BANKING in IRAN.

i. History of banking in Iran.

ii. Banking in the Islamic Republic of Iran.

Introduction. This article traces the historical development of banking in Iran, from the establishment of the first modern banks, by foreign concerns in the late 1880s, to the nationalization and consolidation of banks in 1979. It follows the growth of the banking system in the context of Iran’s economic development in the same period and attempts to highlight the role of particular banks and the evolving banking system in Iran’s economic development process, despite the theoretical debate as to the relationship of banking and economic development in general (see Basseer, 1981, pp. 1-80). (The names of Persian banks are given in their Persian form, the names of some of the major banks also in their English or anglicized form.)

Introduction of modern banking. The first modern bank to start operations in Iran was the British-owned New Oriental Bank which in 1888 opened branches and established agencies in Tehran, Mašhad, Tabrīz, Rašt, Isfahan, Shiraz, and Būšehr (Curzon, I, p. 474). The New Oriental Bank was shortly replaced by another British-owned bank, the Imperial Bank of Persia (1889), which was to remain as a major financial institution in the country for more than six decades.

Prior to the introduction of modern banks, such banking operations as extending loans, discounting and collecting bills of exchange (bījak), acceptance of deposits, and transfer of funds were carried out by reputable merchants. The major merchant-bankers of the late nineteenth century included Ḥājī Moḥammad-Ḥasan Amīn-al-Żarb, Tūmānīān Brothers, and Jahānīān Brothers (Bank Melli Iran, 1958, pp. 40-44). In addition, a number of money dealers, or ṣarrāf, lent money, mostly at 24-36 percent per annum. Among the merchant-bankers of his time, Amīn-al-Żarb was a leading businessman who operated a trading company throughout the key cities in Iran and abroad. He attempted to establish a modern bank in Iran, but as in many other instances, this indigenous effort was frustrated by the ruling Qajar shahs (Abdullaev, cited in Issawi, pp. 42-48).

Other efforts to establish a bank in Iran, notably a joint venture among English, French, Turkish, and Persian interests, namely, “Banque de Perse et d’Afghanistan” was also aborted (ibid.). However, the first bank actually to open branches in Iran was the New Oriental Bank Corporation in 1888. It operated less than two years in Iran, but was relatively successful in its short life span. It paid annual interest of 2.5 percent on current accounts and 4 percent on accounts running for more than 6 months. Its lending rates centered around 12 percent, although it charged a lower 6-8 percent to the shah (Curzon, I, p. 474). Significantly, the bank introduced a form of paper money, in the shape of cashier orders, for sums from five krans (qerān) upward, payable to the bearer, which enjoyed relative acceptance in the capital (ibid.).

However, in 1889, as a result of the grant of an exclusive bank concession by Nāṣer-al-Dīn Shah to Julius de Reuter (q.v.), the New Oriental Bank closed its operations and sold its assets for 20,000 pounds sterling to the resulting Imperial Bank of Persia (Bank Melli Iran, 1958, p. 55).

Although all indications show that the New Oriental Bank was successful in Iran, that bank did not enjoy a favorable reputation in London. Despite the fact that in 1887 the bank’s world-wide profits were 31,730 pounds sterling with equity capital of approximately 500,000 pounds sterling and paid 6 shillings dividends on 5.00 pounds sterling book value shares (Times, June 16, 1888, p. 8), it “suspended payment” in 1892 and was liquidated in 1893 (Bankers Almanac, 1974, p. 611-31).

Bānk-e Šāhī (Imperial Bank of Persia). Article 1 of the all-embracing Reuter concession (see Kazemzadeh, pp. 100-47) called for the establishment of a state bank. The bank was given the exclusive right to issue bank notes (article 3) and it was exempted from any taxation (article 5). It was also to provide the Persian government with individually negotiated loans. In return, the Persian government was assigned 6 percent of the bank’s net profits, or 4,000 pounds sterling, whichever was larger.

Initially, the nominal equity capital of the bank was set at 4 million pounds sterling, with 11 million paid in at the outset. The bank was legally formed in London, under a British royal charter of incorporation. The shares were issued on a subscription basis and, as a result of the attractiveness of the concession, within a few hours it was “subscribed fifteen times over” (Curzon, I, p. 475).

In a very short time the Imperial Bank was operational and after purchasing the branches and the goodwill of the New Oriental Bank offered a wide range of banking services. Furthermore, in 1890 the Imperial Bank introduced the first bank notes in Persia. The notes ranged from 1 toman (tūmān) to 1,000 tomans. At the outset it circulated 28,000 pounds sterling worth of notes. Within six months of its existence, the bank was able to attract double the deposits previously made with the New Oriental Bank, and by the end of 1890 these deposits reached 113,000 pounds sterling. Table 25 shows total assets and number of branches of the Imperial Bank for selected years up to 1951, the last full year of its operations in Iran.

{kind=link}

The bank’s activities were not always successful and recurrently met with commercial and public resistance. Although the merchants were previously familiar with bījaks and foreign bank notes they resisted the acceptance of the Imperial Bank notes. In Tabrīz for example, bījaks comprised 60 percent of the mode of transactions by 1919 (Bank Markazi, Bulletin 1/1, 1962, p. 1).

A major deterrent to the acceptability of the notes was the fact that they were only convertible to silver kran, in the city where they were issued. The bank, well aware of the public distrust of its notes, had adopted that policy to avoid runs in any one city. The other reason, of course, was that the bank earned substantial profits from transferring money from one city to another. In 1911 the bank charged a commission of as high as 8 percent for transferring funds from one city to another (Shuster, p. 270).

In 1899, the merchant-bankers of the time finally concerted their efforts and formed a joint company called ʿOmūmī (public) to compete with the Imperial Bank. The company was formed by 17 of the most influential of the merchants, including Tūmānīān Brothers, Ḥājī Loṭf-ʿAlī Etteḥād, Ḥājī Bāqer and the famed Malek-al-Tojjār (Issawi, p. 45). Although the company was formed with 1 million tomans (20,000 pounds sterling) capital, and had the support of the public, it could not compete with the larger resources of the Imperial Bank. The latter not only drove ʿOmūmī bankrupt, but proceeded to drive a number of the top merchant-bankers, notably the Tūmānīān Brothers, out of business (Bank Melli Iran, 1958, pp. 40-45).

