships in processing projects. A new Mining Act was adopted on 17 May 1999 to attract more private participation in the mining sector by making it almost impossible to revoke licenses, by extending the license period to 25 years, and providing other incentives. The government also adopted a new Foreign Investment Promotion and Protection Act (FIPPA) that replaces the old one, which restricted direct foreign investment to joint ventures. Foreign investment contracts in the sector were based on a buy-back scheme. This means that the foreign investor is guaranteed a contractual rate of return during a fixed period after recovering the initial investment from the project’s output. Under the new law, foreign investors are allowed to make direct investments, or make a joint venture, repatriate their capital and capital gain in foreign exchange, and have their investments guaranteed by government against non-commercial risks, such as nationalization and business disruption due to new laws or regulations. New rules and special advantages were also adopted for Iran’s Free Trade-Industrial and Special Economic Zones (Šāhbahār, Qešm, Kiš; for the text of the new Mining Act and other laws see Ministry of Industries and Mines, Iranian Information Center of Industries and Mines).

The minerals sector (mining, smelting, and refining) remained under direct government control, but no longer under that of the Ministry of Industries and Mines (MIM), but under that of Mines and Metals (MMM); the petroleum industry, as before, remained under the Oil Ministry, and radioactive minerals also were controlled separately. In 2000, the government reconstituted the Ministry of Industry and Mines (MIM) by merging the MMM with the Ministry of Industry. Under the new MIM, as before under MMM, operate a number of agencies and parastatal organizations such as the Geological Survey of Iran, National Iranian Mines Metals Smelting Company, National Iranian Steel Company (NISCO), National Iranian Mining Exploration Company, National Iranian Copper Industries Company (NICICO), National Iranian Lead and Zinc Company (NILZCO), Iran Mines Export Development Company (IMEDCO), Iran General Mine Company, Iranian Aluminium Company (IRALCO), and al-Mahdi Aluminium Corporation (a joint venture). Most of the non-petroleum mineral production companies are under government control through some 30 companies administered by MMM. These include the above-mentioned parastatals as well as so-called joint-stock companies. The latter are often partially nationalized companies in which the government has a majority share. So-called private companies are of two kinds: (1) mines operated by cooperatives and foundations (bonyād), and (2) mines operated by private companies or leased to private operators. The foundations constitute the large group among these private operators. The government pursues a policy of privatizing the management of mostly smaller mines and related commercial operations, while it has so far excluded the major mining operations. The government intends to privatize 40 mineral industry companies affiliated with MIM during the Third Development Plan period, 2000-05 (1379-84).

Although the environmental effects of mining and metallurgical processing cause occupational safety and health problems, the government has ignored this fact in the past. Regular, integrated environmental impact assessments were not made. However, this is changing. The government encourages its parastatals to earn the International Organization for Standardization’s ISO 9001 quality control certificate and has prepared a pamphlet about environmental considerations of the ISO 9000 quality management standard. New investment studies therefore include environmental concerns, and new investments include environmental impact-reducing technologies.

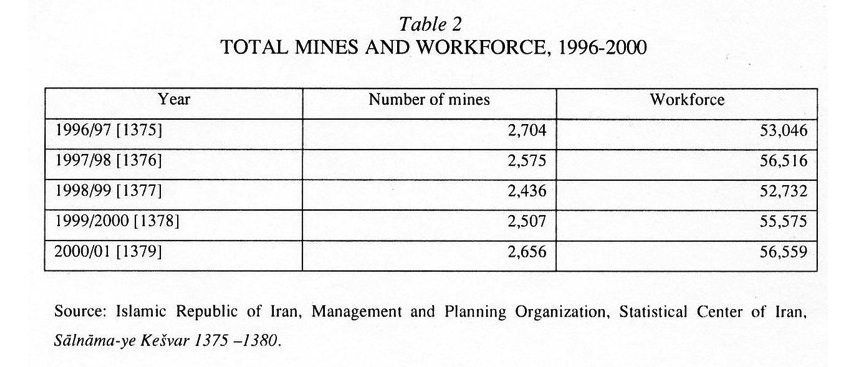

In 2001, about 56,000 people worked in 2,656 active mines producing 40 different minerals (Table 1, Table 2). The majority of mines each employed fewer than 20 persons. Only about 100 mines employ 50 persons or more. In 1999, the share of the mining sector in GNP and value added of industries and mines was 0.9 percent and 2.4 percent respectively.

