TEXTILE INDUSTRY IN IRAN. Textile production in Iran dates back to the 10th millennium BCE, and much of the output of Persia’s weavers has rightly been hailed as masterworks. The first European-style factories in Persia were established in the 1850s and were among the first establishments in the country to use modern technology.

In the 19th century, much of Persia’s demand for textiles was satisfied through imports, mainly from India, which produced a large variety of cotton fabrics (see INDIA xii.). There also was some import of broadcloth for the high-end market. Because of the wide availability of the raw materials (silk, cotton, wool, flax) in Persia, spinning, knitting, and weaving formed an almost universal occupation. However, in the course of the 19th century, most of Persia’s domestic textile industry disappeared, first slowly and later rapidly, since it could not compete with cheap Indian and European (especially British and Russian) imports (Floor, 1999, pp. 98-127; idem, 2000, pp. 254-58; idem, 2003b, pp. 357-432). To stem this onslaught, attempts were undertaken to introduce modern textile factories that would make imports superfluous. In 1850, a silk-weaving mill and a calico-weaving mill were built in Kashan and Tehran respectively; and, in 1859, a spinning mill was built in Tehran. Lacking qualified technicians and a technical infrastructure, Iran was dependent on import of these resources, which added to the investment cost. This first attempt established the pattern for the manufacturing sector of the economy, which for the next 150 years continued to be characterized by (1) import substitution, (2) import of technology and skilled technicians, and (3) government subsidy.

The early textile factories could not benefit from government protection, because of the Treaty of Torkmānčāy (1828). The treaty imposed a uniform import tariff of 5 percent ad valorem, thus effectively barring Iran from protecting its nascent industries through high import tariff barriers. Eventually, in the 1920s Iran negotiated new economic agreements with its trading partners, and textile manufacturing and other state enterprises immediately received government protection through tariffs and non-tariff barriers. Whereas these early attempts were costly failures, the silk-reeling plant founded by Amin-al-Żarb in 1884 proved to be successful. Other similarly successful textile plants were a Russian-owned silk-reeling plant at Birihkadeh in Gilān which was constructed in the mid-1880s, and spinning mills erected by Ḥājj ʿAli-Naqi Kāšāni and Ḥājj Raḥim Āqā-ye Qazvini at Semnān in 1902 and at Tabriz in 1908, respectively (Floor, 2003a, pp. 17-38; idem, 2003b, pp. 391, 399).

Textile production continued to play an important role in the Persian economy, but it still remained a cottage industry despite the rapid growth of new factories in the 1930s. In 1923, Amin-al-Żarb’s old silk-reeling factory was reopened, while in 1925 the Vaṭan textile factory began production in Isfahan. Between 1931 and 1938, at least 29 large-scale textile mills were funded by both the state and private capital. The center of Persia’s textile industry was Isfahan with eight mills (5,372 workers), followed by Yazd with two mills (1,074 workers) and Kerman (696 workers) and Šāhi (3,396 workers) with one mill each. Hosiery, wool-cleaning, cotton-ginning, and other textile-related industries also expanded their capacity and labor force. In the 1930s, 32 small hosiery factories (1,584 workers) and 12 small wool-cleaning factories (225 workers) were founded. Most of the cotton-ginning industry, which had already flourished at the beginning of the 20th century, was located in Khorasan, the main cotton-producing region. By 1931, Persia already had 26 textile factories, the average labor force of which consisted of 25 workers per plant. By 1940, the number of cotton-ginning plants had risen to 76 factories (1,500 workers). Private capital concentrated on the development of the textile industry. Before the launch of the First Development Plan the state-owned mills were the textile factories of Behšahr and of Qāʾem-šahr, the silk factory of Čālus, and the jute processing plant also at Qāʾem-šahr. By 1940, the modern textile factories employed a labor force of 24,500 workers, whereas twenty years earlier they had employed only 1,000 workers (Floor, 1984, p. 29, table 10). In 1948, these factories were still working. The 26 cotton-weaving and spinning mills had 188,000 spindles with an output of 10,800 tons per year. The equipment of all textile mills urgently needed repairs or replacement, and productivity was therefore low. Hosiery and cotton piece goods were imported, as well as cotton and wool yarns to be used for warps and wefts by the carpet industry (Roberts, pp. 14-15, 20-21; Zāhedi, pp. 31 ff.; Gupta, p. 74).