In 1892, the Imperial Bank extended the first major foreign loan to the government of Iran, for 500,000 pounds sterling at 6 percent per annum (Browne, p. 31), which added to its leverage against the Persian government. The bank, although privately owned, continued to remain as a semi-political institution. Its shareholders’ meetings were often a podium for declaring British foreign economic policy in Persia, and for interfering with internal Persian politics (see, e.g., Times, December 13, 1904, p. 15, and Times, December 14, 1905, p. 14).

The Imperial Bank tended to finance primarily business concerns linked with Britain, notably Sassoon and the Anglo-Iranian Oil Company. On the whole it adopted a policy of refraining from extending credit to Iranian nationals (Bharier, 1967, p. 297). As a state bank the Imperial Bank did very little to foster indigenous capital formation or support the Iranian currency. Between 1890 and 1904, for example, the kran devalued by more than 50 percent (Yaganegi, pp. 52-87).

With the establishment of indigenous banks starting in 1929, the Imperial Bank gradually lost two-thirds of its deposits to these banks and was replaced as the “state” bank by Bānk-e Mellī-e Īrān (see below). It remained as a profitable enterprise and paid an average dividend of 9 percent per annum of its paid-up capital. However, starting in 1948, as a result of stringent reserve and other requirements, its fortunes dwindled in Iran. In the following years it changed its name to the British Bank of Iran and the Middle East (Bānk-e Īrān o Ḵāvar-e Mīāna) and diversified its operations in the neighboring countries, while curtailing its operations in Iran.

By 1952, as a result of the Iranian strife with Britain, after having lost most of its deposits, the Imperial Bank closed its operations in Iran (Times, 1 August, 1952, p. 5). The ensuing British Bank of Iran and the Middle East resumed its activity as a joint-venture bank with majority Iranian ownership in 1959. It operated as a purely commercial bank until the revolution of 1979, when along with all other private banks it was nationalized.

Bānk-e Esteqrāżī-e Rūs (Russian loan bank) and other foreign banks. Subsequent to the Reuter bank concession, the Russian government, spearheaded by Yakov Polyakov, an entrepreneur who had extensive commercial interests in Iran, demanded, among other concessions, establishment of a Russian bank in Iran. In 1890, Polyakov received a 75-year concession to establish a loan bank, which later became variously known as Russian Loan Bank, Iranian Loan Company, Banque des Prêts, and Banque d’Escompte de Perse. Formed as a private company, the bank was capitalized with 2 million French francs, half of which were spent “on the concession” (Kazemzadeh, pp. 272-73).

By 1898, partially due to an initial lack of success as a business enterprise, the shares of the bank were formally transferred to the Russian Ministry of Finance. The management of the bank fell under the jurisdiction of the Russian embassy in Iran; and in fact the Russian commercial attaché at times acted as the formal manager of the bank (Bank Melli Iran, 1958, p. 39). In practice it operated as a branch of the Russian State Bank until 1921, when it was finally turned over to Iran by the Soviet government.

The Loan Bank acted as a quasi-commercial bank, accepting deposits and lending to merchants, officials, and the Iranian government. In its commercial activities it naturally specialized in financing trade with Russia and other East European countries. As a lender to the Iranian government, it notably undertook the 1900 loan of Rbs 2.5 million (ca. 2.3 million pounds sterling). This loan, which was to replace an existing loan from the Imperial Bank of Persia, was aimed at reducing the power of the rival British banking institution (Yaganegi, p. 25).

There are few indications whether the Russian Loan Bank was ever profitable. Its mission, although commercial in appearance, was more of a political nature. For example, it subsidized the Cossack Brigade, a mercenary force in Iran (Shuster, Persia, p. 290). On the whole, like its British competitor, it did very little to finance indigenous economic activity in Iran.

Three years after the closing of the Loan Bank the Soviet Government established the Bānk-e Īrān o Rūs, which was to remain as a small wholly foreign-owned bank, serving Iran’s bilateral trade with the Soviet Union.

The only other foreign-owned bank operating in Iran, prior to the late 1950s, was the Ottoman Bank. This British- (later French-)owned institution, which was already active in the Middle East, opened a branch in Iran in 1919 (Wilson, p. 269). Although by 1930 it had four branches in the country it remained a relatively small commercial enterprise until 1948, when it closed its Iranian branches. It returned to Iran in 1958, but only as a minority shareholder in a joint-venture bank (Bānk-e Eʿtebārāt).

The establishment of Iranian banks. One of the first items on the agenda of the first Iranian parliament (Majles) was the establishment of an indigenous national bank. The move was naturally aimed at reducing the foreign financial domination. In 1907, the Majles approved the establishment of a national bank and its charter was formally signed (Times, February 7, 1907, p. 3).

However, despite the public enthusiasm, due to the politico-economic conditions of the time, the move failed to materialize (Bank Melli Iran, 1958, p. 66). Iranian-owned banks were not formed until Reżā Shah’s reign, almost two decades later.

The first Iranian-owned bank to operate in Iran was Bānk-e Sepah, which was established in 1925. It was capitalized with the army pension fund and operated only as a semi-commercial bank. The first National Bank in Iran, Bānk-e Mellī-e Īrān, was formed on August 19, 1928, and was to become Iran’s leading bank and later among the top fifty banks in the world. It started operations with the small paid-up capital of 8 million krans (162,000 pounds sterling), wholly owned by the government of Iran. Its charter was conceived by the Majles as a profit-making joint-stock company to “deal in all monetary transactions and endeavor to promote trade, industry and agriculture” (Ministry of Finance of Iran, Announcement no. 899, August 19, 1928).