{kind=link}

{kind=link}

Total mineral output increased from 800,000 tons in 1988 to 8 million tons in 1999. This trend of realizing Iran’s mineral potential by increasing output and sustaining a growing mining sector had already started in the 1970s, and after the Iran-Iraq War (1980-88) the increase of the steel and cement sector figured high in the government’s agenda as part of its postwar reconstruction and economic development program. In the next section some of the major mining and related (smelting-refining) operations are discussed. However, the petroleum sector and the steel industry are not included in this review.

Aluminum: Although Iran does not have major bauxite deposits (32 million tons) it does have vast deposits of alumite (< 687 million tons). Large deposits of nepheline also are found in Azerbaijan. Only because of Iran's cheap gas resources is the establishment of the upstream aluminum industry possible. Iran has become a aluminum/alumina-producing country. The following alumina refineries are located in Iran: Ara@k, al-Mahdi, al-GÚadir, and Qeæm. These are owned by the Iran Aluminium Company (IRALCO), which dominates the upstream aluminium industry. It is a state-owned company that was established in 1964 as a joint venture between Iran (70 percent), Pakistan (5 percent), and Reynolds Company (25 percent). The plant became operational in 1972 with a capacity of 45,000 tons, was increased to 70,000 tons later, and in 1994 to 120,000 tons per year. Australia supplied the alumina powder, which is extracted from bauxite. Output included aluminum bars, rolled bars, billets, and alloys.

The al-Mahdi Aluminum Smelter Complex at Bandar-e ʿAbbās started production in 1997 with a design capacity 110,000 tons per year, which will be upgraded to 220,000 tons per year at a later date. At the moment its output is 30,000. It is owned by the Ministry of Mines and Metals/NICICO (60 percent) and the Dubai-based International Development Corporation (40 percent). Al-Ḡadir is an aluminium smelter located in Kerman and is also owned by IRALCO. The Qešm aluminium smelter is located in the Qešm Island Free Trade Area and has a capacity of 30,000 tons per year. The Qešm smelter is owned by Prime International, a private firm. At Jajarm (150 km northeast of Šāhrud), there are deposits that contain 19 million tons with an alumina content of 41 to 69 percent. The Jajarm Alumina refinery, owned by IRALCO, was developed with Czech technical assistance and has an initial capacity of 100,000 tons per year and will later reach 280,000 tons per year. Its output serves to supply the smelters at Arāk and Bandar-e ʿAbbās.

In 2002, the expansion of the Arāk Aluminum Plant was completed. The gradual phasing out of old and outmoded equipment and machinery will take three years. This expansion is part of Iran’s intention to increase aluminum production capacity to one million tons per year during the fourth five-year development plan. To produce that amount, over two million tons of alumina powder is needed annually. Iran is currently discussing with German companies the expanding of production of the al-Mahdi Aluminium Complex from 60,000 tons to 110,000 tons annually. Meanwhile, a new contract to attract foreign investment worth 600 million dollars was signed with China. The agreement aims at the production of one million tons of aluminum ingot, 1.5 million tons of alumina powder. The company will establish a unit with the capacity of 200,000 tons of alumina, aluminum oxide in Sarāb, East Azerbaijan Province. It is also to establish another one-million-ton unit in southern Iran using imported bauxite from Guinea (BBC Monitoring Service, 21 April 21 2002).

Downstream activities are dominated by Aluminum Sazi Arak (established in 1972), which has cold and hot rolling facilities with a capacity of 15,000 tons, and Alum Pars (established in 1977) in Sāva; its cold rolling mill, which make sheets, has a capacity of 12,000 tons. There are scores of plants making intermediate and end-use aluminium products, such as items demanded by the construction, automotive, and domestic appliance industries. One of these companies is Iran Khodrow Aluminium Foundry Company (private joint-stock). It was founded on 29 August 2000 with the objective of production of aluminum vehicle parts. Another is the Iran Aluminum Industry Co., which was established in 1967. It is a leading manufacturer of aluminum proftiles, doors, windows, and curtain wall, as well as decorative fixtures in various colors and thickness. It has a total production in several plants of 3,500 tons per year with extrusion and handling, anodizing, and powder coating processes.