In 1949, the domestic output of the textile industry, more than 55 percent of which was produced by handlooms, satisfied only 40 percent of the national demand. At the same time, 30,000 handlooms could not compete with imports and were idle, thus adversely affecting the employment of around 120,000 workers. After World War II, the government realized the need to repair and renovate the old factories and to develop new textile mills. It therefore promoted both private and public investment. The mills’ production costs were high because of large overhead, lack of maintenance, deteriorated equipment, and poor management, resulting in low productivity (Roberts, p. 34; Overseas Consultants IV, pp. 134-35). Textile sales soared after 1950 due to renewed economic activity. Domestic demand was satisfied by cheap printed calico, but the upper end of the market was not. Between 1945 and 1958, consumption had doubled, while capacity had only increased by one-third. The industry, burdened with costly over-employment and inefficient production methods, could neither compete with cheap imports nor satisfy growing demand; and the cotton supply was not always sufficient. The profitability of textile production was enhanced by high prices caused by import restrictions. The availability of foreign exchange, furthermore, allowed the purchase of modern technology that contributed to greater profitability by improving labor productivity and by reducing capital requirements and cost of raw materials.

The attraction of huge profits stimulated the building of new textile plants. The government led the construction effort, and the number of plants rose between 1956-57 and 1959-60 from 13 to 52, more than doubling the labor force. Yet a small number of efficient factories coexisted with a larger number of old factories with worn-out machinery under poor management. The privately owned factories had problems competing with the newer, state-owned ones. The former had not upgraded their technology, and some had to close. Moreover, the new factories were allowed to fire redundant workers, while the old ones were not. Consequently, the new mills’ wage bill was 35-50 percent lower than that of the old ones. In 1957, however, 40 percent of the overall output was still produced by handlooms that employed about 70 percent of the industry’s workforce. Smaller companies and artisans that were not able to buy modern technology thus suffered from a profit squeeze. Lower prices lead to rising demand that in turn sustained industrial development. In 1955, there were 51 textile-producing companies, 41 of which were cotton-based. The total number of spindles was 370,000 (90 percent cotton), and there were 5,000 weaving and knitting machines (85 percent cotton). In 1959, the sector’s output was about 200 million meters, more than 60 percent of which was produced by 26 modern factories. The spinning and weaving of wool was concentrated in Isfahan and Tabriz, where mills continued to produce cheap materials for suits, blankets, and army uniforms. There was also some production of synthetic materials of cheap rayon for women’s dresses and veils, which adversely affected the sale of woven silk products. The industry continued to grow until 1961. Between 1950 and 1962 the number of spindles almost doubled, and the number of textile machines nearly tripled. In 1961, the recession caused a decline in demand, which was lower than supply; many plants were closed, and the industry asked the government to ban all textile imports. Between 1962 and 1966, the government prohibited foreign investments (U.S. Army, pp. 478-79; Agah, p. 212-13; Karshenas, pp. 121-22; Iran Almanac, 1963, pp. 236, 241-42).

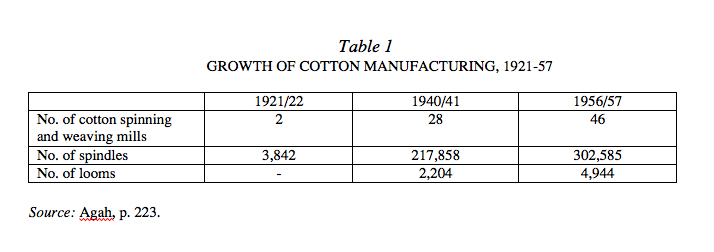

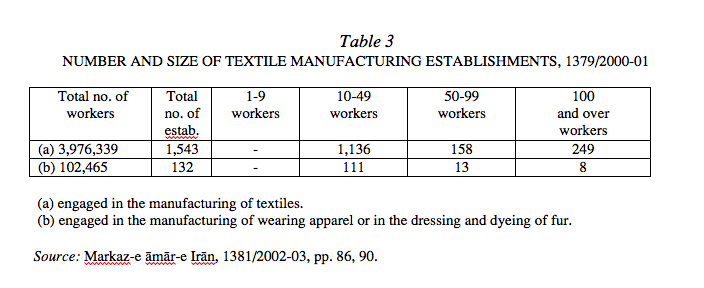

Table 1. Growth of cotton manufacturing, 1921-57.