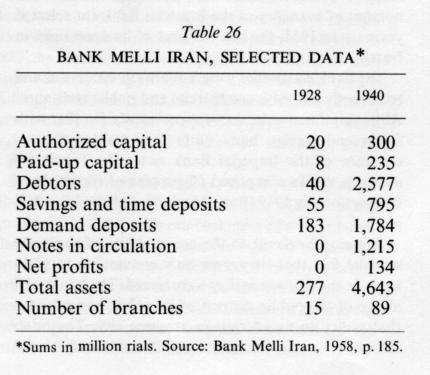

Within three years Bānk-e Mellī attracted half of the deposits in the country and embarked upon the implementation of socially desirable government policies. It was instrumental in mobilizing the monetary resources of the country during Reżā Shah’s reign. The following are some of the key financial innovations which this bank introduced in its early years of operations: (1) Branch banking. From its outset, Bānk-e Mellī adopted an expansionary policy in branch banking, opening fifteen branches in its first year of operation and reaching eighty-nine branches by 1940 (see Table 26). In contrast, the Imperial Bank never had more than twenty-five branches in Iran. Bānk-e Mellī’s branch expansion policy helped to monetize the savings of the population in a large number of provincial cities and towns. (2) National bank notes. After purchasing the bank note issuing rights from the Imperial Bank, Bānk-e Mellī adopted a uniform national bank note policy, abolishing multiple regional ones. It also reduced fund transfer charges within the country. These measures were instrumental in easing interregional trade barriers in the country. (3) Government lending. In the 1930s Bānk-e Mellī became the main source of borrowing for the public sector. It financed most of the short and medium term needs of the government for its vast developmental efforts. This policy put a limit on credits to the private sector. For example, by 1940 the total of loans to the public sector reached Rls 1,985 million, comprising more than two-thirds of the bank’s credit allocation to the nonfinancial sector (Murray, p. 271). (4) Gold standard. Bānk-e Mellī was instrumental in placing Iran’s currency on the gold standard by changing the official currency from the silver-based krans to the gold-based rials. The secular depreciation of silver prices in the world markets, plus a sharp decline following the Wall Street crash of 1929, had caused the kran to devalue along with silver, reducing Iran’s foreign exchange reserves drastically. During the period of 1928-31, the world price of silver dropped by 33 percent, which, along with the deterioration of Iran’s balance of trade, caused a 50 percent devaluation of the Iranian currency. However, the change to a dual, gold and silver, standard later contributed to maintaining Iran’s currency parity vis-à-vis European ones in the late 1930s. (5) Development banks. Bānk-e Mellī was also instrumental in starting Iran’s first two development banks in this period. Two departments of Bānk-e Mellī were expanded to become two autonomous development banks namely Bānk-e Rahnī-e Īrān (mortgage bank) and Bānk-e Kešāvarzī (agricultural bank). Although at their infancy these two special banks did not have a major impact on the agricultural sector or on the construction activity (Bharier, 1967, p. 297), a number of years later they became the leading special banks in servicing those sectors (see below).

{kind=link}

In short, Bānk-e Mellī’s policies in the 1930s laid the financial foundation for Reżā Shah’s reforms and development efforts. However, most of those development efforts were halted with the advent of war and the occupation of Iran.

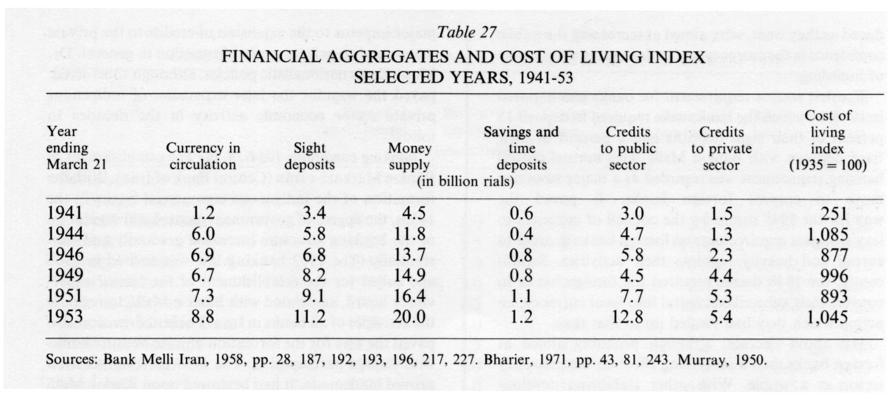

Banking conditions 1941-53. During the occupation years (1941-45), the huge Allied expenditures, the deterioration of the state’s fiscal machinery, and the lack of public confidence in the banking sector pressed the government, through the Šūrā-ye Neẓārat-e Ḏaḵīra-ye Eskenās (note reserve control board), to rely inordinately on the expansion of money supply. It was the case of a desperate government merely printing money to finance not only its own deficits, but also to provide local currency for the Allied armies’ extremely large expenditures. The public, on the other hand, tended to hoard money due to a lack of confidence in the banking sector.

In the three years 1941-44, the notes and coins in circulation increased fivefold (see Table 27). The huge infusion of currency in circulation into the money supply, however, resulted in only a 24 percent increase in sight deposits, and savings and time deposits in fact decreased by 50 percent (Table 27), reflecting substantial hoarding at that time and a lack of financial intermediation growth. The credits to the public sector, although increased, were not allocated for development purposes. The result was over 332 percent inflation in three years which, coupled with stagnant productivity, eroded much of the development achieved in the previous decades and almost destroyed the infant indigenous banks.

{kind=link}

As a direct result the rial was devalued by 50 percent in 1941, and its convertibility to precious metals was repealed in 1942. The cover of bank notes (i.e., the precious-metals backing for the issuance of currency) was reduced to 60 percent in 1941 and was maintained in that fashion until 1944.

After the occupation years a degree of normalcy prevailed and monetary order was reinstated by increasingly nationalistic governments. In late 1944 the rial cover was increased to 100 percent. Symbolically the crown jewels, the state’s collection of precious jewels, were revalued to Rls 1.7 billion and were placed with Bānk-e Mellī as a backing for the currency. The remaining cover was comprised of gold, silver, and foreign exchange (Bank Melli Iran, Bulletin, Spring, 1945, p. 10). These measures, as symbolically introduced as they were, were aimed at increasing the public confidence in the currency and at decreasing the practice of hoarding.

The first reserve requirement for banks was imposed in 1946, by which the banks were required to deposit 15 percent of their sight deposits and 6 percent of their fixed deposits with Bānk-e Mellī. This normal central banking requirement was regarded as a major sovereign move to control foreign banks. It paved the way for the 1948 decree by the council of ministers to levy stringent requirements on foreign banks in order to curtail and heavily regulate their activities. Significantly, the 1948 decree required the foreign banks to convert their subscribed capital into local currency, an action which they had evaded up to that time.

The above decrees, although probably aimed at foreign banks, had a stabilizing effect on the monetary sector as a whole. With other stabilizing developments, they caused a gradual fall in prices. The cost of living index had shown a steady decrease up to 1948, and relative stability in the succeeding years (see Table 27) despite adverse developments. The nonfinancial reasons for the deflation were the increased supply of goods after World War II and the large accumulated reserves of the government.