Chromium. The major deposits of chromite are found at Esfandaqa (south of Baft); southwest of Sabzevār; and at Faryāb (east of Bandar-e ʿAbbās; 1 million tons). The Faryab Mining and Chrome Smelting Company manages the ferrochromium smelter near Bandar-e ʿAbbās. Its capacity is 14,000 tons per year and satisfies domestic demand; the remainder is exported to Japan. The mines in the Kerman region yielded 282,000 tons of ore in 1997, half of which was consumed by the Faryab ferroalloy refinery. The construction of 18,000 tons per year chromite mine with a 25,000 tons/year ferrochrome plant at Ābada and a 25,000 tons per year ferrochrome plant at Baft are planned.

Coal. The major coalmines are Pābedana (Elburz), Bābnizu and Darra-ye Gaz (Kerman; estimated 351 million tons), Zirab (Māzandarān; 37 million tons). The Kerman and Zirāb mines supply 800,000 tons to the Isfahan steel mill. The NISCO Bābnizu and Pābedana mines near Kerman and those near Šāhrud produced about 65 percent of all coking coal in 1996; the remainder was supplied through imports. The Ṭabas underground mine with a planned capacity of 3.5 million tons per year is also a NISCO mine.

Copper. Iran’s deposits (purity rate of 0.8 Bandar-e ʿAbbās are estimated at 3 billion tons or 5 percent of the global reserves. The Sar-Čašma mine was ‘discovered’ in 1967. In 1971, an agreement were concluded to develop the mine, which is one of biggest and richest in the world, with estimated reserves of 800 million tons with a copper content of 1.12 percent, and another 400 million tons with 0.67 percent copper content. The design capacity is 144,000 tons per year also includes melting and purifying units. Its products are 24.4 percent concentrated copper, molybdenum, blister, copper anode, copper cathode and copper dust. NICICO owns the Sar-Čašma copper mine-concentrator-smelter-refinery complex. An underground copper mine and concentrator at Qalʿa-ye Zarri (150 km from Birjand) is also operated by NICICO. Its reserves are 1.8 million tons of sulfide ore with 2-4 percent copper, 2-3 grams of gold per ton of gold, and 15-20 g per ton of silver. About 30 tons per day is trucked to Sar-Čašma. The Meyduk Copper Mining Complex (130 km southwest of Sar-Čašma) is a new open-pit copper mine with reserves of 145 million tons with a copper content of 0.84 percent and has a capacity to process 5 million tons/year and 150,000 tons of concentrate (30 percent). It was developed with Finnish assistance. The Ḵātunābād smelter plant at 20 km from Sar-Čašma was built by the Chinese and will process the output of the Meyduk mine; it has a capacity of 80,000 tons per year of copper anodes at 99.4 percent copper. The Ḵātunābād smelter is owned by the National Iranian Copper Industry. The Songun Copper Complex is located in East Azerbaijan Province. The total ore reserve of this deposit is 384 million tons. However, a probable and possible reserve is one billion tons (average grade 0.67 percent). A concentrator plant with a production capacity of 150,000 tons per year with an average copper grade of 30 percent is under construction and was commissioned in early 2004.

The Shahid Bahonar [Šahid Bāhonar] Copper Complex was set up in 1980, 20 km from Kerman. It is the largest downstream copper manufacturer producing a wide range of copper products (sheets, pipes, wire, bars, strips). Its slab-billet mill has a capacity of 44,000 tons per year and its cold rolling mill 30,000 tons per year. Its cold extrusion plant has a capacity of 19,500 tons.

Gold. Iranian history is riddled with efforts to find gold, and when found invariably proved to be uneconomical or not gold at all. The Muta mine (140 km northwest of Isfahan) was first mined by traditional methods, but modern methods were employed as of 1955 till 1966, when mining was discontinued. It was resumed again in 1980. The estimated reserves are 5.1 million tons of ore of 4 g per metric ton of gold based on a cutoff grade of 1 g per metric ton. The largest deposit (Čahār–Ḵātun) accounts for half of the reserves. Mining is by open pit and the facilities were developed with Australian assistance. The Sar-Čašma precious-metals recovery plant produced 318 kg in 1994, and is expected to produce 800 kg per year and 14 tons per year of silver. There is also some gold production from placer mines in the Nishapur area. There are other gold deposits that are being explored.