{kind=link}

Because of its overcapacity, the industry looked for export possibilities, and in 1972 6 percent of the total output of cotton textiles were exported. The import ban was lifted in 1969, when a rise in income lead to increased demand. By 1972, spindles numbered 900,000, and weaving and knitting machines 17,000, employing 145,000 workers, effectively doubling the workforce which had been employed in 1962. The clothing industry employed 70,000 workers (Iran Almanac, 1975, pp. 329-30). In the 1970s, the overheating of the economy had a negative impact on the industry’s competitiveness. As wages rose sharply, this labor-intensive industry suffered from higher production costs. Increased domestic demand reduced the competition, which was only partially restored by the lowering of import tariffs to slow down price increases, and by the temporary lifting of import restrictions in order to address the shortage of raw materials and final products. The industry, however, continued to grow rapidly because of high domestic demand and strong state protection. In 1979, the textile industry was less competitive than in 1969 (Iran Almanac, 1972, pp. 244-45; ibid., 1976, p. 205). In 1980, the number of spindles was 1.4 million, and the number of weaving and knitting machines 35,000. This growth was quite an achievement, because the industry suffered from weak management and limited technical expertise—in short, it was resource-constrained—although it was mostly privately owned. After the Islamic Revolution of 1979 the larger plants were nationalized, and between 1980 and 1988 the government imposed a price control system upon the industry. Since all inputs were supplied at highly subsidized prices, the industry could maintain its previous output levels. During this period, the domestic textile industries were plagued by numerous problems such as ageing equipment, lack of spare parts, inability to import needed parts and raw materials, as well as labor problems. New investments were not made, and no extension plan was implement. After 1988 the price controls were relaxed, while the input subsidies were reduced, causing higher prices and a drop in output. The situation was aggravated by cheap Asian textiles, imported via the Kish Free Trade Zone, which remained competitive despite the high import tariffs.

After the Islamic Revolution and the subsequent nationalization of much of the industrial sector, there was insufficient investment due to the reluctance of private investors. Also, the government believed that the existing capacity was sufficient to meet domestic demand. Between 1980 and 1993, capacity grew. The industry totally depended on the import of machines and technology, which further constrained its development due to foreign exchange restrictions. Then the government invested in the creation of two companies to assemble spinning machines; but this decision only relocated the problem, because these assembly companies also needed foreign exchange. After more than a century, Iran’s industrialized textile production was still not competitive, although it benefited from domestically produced, cheap wool and a cheap, though poorly trained, labor force.

In the 1990s, output increased again due to a rise in income and stronger protective measures. In 1993, the number of spindles was 1.5 million, and the number of weaving and knitting machines 40,000. It has been estimated that about 420,000 workers, that is, 30 percent of the total industrial labor force, were working in the textile industry (UNIDO, 1995, p. 99). Most workers were employed in the cottage industry, which included unlicensed workshops for weaving handmade carpets and small tailor shops. The industrialized textile and garment production, with a workforce of about 150,000, was the largest industrial employer.

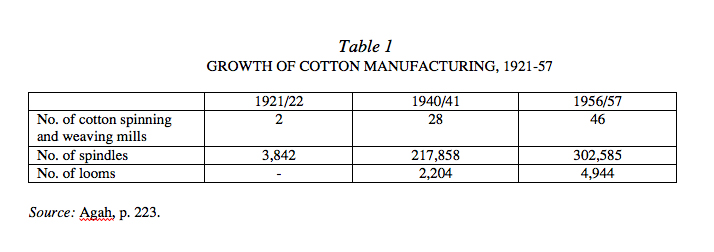

Table 2. Growth of the textile industry components, 1995-2000.