Nevertheless, a major disruption to the financial sector occurred subsequent to the actions of the Bank of England, which held most of Iran’s foreign exchange reserves. As a result of the nationalization of the Anglo-Iranian Oil Company, the Bank of England in 1952 imposed severe restrictions on the conversion of Iran’s sterling holdings and in essence froze the bulk of Iranian financial assets abroad (Mahdavi, pp. 441-42). This measure plus the drop in oil revenues led to an immediate devaluation of the rial.

Despite the major blow to Iran’s economic activity resulting from the drop in oil exports, the banking sector on the whole maintained relative stability. Monetary authorities and Bānk-e Mellī’s management during the Moṣaddeq period did not resort to inordinate expansion of money supply. The Banking Decree of 1948 also paved the way for the establishment of the first privately owned Iranian commercial banks.

As a result of Dr. Moṣaddeq’s nationalistic measures, both as a Majles deputy and as the prime minister, the foreign banks truncated their operations and, as noted above, the two British banks finally closed offices. The only remaining foreign bank, Bānk-e Īrān o Rūs, adopted a low profile policy, which it retained during the following decades. The decline in foreign bank activity opened the market for indigenous private banks. In 1949 Bānk-e Bāzargānī, the first indigenous private bank, was established. In 1952 five private banks (Bānk-e Pārs, Ṣāderāt, Tehrān, Bīma-ye Bāzargānān, and Aṣnāf) and one associated with the Pahlavi Foundation (Bānk-e ʿOmrān) were established. In addition, Bānk-e Mellī’s powers were expanded by the passage of Iran’s first banking law (1952), formally granting it central banking powers.

The introduction of private banks was subsequently a major impetus to the extension of credits to the private sector, and to private capital formation in general. Dr. Moṣaddeq’s nationalistic policies, although short-lived, paved the way for the later expansion of indigenous private sector economic activity in the decades to follow.

Banking conditions 1954-78. (a) The establishment of Bānk-e Markazī-e Īrān (Central Bank of Iran). With the formation of the indigenous commercial banks in the 1950s, the degree of government control and regulation of the banking structure increased gradually and substantially. The 1952 banking law was revised in 1955 and called for the establishment of the banks’ supervisory board, associated with Bānk-e Mellī, to regulate the activities of all banks in Iran. The latter revision also paved the way for the formation of joint-venture banks with foreign participation. The 1955 banking act soon proved inadequate. It had bestowed upon Bānk-e Mellī supervisory functions which at times were contradictory with its position as the largest profit-making commercial bank in the country (Bank Markazi Iran, Bulletin 2/10, 1963, p. 489). This development plus the growth of banking activity as a whole warranted the establishment of a relatively independent central bank. As a result, with the passing of the 1960 monetary and banking law, Bānk-e Markazī-e Īrān was established. Following a number of revisions and refinements in the law, notably in 1972, the Bānk-e Markazī was empowered to set monetary policy and perform all central banking functions within the framework of Iran’s overall economic policy. It was the first bank designated to compile and publish national accounting data on a systematic basis.

(b) Commercial banks. In this period commercial banks were formed mostly in two intervals, during the years 1958-59 and 1973-75. The first interval marks a period of relatively high economic growth, a surge in foreign trade and investments and a large increase (45 percent annual rate) in money supply. The years 1958-59 also mark a period of increasing westernization of the Iranian economy and the passing of the “law for the attraction and protection of foreign investments” (qānūn-e jalb o ḥemāyat-e sarmāyagoḏārī-e ḵārejī; 1959). Out of the twelve commercial banks formed in 1958-59, one was government-owned (Bānk-e Bīma-ye Īrān), and out of the remaining eleven private banks, eight were joint-venture banks with majority local and minority foreign ownership. Of the three purely private indigenous banks, Bānk-e Īrānīān later became a joint-venture bank between the American First National City Bank and local concerns (1968). In 1961, the government established Bānk-e Refāh-e Kārgarān (workers’ welfare bank).

The first joint-venture bank established in Iran was Bānk-e Eʿtebārāt-e Īrān, which was formed with the equity participation of the French Crédit Lyonnais, Crédit Industriel et Commercial, and Ottoman Bank. Of the first eight joint-venture banks two had previously operated in Iran, one as a purely indigenous bank (Bank of Tehran) and the other as a purely foreign one (Bank of Iran and the Middle East, the former Imperial Bank of Persia; see above). The total capital formation in the joint-venture banks by the end of 1959 was approximately Rls 1.6 billion ($21 million), or 60 percent of all private-bank capital in that year (see Basseer, 1982, p. 261 ). Table 28 contains a list of all commercial banks, types of ownership, dates of establishment, and key operating data (in 1976).

{kind=link}

The second interval of banking expansion was in 1973-75. With the dramatic increase in oil revenues, in this interval, the government intensified its Western-oriented economic strategy and once again launched liberalized financial and investment policies. Out of the five relatively large private banks formed in the 1973-75 interval, three were joint-venture banks. With the two exceptions cited above, all commercial banks established in the 1954-78 period were formed with majority private capital. Upon establishment the private banks, and especially the purely indigenous private banks, embarked upon a high degree of competition in opening branches and tapping the rising savings of the population. In the period 1954-78, the number of banking units (branches) in Iran grew from 285 or approximately 15 units per million of population to 7,919 or 226 per million (Bank Markazi Iran, Annual Report, 1978, p. 106). By 1978, almost all provinces in Iran were covered by the banking network. In Tehran alone there were approximately 500 banking units per million.

The largest number of banking units belonged to Bānk-e Ṣāderāt, a rapidly growing private bank, which was partially owned by its employees. By 1978, of all the banking units in existence, approximately half belonged to Bānk-e Ṣāderāt. The larger and older Bānk-e Mellī held roughly one-fifth of the banking units.

In addition to domestic branch expansion, by 1978 the larger Iranian banks had established a total of thirty-four branches and representative offices abroad (see Armfield, p. 1315). The foreign branches served to facilitate Iran’s rapidly increasing foreign trade and disbursements abroad.

