NATURAL GAS INDUSTRY IN IRAN: a brief history from the outset to the Islamic Revolution of 1978-79.

In this article, after a technical overview of the natural gas industry, its general scope, elements, and definitions, a brief historical background is presented on the use of natural gas (and town gas) in the world and in Iran. Then is introduced the industrial use of natural gas from the discovery of oil in Iran in 1908 until the formation of the National Iranian Gas Company (NIGC) in 1966.

The main body of the article is dedicated to the original reason behind the establishment of NIGC, that is, the Iran-USSR “Gas for Steel Mill Agreement” of 1966, and its tasks, organizational and statutory limitations, achievements, and fulfilled and unfulfilled plans and projects based on the revised fifth national development plan of 1973-77.

To this end, organizational, political, contractual, and techno-economical aspects, as well as the involved parties, are presented in some detail, so that the Iranian natural gas industry developments up to the Islamic Revolution of 1978-79 may be covered in its essential elements. Also, some complementary information on the fate of the unfinished projects conceived or started in the pre-revolution period is provided.

This entry is divided into the following six sections (for detail, see Table of Contents):

{kind=link}

|

1. |

|

|

2. |

From the outset up to construction of the first gas trunkline |

|

3. |

|

|

4. |

The gas industry in the fifth national development plan (1973-77) |

|

5. |

|

|

6. |

Natural gas production. Raw natural gas comes from three types of wells, both onshore (land) and offshore (sea): oil wells, gas wells, and condensate wells. Natural gas that comes from oil wells is typically termed associated gas. This gas can exist separately from oil in the formation (free gas) or dissolved in the crude oil (dissolved gas). Natural gas from gas and condensate wells in which there is little or no crude oil is termed ‘non-associated gas.’ Gas wells typically produce only raw natural gas. However, condensate wells produce free natural gas along with a semi-liquid hydrocarbon condensate. Whatever the source of the natural gas, once separated from crude oil (if present) or condensate, it commonly exists in mixtures with other hydrocarbons (Devold, p. 23).

Natural gas (as distinct from industrially produced gases such as oxygen, nitrogen, hydrogen, helium, etc.), as produced in the field wellhead facilities, typically is a gaseous form of petroleum consisting predominately of mixtures of hydrocarbon gases, also called ‘rich’ gas. The most common component is methane (CH4), which is desirable as a primary fuel; it also feeds some petrochemical plants, such as those for production of methanol, ammonia-urea, and gas-to-liquid [GTL] plants. Methane constitutes about 90 percent of raw natural gas molecules, depending on reservoir fluid characteristics. Other major components are heavier hydrocarbons—ethane (about 5 percent), propane (about 2 percent), butane (about 1 percent), natural gasoline (C5 and heavier)—as well as varying amounts (based on reservoir fluid properties) of inert gases (nitrogen, helium, etc.), acid gases (hydrogen sulfide [H2S], carbon dioxide [CO2]), sulfur compounds, water vapor, liquid slugs (gas bubbles embedded in liquid), and solids (Busby, Table 1.1; Manning and Thompson, pp. 5-7; GPSA, sec. 1, Definitions, pp. 1-5).