{kind=link}

The Iranian textile industry consists of companies engaged in spinning, weaving, knitting, dyeing, and printing, and of finishing plants that process yarns from natural and synthetic fibers to produce a variety of woven and knitted fabrics. The major textile items are blankets, machine-made carpets, handmade carpets, serge, as well as fabrics and garments. In 1998 and 1999, 30 blanket manufacturers produced 11,202 blankets, but their production capacity was up to 15.5 million blankets, indicating potential for export. Between 1984 and 1993, the average annual output of machine-made carpets amounted to 7.7 million m2, and that of moquettes to 22.5 million m2, much less than the demand of 122.5 million m2 estimated for the year 2000. Iran has a strong serge manufacturing industry, 21 factories of which produced 43 million m2 per year. Between 1984 and 1993, the annual production declined considerably, but efforts were undertaken to reverse this process and even to become a serge-exporting country. It has been estimated that between 1996 and 1997, about 55 million pieces of garments were produced in Iran (UNIDO, 1999, p. 90). Many workshops have official permits from the Ministry of Industry and Mines, but there are also a vast number of unlicensed workshops producing a large amount of garments. Between 1996 and 1997, Iran exported 19,312 tons of garments valued at US $210 million. Low labor costs provided a comparative advantage for this sector. Among the other textile items produced in Iran, knitwear is the most prominent and holds promise for future exports (ibid.; Internet Source 2).

The textile industry makes mostly fabrics composed entirely or partially of cotton, using domestically produced cotton. Cotton production increased until the peak year of 1975, when production reached 716,000 tons of unginned cotton. Afterwards, production declined because of government intervention and the low price the state paid for cotton. This trend was accelerated through the breakup of the large mechanized private cotton estates after 1979. Cotton production declined sharply, falling to a level as low as 204,000 tons in 1981, and forced the government to ban the export of cotton. Nonetheless, cotton production continued to decline, and Iran even had to import cotton, while the price of cotton yarn increased. However, because of corrective government measures, production has been rising since. In 1993, the price of cotton rose worldwide, encouraging further growth of production in Iran. In 1995, the output of beaten cotton rose to 150,000 tons a year, and in 1997 production reached 598,000 tons, 35,000 tons of which were exported. Recently, the export of cotton fell, and in 2002 only 3,200 tons were exported.

Iran also imports cellulose-based fibers (e.g., viscose), although there is capacity for the production of synthetic fibers. However, the petrochemical industry is not yet sufficiently well developed to sustain a downstream synthetic fiber industry. Therefore, the fiber industry remains dependent on imports, and the availability of foreign exchange constrains its development. Investment in the petrochemical industry has changed this situation through reduction of the dependence on imports of synthetic fibers. This allowed both industries to work now at much higher capacities than in the past.

Although Iran’s wool production is large, most of its output is used by the handmade carpet industry, and Iran imports wool for the manufacture of worsted wool fabrics. Iran has 102 commercial wool-spinning mills that produce 24,000 tons of wool yarn each year; its cottage industry produces an equal quantity. Handmade carpets are, next to pistachios, Iran’s most important non-oil export items. Between 1998 and 1999, Iran exported handmade carpets with a value of US $570 million. However, in recent years, Iran’s exports of hand-woven carpets have declined due to fierce competition from other countries.

Iran has a large goat population, which makes it one of the largest producers of cashmere: about 1,500 tons of a total world production of about 8,000 tons. Until recently, however, Iran did not have the proper facilities for the processing of cashmere and so exported all the soft wool in raw form. This constitutes a significant loss of income, for Iran would earn ten times more for its cashmere than it currently does by exporting dehaired cashmere (99 percent pure wool). If it were able to produce cashmere yarns, its earnings would rise another 10 percent. This amount could be doubled through the production of cashmere garments. In the last few years, investments have been made to capture this value-added. Iran Cashmere Company is the biggest Iranian cashmere scouring and dehairing company.