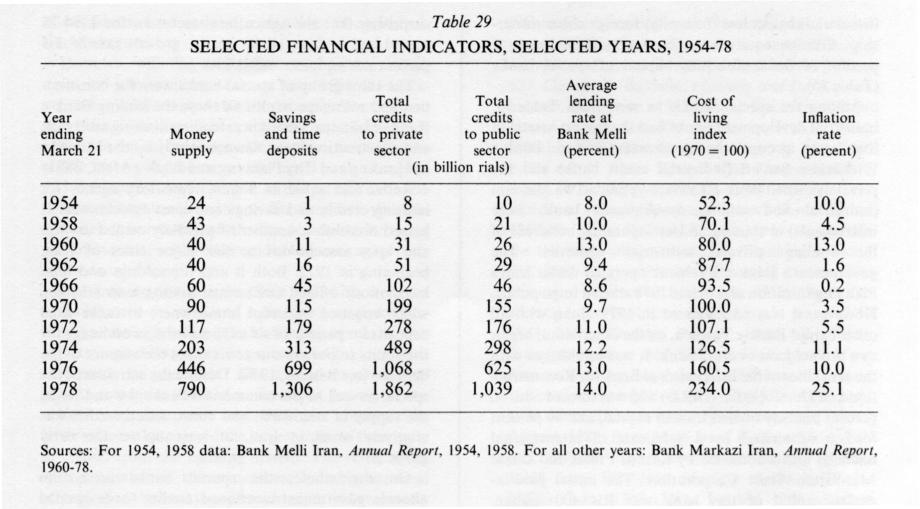

Expansion of the banking network helped to mobilize the country’s growing financial resources. The attraction of deposits by the banking sector provided a valuable pool of loanable funds to be utilized by both the private and the public sectors. The availability of credits along with the rising national income helped the enormous expansion of private sector economic activity in the 1954-78 period. The government in this period greatly encouraged the expansion of private financial intermediation. Moreover, through the regulations of the banking sector the state kept the cost of finance relatively low. In the period of 1954-78 aggregate private deposits at constant prices rose 26-fold and credits to the private sector at constant prices rose over 50-fold, outpacing by far the 19-fold estimated increase of the GNP in the 1954-78 period (see Basseer, 1982, p. 276). Table 29 shows aggregate financial data for selected years during this period.

{kind=link}

By 1978, commercial banks provided 69.9 percent of the banking credits to the private sector, the rest emanating from special banks (Bank Markazi Iran, Annual Report, p. 279). As can be seen from Table 29 the interest rates charged by commercial banks on credits to the private sectors were in the 8 to 14 percent range. Considering the rate of inflation, especially in the 1970s, the high rates of return on investments and the 20 to 26 percent interest rates in the bāzār, or the “curb market” (see Basseer, 1982, pp. 194-98), the bank lending rates were relatively low.

By and large the commercial banks provided short-term working capital financing at relatively low cost for domestic firms. They also facilitated Iran’s fast-growing domestic and foreign trade. The task of institutional financing of capital investments was largely left to the special banks.

Shortly after the fall of the shah private commercial banks along with special banks, insurance companies, and many other firms were nationalized by the revolutionary council (May 28, 1979). Only Bānk-e Īrān o Rūs was not nationalized in that year. By October, 1979, the plan for merging and consolidation of banks was approved. According to this plan the banks with similar activities were merged. Thus five new consolidated banks were created. The new banks were Bānk-e Maʿdan wa Ṣaṇʿat (industrial and mining bank), Bānk-e Maskan (housing bank), Bānk-e Kešāvarzī (agricultural bank), Bānk-e Tejārat (mercantile bank), and Bānk-e Mellat (people’s bank). Of the existing banks, Bānk-e Mellī, Bānk-e Sepah, Bānk-e Refāh-e Kārgarān, and Bānk-e Ṣāderāt continued their operations under government control (Bank Markazi Iran, Annual Report, 1980, published in 1982, pp. 81-82). Furthermore, in 1983 the law for Islamization of the banking sector and abolition of interest rates was passed (idem, 1983), setting the ground for launching of ensuing Islamic banking practices. (See also below, ii. banking in the islamic republic of iran.)

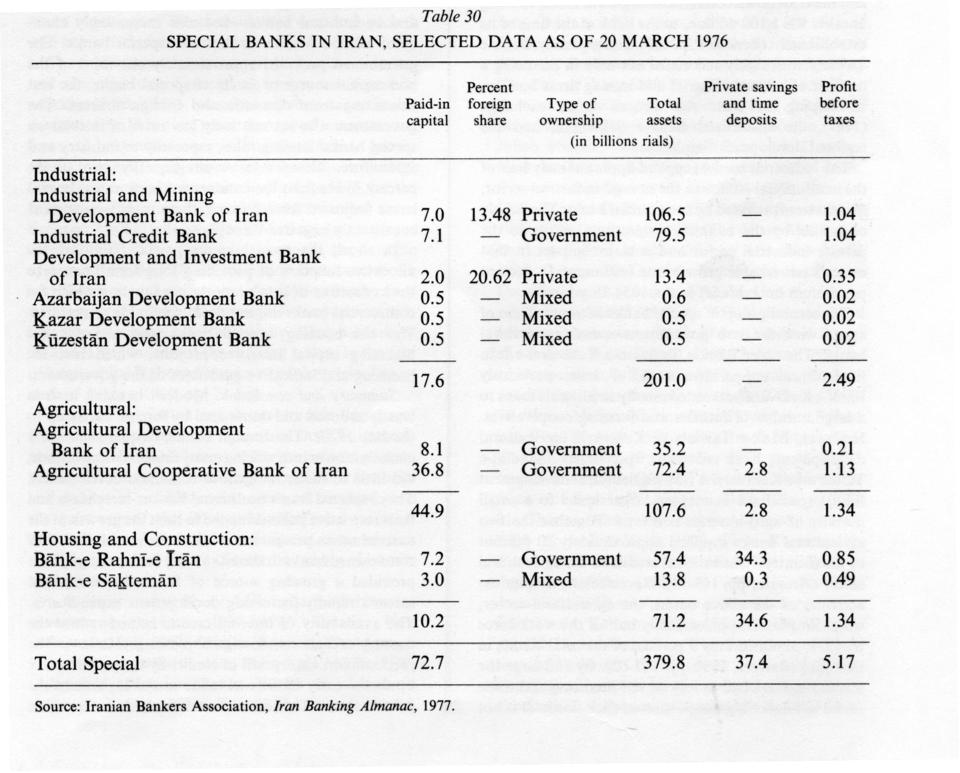

(c) Special banks. Special banks, either by law or charter, were established to supply credits for the development of specific sectors of the Iranian economy. These special or development banks were intended to extend the types of credit which the commercial banks had traditionally refrained from supplying. The areas of specialization of the development banks were industry, agriculture, and housing, which all required medium and long term credits. Table 30 shows the list of special banks by areas of specialization and indicates the dates of establishment, types of ownership, and key operating data for those banks in 1976.