Iron ore. NISCO owns and operates all iron mines and steel plants. Iron ore output continues to rise (see Table 2). Iran has four main iron mines: (1) Chadar Molu, 125 km northeast of Yazd—the physical work started in 1988, and the mine became operational in 1995; (2) Čoqart in Bāfq (200 km e. of Yazd); (3) Gol-Gowhar (55 km southwest of Sirjān); and (iv) Sangan (250 km southeast of Mashad). These mines, with combined reserves of 2 billion tons, were all developed to supply the Mobarakeh [Mobāraka] and Ahvaz Steel Complexes and other plants with iron ore (10 million tons per year) and end imports. NISCO has built an iron ore beneficiation plant at Čoqart and Seh Čāhun. The iron ore content varies from 24 to 40 percent, and the concentrate is 66 percent. Both plants will have a capacity of 3.3 million tons per year. In 1994, Čoqart supplied Isfahan Steel with 4.1 million tons per year, but the mill required 1.5 million tons per year more. NISCO therefore has expanded Čoqart’s capacity. The Gol-Gowhar mine became operational in 1994 with an initial capacity of 2.7 million tons per year that will be expanded to 5 million tons per year. The Čādar Molu mine (400 million tons reserves) became operational in 1998 with an output of 3 million tons per year. All these projects were developed with assistance from Japanese, German, and Australian companies. The biggest development project in eastern Iran was signed between Iran and Italy in March 2003. The contract, which is in the buyback and finance form, is worth 155 million US dollars and is between the Italian Consortium represented by Daniali Co. and the Iranian Power Development Company to develop and expand the Sangan open-pit mine that will have a capacity of 3.4 million tons per year. It will take three years to commission the Sangan mine, which has a reserve of 1.2 billion tons of ore with an average alloy of 60 percent and is the largest in the Middle East (Ettelaat International, 5 March 2003).

Lead and zinc. Most of Iran’s lead and zinc output comes from eight mines: Āhangarān, Angurān, Emārat, Irānkuh (Isfahan), Kušk (Yazd), Naḵlak, and Ravanj. Although the deposits are widely spread, except for the Angurān mine (southwest of Zanjān), the major mines are near Yazd and Isfahan. With the exception of Angurān, which has a 40,000-tons-per-year lead smelter, the other mines produce concentrate. The Angurān smelter produces below capacity (10,000 tons of lead bars) and is a joint venture with Calcimine. In 1997, a 60,000-tons-per-year zinc smelter became operational at Angurān. A second zinc smelter with a capacity of 28,000 tons per year was built at the Kušk mine. In 2000, the 5,000-tons-per-year Qešm zinc smelting plant became operational. It is also a joint venture with Calcimine that aims to double the plant’s capacity. Further zinc investments are planned (e.g., Mahdiābad, near Yazd).

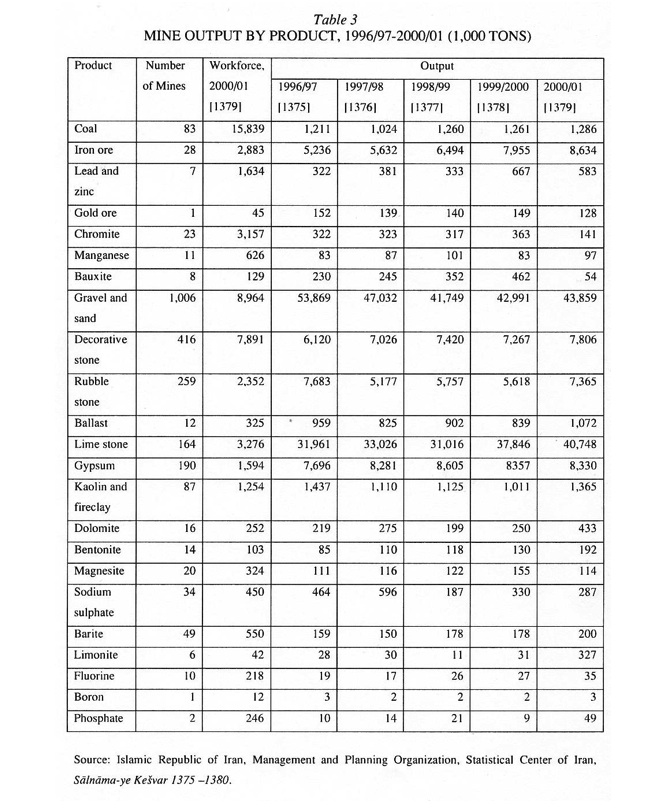

Table 3. Mine Output by Product, 1996/97‑2000/01.