Jute is produced domestically. In 1947, the annual requirement was 10 million m2, 75 percent of which were needed to manufacture jute bags for rice, sugar, flour, and cement, while the remainder was used for cotton bales and the wrapping of other products. Double bag were used for export shipments, single bags for trade within the country, and second-hand bags for coarse materials, especially charcoal. Most jute was woven with a width of 140 cm, cut into pieces of 100 cm length, and then sewed into bags 70 cm wide and 100 cm long. Bags woven in Rasht weighed about 750 g each, and the ones woven in Šāhi about 800 g. Most jute was grown around Rasht, although an attempt was made to grow it around Dezful as well. There was also some import of raw jute and much woven jute fabric from India. Two jute factories were in operation. The first was a private plant in Rasht that had modern Scottish machinery with 2,100 spindles and 80 looms. It operated in two 8-hour shifts and could produce 4.5 million meters of cloth per year, using 3,000 tons of fiber. The government-owned mill at Šāhi, also equipped with modern Scottish machines, had 1,280 spindles and 60 looms, and produced 3 million meters of cloth. Both also produced 4,000 kg of string and rope. Both mills were in fair condition, but needed an overhaul. A new, privately owned small mill with 30 looms was planned at Dezful (Overseas Consultants, IV, p. 147; Gupta, p. 75). Until 1973, the jute production averaged 4,000 tons per year, enough to ensure self-sufficiency. Since 1973 production has fallen to an average of 1,000 tons per year, while demand has risen. There are four spinning and knitting units that produce jute and are more than 40 years old. They do not enjoy a favorable status from economic and industrial points of view. Their nominal capacity is 28,500 tons combined. Among other things they produce jute thread and sacks, but the raw material is imported from abroad. The domestic consumption of jute products, most of which are imported, stands at 85,000 tons per year. According to the United Nations Conference on Trade and Development (Internet Source 5), during 1996 and 1998 Iran’s average annual import amounted to 53,800 tons, which represented 5.3 percent of the total world trade in jute (Internet Source 5). As recently as in 2002, Iran protected its own jute industry against imports through import restrictions (Banerjee).

Iran also produces a considerable amount of silk, all of which is used in its carpet weaving workshops, which are mainly located in and around Qom, Isfahan, Kashan, and Nāʾin. The Čālus factory was closed in 1958. In the 1960s, it re-opened, equipped with 7,344 spindles and 220 weaving machines. In 1970, it produced more than 500,000 m of fabric, which was more than twice the domestic demand (Iran Almanac, 1970, p. 289; ibid., 1971, p. 309). In 2000, the production amounted to 800 tons. In November 2003, the only silk thread factory in Iran, in Ṣumaʿa-Sarā near Rasht, was closed down, allegedly due to illegal export of cheap silk thread. However, the factory had already been in the red for three years (Internet Source 1, item 1986415).

According to the Ministry of Industry and Mines, the total output of the Iranian textile industry (7,000 textile units) constituted 6.5 percent of the national value-added, 7.8 percent of the national industrial production, 19.3 percent of employment, and 10 percent of industrial export. In 1995 and 2000, synthetic and regenerated fibers were 1.2 and 1.5 percent of the import, respectively; all other textile products for which data are available were less than 1 percent of the total import. In 1999, some clothing (0.2 percent) was exported.

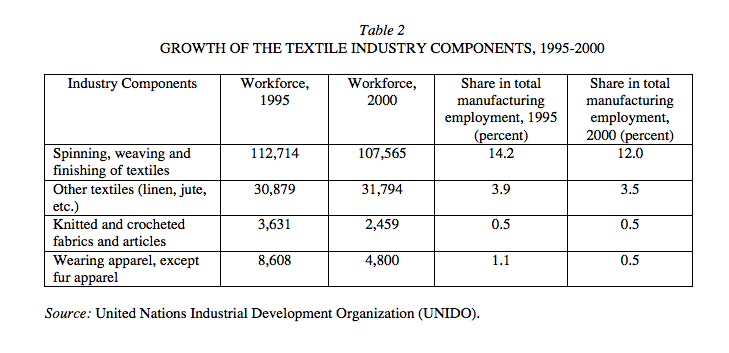

Table 3. Number and size of textile manufacturing establishments, 1379 Š./2000-01.

{kind=link}

At present, Iranian textile industries are facing numerous problems, such as lack of liquidity and lack of foreign exchange to import raw materials and spare parts; outdated and ageing machinery because of the impossibility of renovating production lines; rise in wages; and, finally, the inefficiency of the industry (Eṭṭelaat International, 19 November 1998). Not only the domestic yarns, but also those imported to satisfy domestic demand for low-priced apparel due to low purchasing power, are of low quality, so that the final product is likewise of low quality. Exporters face macroeconomic distortions, particularly in regard to foreign exchange problems and a lack of proactive and adequate government regulations (see Internet Source 1; Internet Source 3, under “Import/Export”).