{kind=link}

Of the ten special banks in existence two (industrial) banks were privately owned, four (industrial, construction) banks were mixed enterprises with majority private ownership, and the rest were government enterprises. The government special banks all originated before 1958, whereas special banks with private share capital were established after 1958, along with the aforementioned financial liberalization policy of the government. Nevertheless, by 1978 approximately 83 percent of the equity capital of special banks was owned by the government. Among the special banks only two (industrial) banks had (minority) foreign share ownership. Foreign equity investment contributed only 2 percent of the total equity capital of special banks (Table 30).

Among the special banks, as seen in Table 30, industrial development banks had the largest assets. In the latter group, the government-owned Bānk-e Eʿtebārāt-e Ṣaṇʿatī (industrial credit bank) and the privately owned Bānk-e Tawseʿa-ye Ṣaṇʿatī wa Maʿdanī (industrial and mining development bank) were instrumental in starting and/or expanding hundreds of the leading private industrial concerns. The government’s Bānk-e Eʿtebārāt operated under Iran’s Plan Organization and in late 1978 started to go public. However, it was nationalized in 1979 along with all other banks. Bānk-e Tawseʿa, on the other hand, began as a private joint-venture bank. It was established with the assistance of the International Bank for Reconstruction and Development (IBRD) and was formed with 60 percent publicly owned Iranian capital, and 40 percent foreign subscribed by a syndicate of international financial institutions, led by Lazard Frères and Chase Manhattan Trust Corporation. The initial paid-in-equity capital of this bank was Rls 400 million. However, the government of Iran along with the IBRD and the USAID all committed long-term loans, totaling another Rls 1,100 million, to the bank at the time of its establishment (Benedick, p. 120). Subsequently, Bānk-e Tawseʿa was highly successful not only in financing a number of major industrial and mining firms but also in helping to start the Tehran stock exchange (1967), the specialized Bānk-e Sāḵtemān, and the regional development banks.

The industrial banks supplied approximately half of the institutional credits to the non-oil industrial sector; the rest were provided by commercial banks. The supply of credits by the banking system as a whole to the private industrial sector had a major impact in that sector’s remarkable growth rate (estimated 11 percent per annum on average) in the 1954-78 period.

The second group of special banks in terms of size of assets were the two government-owned agricultural banks. The older Bānk-e Taʿāwon-e Kešāvarzī-e Īrān (agricultural cooperative bank of Iran, previously Bānk-e Kešāvarzī) extended mostly small-scale loans to a large number of farmers and farming cooperatives. However, Bānk-e Tawseʿa-ye Kešāvarzī (agricultural development bank of Iran, previously Ṣandūq-e Tawseʿa-ye Kešāvarzī-e Īrān [agricultural development fund]) specialized in making larger loans to a small number of agro-business concerns. Together the two agricultural banks supplied approximately 80 percent of the country’s institutional credits to the agricultural sector (Aresvik, pp. 169-74). Nevertheless, despite the activities of the above banks, the agricultural sector, which employed approximately half of the work force by 1977, obtained only 9 percent of the total credits in that year (Basseer, 1982, pp. 301-02). By and large the Iranian farmers had to rely on self-financing and trade credit to finance a great portion of their needs. It is not surprising that the agricultural sector in the 1954-78 period had a slow, albeit steady, growth rate of 2-3 percent per annum.

The third group of special banks were the construction and mortgage banks. Of these the leading Bānk-e Rahnī-e Īrān specialized in extending housing mortgage and construction loans. Owned jointly by the Ministry of Housing and City Planning and Bānk-e Mellī, Bānk-e Rahnī also acted as a state regulatory agency for housing credits and savings and loan associations. It helped establish a number of privately owned savings and loan associations in the major cities of Iran, beginning in 1972. Both it and the savings and loan associations offered contractual savings-loan schemes, which required potential homeowners to make fixed deposits for periods of six to 36 months, in exchange for the ability to borrow one to six times the amount of the deposits (see Basseer, 1974). Despite the activities of the special as well as the commercial banks, by and large, the supply of residential and construction credits was relatively small in Iran, at least up to the early 1970s.

On the whole, the special banks served to allocate government-sanctioned credits to designated sectors. The government not only allocated a part of its annual budget to special banks—particularly industrial and agricultural banks—but also increasingly channeled Bānk-e Markazī’s funds to special banks. The government provided approximately one-third of the non-capital source of funds of special banks, the rest emanating from domestic and foreign sources. The government also set relatively low rates of interest on special banks’ lending rates, especially to industry and agriculture. These rates were generally two to six percent lower than the commercial bank rates. In real terms (adjusted for inflation), these rates were almost consistently negative throughout the 1970s.

In short, the special banks partially fulfilled the allocative function of providing long-term finance to the key sectors of Iran’s economy, a function which the commercial banks did not deem profitable to perform. The non-housing special banks generally favored financing capital-intensive projects, which met the licensing and indicative guidelines of the government.

Summary and conclusion. Modern banking in Iran was introduced and dominated by foreign banks up to the late 1920s. The foreign banks, despite their early contribution in introducing many financial innovations, did little to foster indigenous economic development. They replaced Iran’s traditional banker-merchants and their restrictive policies tended to limit the growth of the nascent urban private sector. With the establishment of state-owned banks in the late 1920s, the banking system provided a growing source of funds for the public sector’s rapidly increasing development expenditures. The availability of internal credits helped reduce the country’s reliance on foreign borrowings. However, the predominant absorption of credits by the public sector up to the early 1950s was made at the expense of the private sector. The result was relatively slow expansion of private investments and a slow rate of capitalistic transformation.

However, with the establishment of private indigenous and joint-venture banks in the 1950s, the banking sector increasingly helped to monetize Iran’s growing private savings and provided a larger supply of finance capital for the private sector as well as for the public sector. Furthermore, the rental price of capital and the interest rates charged to the private entrepreneurs were kept low in real terms. The availability and the low cost of borrowing on the one hand and the rising national income on the other tended to encourage private sector economic activity.

The state, especially in the 1960s and 1970s, as a part of its Western-oriented and indicative economic planning, increasingly utilized the banking system to expand private capital formation in general and in designated enterprises in particular. The guided expansion of private enterprise resulted in the rapid growth of the urban-based mercantile and industrial sectors. The latter sectors also enjoyed the largest share of the supply of credits from the banking system. The state, along with a number of other measures, notably the land reform, used the banking system in order to break away from Iran’s pre-capitalistic economic conditions. Nourished by the vital flow of oil revenues the overall result was a rapid rate of Western-oriented economic growth and capitalistic transformation.