{kind=link}

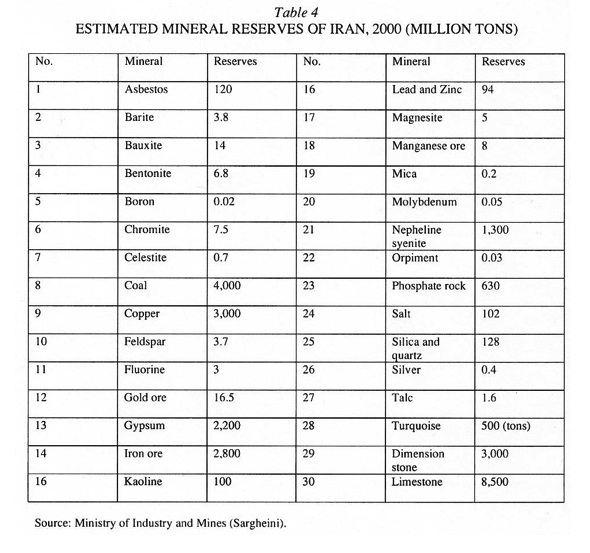

Table 4. Estimated Mineral Reserves, 2000.

{kind=link}

Bibliography:

Printed sources. Echo of Iran, Iran Almanac, Tehran, 1961-77. Eṭṭelāʿāt, 21 May 1996.

Willem Floor, The Economy of Safavid Persia, Wiesbaden, 2000.

Idem, Traditional Crafts in Qajar Iran (1800-1925), Costa Mesa, Calif., 2003.

Raj Narain Gupta, Iran. An Economic Study, New Delhi, 1947.

Iran Yearbook, Bonn, 1989-90.

Middle East Economic Digest, 17 March 1995, p. 25; 5 February 2001.

Islamic Republic of Iran, Management and Planning Organization, Statistical Centre of Iran, Statistical Pocketbook of the Islamic Republic of Iran 1380, Tehran, 2003.

Mining Annual Review, Mining Journal, 1995-99.

Overseas Consultants, Inc., Report on Seven Year Development Plan for the Plan Organization of the Imperial Government of Iran, 5 vols., New York, 1949.

N. S. Roberts, Iran. Economic and Commercial Conditions, London, 1948.

United Nations Industrial Development Organization (UNIDO), Economist Intelligence Unit, Islamic Republic of Iran. Industrial Revitalization, Vienna, 1995, pp. 157-67.

Hans E. Wulff, The Traditional Crafts of Persia. Their Development, Technology, and Influence on Eastern and Western Civilizations, Cambridge, Mass., 1966.

ʿAli Zāhedi, Ṣanāyeʿ-e Irān baʿd az jang, Tehran, 1945.

Internet resources. (Websites were accessed 18 February 2005.) Metal Bulletin (various issues), at http://www.metalbulletin.com/welcomeҳ2003.asp.

Ministry of Industries and Mines, Iranian Information Center of Industries and Mines, “Mining Act of I.R. Iran, Ratified in 1998,” at http://www.mim.gov.ir/Laws/2-1-1-e.asp.

National Geoscience Database of Iran, at http://www.ngdir.ir/Subject/Subject.asp.

On-Line ICCUM [Iran Chamber of Commerce, Industries and Mines] Publications, “Mining Sector’s Performance and New Laws,” at http://www.iccim.org/English/Magazine/iran commerce/no2 1999/12.htm.

Idem, “Mining Indices (1988-1998),” at http://www.iccim.org/English/Magazine/iran commerce/no1 2000/12.htm.

J. Sargheini, “Business Environment and Investment Opportunities in Industrial and Mineral Sectors of the Islamic Republic of Iran,”atMineral Resources Information Center, http://www.jogmec.go.jp/mric web/koenkai/030129/sargheini.pdf. (See also the various metal industry company websites.)

July 28, 2005

(Willem Floor)

Originally Published: July 20, 2005

Last Updated: July 20, 2005