In 2001, the aged state of the textile industry was even blamed for the bad results in cotton production. The same year, the government reacted by helping exporters of textiles, who received 200 billions rials in subsidies. In 2001, textile production was up by 30 percent, but exports had increased by 15 percent to a total of $220 million, and, in 2002, even by 45 percent. To redress the situation, the government hopes to modernize Iran’s textile industry through joint ventures with foreign companies in Japan, Germany, China, and South Korea, mostly through the extension of low-interest loans to the Iranian private textile companies for purchasing required equipment, raw materials, and technical expertise. The government has made available $500 million in preferential loans to modernize its aging textile industry (Iran Textile News).

In July 2002, it was announced that the 31 textile plants of the Bonyād-e Mostażʿafān would be privatized, an action which is in line with the official policy of privatizing the entire textile industry to make it more competitive on the world market. The pressure of the world market is already being felt, for in 2000 some two million meters of fabric were illegally imported into Iran. At the same time, the government continues to invest in new state-owned capacity. In August 2003, the largest textile factory in Iran was opened in Farmihan, close to Arāk, which has a production capacity of 8,000 tons per year (Internet Source 1).

See also INDUSTRIALIZATION.

Bibliography

Manuchehr Agah, “Some Aspects of Economic Development of Modern Iran,” Ph.D. diss., Oxford University, 1958.

Economist Intelligence Unit, Islamic Republic of Iran: Industrial Revitalization, London, 1995, pp. 91-106.

Willem Floor, Industrialization in Iran: 1900-1941, University of Durham, Occasional Paper 23, Durham, 1984.

Idem, Labour Unions, Law and Conditions in Iran (1900-1941), University of Durham, Occasional Paper 26, Durham, 1985.

Idem, The Persian Textile Industry in Historical Perspective: 1500-1925, Paris, 1999.

Idem, The Economy of Safavid Persia, Wiesbaden, 2000. Idem, Agriculture in Qajar Iran, Washington, D.C., 2003a, pp. 357-432.

Idem, The Traditional Crafts in Qajar Iran (1800-1925), Costa Mesa, 2003b. Iran Almanac, 1961-77, issued annually.

Raj Narain Gupta, Iran. An Economic Study, New Delhi, 1947.

Iran Yearbook, Bonn, 1989-90.

Massoud Karshenas, Oil, State and Industrialization in Iran, Cambridge, 1990.

Hans-Joachim Koellner, “Die Grundlagen der Industrialisierung Irans unter besonderer Berücksichtigung der wichtigsten iranischen Industriezweige,” Ph.D. diss., Ludwig-Maximilians-Universität München, 1949.

Markaz-e āmār-e Irān, Statistical Pocketbook of the Islamic Republic of Iran, Tehran, 1983- , issued annually. Overseas Consultants, Inc., Report on Seven Year Development Plan for the Plan Organization of the Imperial Government of Iran, 5 vols., New York, 1949.

N. S. Roberts, Iran: Economic and Commercial Conditions, Overseas Economic Surveys, London, 1948, pp. 14-15, 20-21. [UNIDO]: United Nations Industrial Development Organization, Islamic Republic of Iran: Industrial Sector Survey on the Potential for Non-Oil Manufactured Exports, 1999, pp. 85-92.

Idem, Economist Intelligence Unit, Iran, Industrial Revitalization, 1995.

U.S. Army, Area Handbook for Iran, Washington, D.C., 1964, pp. 478-79.

ʿAli Zāhedi, Ṣanāyeʿ-ye Irān baʿd az jang, Tehran, 1944.

Internet Sources.

1. Bharat Textile, current news items at:

http://www.bharattextile.com (login required)

2. Iran Industrial, company information at:

3. Iran Textile News, formerly at:

http://iran.textilenews.info

4. Mohammad Tabibian, “Manufacturing Sector’s Long Term Strategy and Development in Iran,” listed, but not currently available, at Global Development Network, as:

http://www.gdnet.org/pdf2/gdnҳlibrary/globalҳresearchҳprojects/explainingҳgrowth/Iranҳindustryҳfinal.pdf

5. UNCTAD: United Nations Conference on Trade and Development, “International Study Group on Jute and Jute Products Established,” at:

http://unctad.org/Templates/Webflyer.asp?docID=2626&intItemID=2068⟨=1

6. “Islamic Republic of Iran: Employment, Wages, and Related Indicators by Industry, at Current Prices, Selected Years,” at:

http://www.unido.org/index.php?id=4835&ucg_no64=1/data/country/stats/statablee.cfm&ShowAll=Yes&c=IRA

(Willem Floor)

July 15, 2005