The rate of transformation of the Iranian economy and accompanying financial expansion was especially accelerated after 1973, when the oil revenues increased dramatically. However, when the rate of economic and financial expansion proved unsustainable, particularly in the light of stagnating oil revenues in 1978, various economic brakes were applied. In 1978, for the first time, the gross national product in real terms dropped by 8.7 percent (Bank Markazi Iran, Annual Report, 1978). Nevertheless, interestingly, the banking system during the 1978-79 revolution kept its resilience and despite many institutional disruptions for the most part operated normally. Aggregate demand and savings deposits increased dramatically. Bānk-e Markazī, by and large, bailed out the banking system in the face of huge capital flight and imminent bankruptcies (see its Annual Report, 1980, pp. 73-83).

Thus, the revolution put an end to nine decades of Western-oriented banking expansion. In 1979, immediately after the establishment of the provisional government, all banks along with a number of other financial and industrial establishments were nationalized, and the governor of the Bānk-e Markazī was executed. The nationalization and the subsequent consolidation of the banks paved the way for the launching of Islamic banking.

Bibliography:

Sharif Adib-Soltani, “Private Investments in Iran, 1937-1959,” Tehran, Plan Organization, 1962.

Oddvar Aresvik, The Agricultural Development in Iran, New York, 1976.

J. W. Armfield, “Iranian Banks Knock on London’s Door,” Banker, November, 1975.

Ahmad Ashraf, “Historical Obstacles to the Development of a Bourgeoisie in Iran,” in Studies in the Economic History of the Middle East, ed. M. A. Cook, London, 1970, p. 327.

George B. Baldwin, Planning and Development in Iran, Baltimore, 1967.

Shaul Bakhash, “Rapid Branch Expansion Continues in Iran,” World Banking XXV, The Financial Times, 19 May 1969, p. 21, col. 5.

Amin Banani, The Modernization of Iran, 1921-1941, Stanford, 1961.

Bank Markazi Iran, Annual Report and Balance Sheet, Tehran, 1960-80. Idem, Bulletin, Tehran, 1962-78 (includes the following unsigned articles: “Banking In Iran,” 1/1, 1962; “Experience in Estimating National Income and Product of Iran,” 1/4, 1962; “Some Observations on Problems of Banking in Iran,” 2/10, 1963.

Idem, Circular, Tehran, from 1961. Idem, Investors Guide to Iran, Tehran, 1966.

Idem, Monetary and Banking Act, July 1972, Tehran, 1972.

Idem, National Income of Iran, 1338-50 (1959-72), Tehran, 1975.

Idem, The Law of Usury Free Banking, Tehran, August, 1983.

Bank Melli Iran, Balance Sheet, Tehran, 1948-78.

Idem, Thirty Years History of Bank Melli Iran, 1928-1958 (Tārīḵ-e sī-sāla-ye Bānk-e Mellī-e Īrān, 1307-1337), Tehran, 1958.

Bankers Almanac and Yearbook, 1973-1974, London, 1974, p. G1131.

Potkin Basseer, The Case of Bank Rahni Iran, Tehran, 1974.

Idem, A Note on the Tehran Stock Exchange, Tehran, 1973.

Idem, The Role of Financial Intermediaries in Economic Development: The Case of Iran, 1888-1978, Doctoral dissertation, the George Washington University, 1982.

Richard E. Benedick, Industrial Finance in Iran, Boston, 1964.

Julian Bharier, “Banking and Economic Development in Iran,” Bankers Magazine, 1967. Idem, Economic Development in Iran 1900-1970, London, 1971.

Edward G. Browne, The Persian Revolution of 1905-1909, Cambridge, 1910.

The Chase Manhattan Bank, A Capital Market Study of Iran, New York, 1975.

George N. Curzon, Persia and the Persian Question, 2 vols., London, 1892.

M. Ḥejāzī, Mīhan-e mā, Tehran, 1328 Š./1949, pp. 753-57.

Industrial and Mining Development Bank of Iran, Annual Report and Balance Sheet, Tehran, 1960-77.

Idem, “Articles of Association,” Tehran, 1959.

Iranian Bankers Association, Iran Banking Almanac, Tehran, 1973-78.

“Iran: Nationalization Trend Continues,” Business Week 25, June, 1979, p. 28.

“Iran’s Miracle That Was,” Economist, 20 December 1975, pp. 68, 28-32.

Iran-U.S. Business Council, Iran-U.S. Finance Conference: A Report, Washington, D.C., 1976, pp. 119-21.

Charles Issawi, The Economic History of Iran: 1800-1914, New York, 1973.

Firuz Kazemzadeh, Russia and Britain in Persia, 1864-1914: A Study in Imperialism, New Haven, 1968.

Ḥ. Maḥbūbī Ardakānī, Tārīḵ-emoʾassasāt-e tamaddonī-e jadīd dar Īrān, 2 vols., Tehran, 2537 = 1357 Š./1978, II, index pp. 432-33.

H. Mahdavi, “The Patterns and Problems of Economic Development in Rentier States: The Case of Iran,” in H. A. Cook, ed., Studies in the Economic Development of the Middle East, London, 1970.

J. Murray, Iran Today, An Economic and Descriptive Survey, Tehran, 1950.

“Persia To Have a Bank,” New York Times, 13 October 1889, p. 11.

W. M. Shuster, The Strangling of Persia, New York, 1912.

The Statistical Center of Iran, Bayān-e āmārī, Tehran, 1977. Times (London), 16 June 1888, p. 8; 2 December 1890, p. 5; 11 December 1890, p. 11; 19 December 1906, p. 14; 7 February 1907, p. 3; 12 February 1907, p. 10; 1 January 1952, p. 3; 17 July 1952, p. 10.

A. T. Wilson, Persia, London, 1932.

Esfandiar B. Yaganegi, Recent Financial and Monetary History of Persia, New York, 1934.

(P. Basseer)

ii. In the Islamic Republic of Iran

Islamic banking is based on the principle of profit-earning on equity participation, the earning of interest (bahra) being forbidden. The merits of such a system compared to the system more common in the West (fixed interest rates and guaranteed value of deposits) is a matter of debate among economists. On the one hand, the Islamic system has certain disadvantages compared to the Western system: The equity investment principle makes Islamic banks less liquid and therefore perhaps not as flexible; the profit-sharing concept requires businessmen to share more information with banks than they may be prepared to do; banks must devote much effort to analyzing businesses because their capital is at risk; and Islamic banking is not well suited for financing consumer purchases or government deficits. For these reasons among others, pre-twentieth-century efforts to implement Islamic banking were not particularly successful.

On the other hand, some economists have argued that an equity-based system is better suited to adjust to shocks and to avoid banking crises precisely because it excludes predetermined interest rates and does not guarantee the value of deposits. Indeed, the Islamic banking system bears a striking resemblance to proposals made in the 1930s and 1940s by eminent economists for reform of the U.S. banking system (Fisher, Simons, Friedman). Furthermore, it may be suggested that Islamic banking permits the payment of a high return on capital which is economically justified in less developed countries but which would be unacceptable to regulators who set interest rates under a Western-style banking system.

On the deposit side, banks accept two basic sorts of deposits: qarż al-ḥasana and term investment deposits. In theory, the principal in qarż al-ḥasana deposits is guaranteed but the account earns no profit, while the term deposits do not have a guaranteed principal but earn profit. In practice, however, banks offer bonuses and prizes for qarż al-ḥasana savings deposits (but not for qarż al-ḥasana current deposits), and banks insure at their own expense the principal in term investment deposits (Bānk-e Markazī-e Jomhūrī-e Eslāmī-e Īrān, 1986a). Furthermore, the Bānk-e Markazī (Central Bank) sets one uniform rate which all banks pay on term investment deposits. As practiced in Iran, therefore, Islamic banking involves a guaranteed rate of return, without funds being at risk—which makes the system rather similar to Western banking.

On the lending side, the Law on Interest-Free Banking authorizes a variety of transactions, and the Central Bank closely regulates distribution of credit among the categories and by borrower type (e.g., various industries and types of agriculture). On 20 March 1986 Islamic transactions accounted for 1,833,038 million rials outstanding from the commercial banks to the private sector, while 3,005,792 million rials were outstanding to the private sector on facilities under the previous system (Bānk-e Markazī-e Jomhūrī-e Eslāmī-e Īrān, “The Practical Aspects of Islamic Commercial Banking,” paper presented at the International Islamic Banking Seminar, Tehran, 1986). On the Islamic side, the facilities and their share in the total were: 1. qarż al-ḥasana (10.9%): provision of a sum to a borrower who is to pay back the same sum at a later date; 2. civil partnership or mošāraka (13.3%): contribution of capital by several persons to a common pool on a joint-ownership basis; 3. legal partnership and direct investment (11.0%): ownership of stock in joint-stock companies or direct ownership by banks; 4. możāreba (16.0%): the bank provides the funds utilized by the borrower in trading, with profits split between the two; 5. forward delivery transactions (3.1%): advance cash purchase of products at a fixed price; 6. installment sales (of equipment or materials for production or of housing) (32.1 %): the borrower makes payments over time sufficient to allow the bank to recover the cost and to make a profit; 7. hire purchase (0.9%): the borrower leases a good owned by the bank with the stipulation that the leaseholder will ultimately receive title; 8. jeʿāla, either as ʿāmel or as jāʿel (1.3%): one party (jāʿel) pays another party (ʿāmel) to perform a service; 10. możāraʿa (not available): the bank turns land over to the borrower for a fixed period for farming in return for a specified share of the harvest; 11. mosāqā (not available): the banks turns over trees to the borrower for a specified share of the produce; 12. purchase of debt (10.2%): banks may discount debt documents and commercial papers.

In practice, the profit rate to be earned from each activity is tightly regulated by the Bānk-e Markazī, which sets minimum and maximum profit rates by industry. Furthermore, failure to repay a loan on time results in a penalty which is calculated in the same manner as interest. The Bānk-e Markazī also closely regulates the distribution of credit; for instance, the qarż al-ḥasana transactions (on which the banks make no profit) are essentially all at its direction. In sum, Islamic banking in Iran involves lending at rates that are largely set in advance, with additional payment required if funds are kept longer—which makes the system rather similar to Western banking.

To some extent, the similarities between Islamic banking in Iran and Western banking reflect the problems in the transition to the new system; e.g., personnel had to be trained in new skills and techniques, and the confidence of the public in the new system had to be ensured. Furthermore, the Islamic banking system was introduced at a difficult moment, when the banking system was suffering from bad debts extended just before the 1979 revolution and when Iran was in the midst of a deep recession.

More important, however, the characteristics of Iran’s Islamic banking system have been shaped by the need to finance a large government deficit. Islamic banking theory provides little guidance on how a government can finance its deficit. The technique used in Iran has been to require banks to lend large sums to the government, both by buying government bonds and by depositing reserves in the central bank for on-lending to the government. In the first eleven months of 1364 Š.(1985-86), these two forms of lending to the government absorbed 58% of the increase in private sector deposits (478.2 billion rials out of 827.6 billion rials; Bānk-e Markazī-e Jomhūrī-e Eslāmī-e Īrān, 1986b). In order that banks could continue to pay rates of profit sufficient to attract deposits when so much of their funds was tied up in loans to the government, the government has paid interest on its borrowing. This has been justified on the basis of a religious ruling (fatwā) that it is permissible to pay interest to oneself and that the government and the nationalized banks are all one corporate person.

Bibliography:

Bānk-e Markazī-e Jomhūrī-e Eslāmī-e Īrān, “Mobilization of Resources and Granting of Facilities,” paper presented at the International Islamic Banking Seminar, Tehran, 1986a.

Idem, “Report on the Banking System During 1363-1364,” paper presented at the International Islamic Banking Seminar, Tehran, 1986b.

R. Cooper, “A Calculator in One Hand and the Koran in the Other,” Euromoney, November, 1981.

I. Fisher, 100% Money, New Haven, 1945.

M. Friedman, “The Monetary Theory and Policy of Henry Simons,” in his The Optimum Quantity of Money and Other Essays, Chicago, 1969.

Mohsin Khan, “Islamic Interest-Free Banking,” International Monetary Fund Staff Papers 33/1, March, 1986 (this publication has an extensive bibliography on Islamic banking theory).

H. Simons, Economic Policy for a Free Society, Chicago, 1948.

(P. Clawson and W. Floor)

(P. Basseer, P. Clawson and W. Floor)

Originally Published: December 15, 1988

Last Updated: December 15, 1988

This article is available in print.

Vol. III, Fasc. 7, pp. 698-709