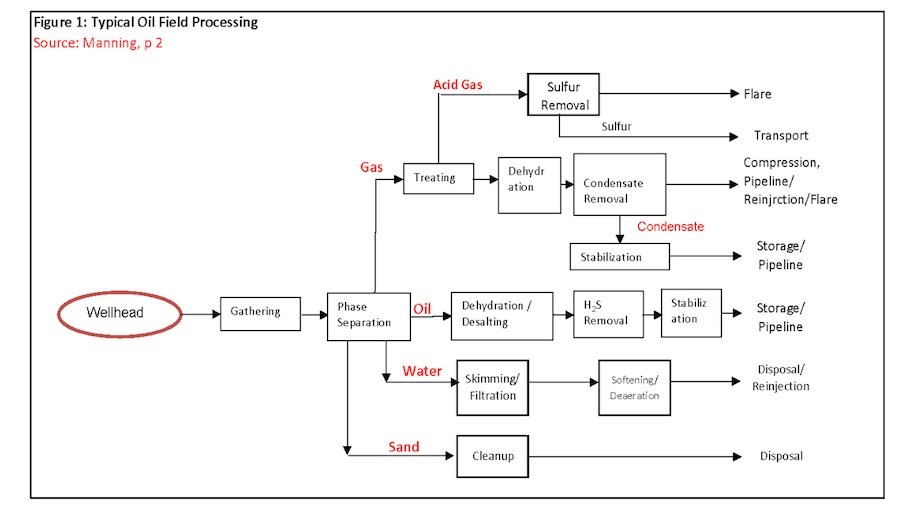

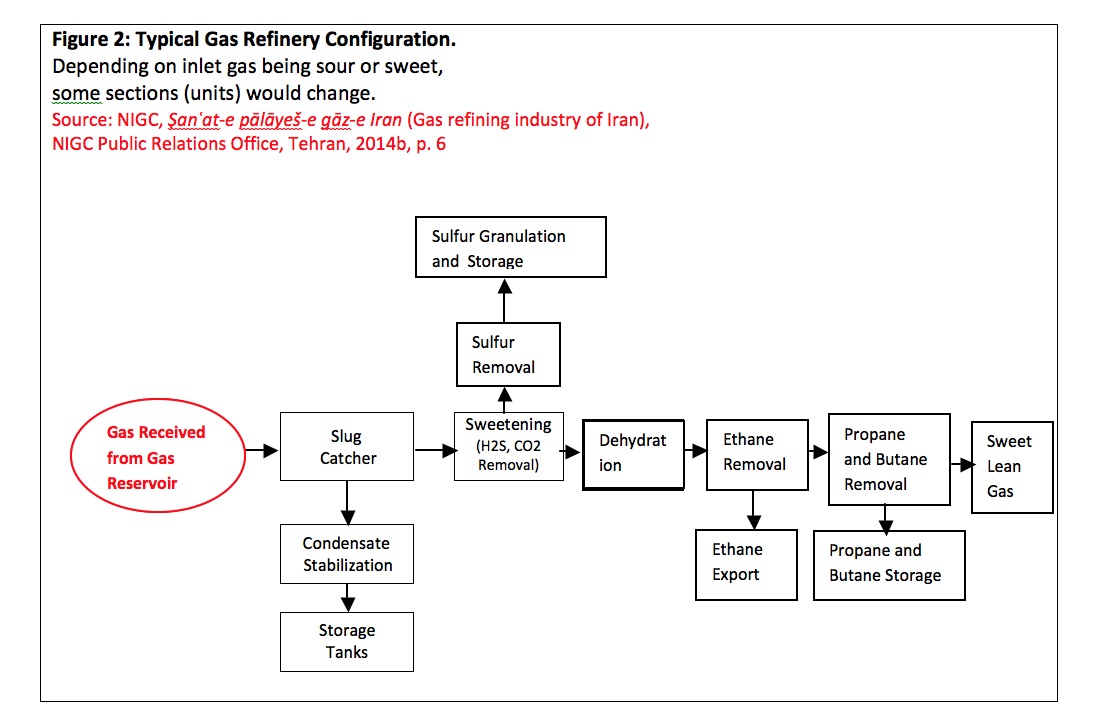

Natural gas processing. Natural gas, as it is used by consumers, is much different from the natural gas that is brought from underground up to the wellhead. While some of the needed processing can be accomplished at or near the wellhead field processing plant (such as a gas and oil/(water) separation plant [GOSP]), more complete processing of natural gas may take place at a processing plant or ‘gas refinery,’ depending on the intended products and their specifications. Such a ‘refinery’ is normally located in a natural gas-producing region (Figure 1, Figure 2).

{kind=link}

{kind=link}

Natural gas processing in a gas refinery may consist of separating all the various hydrocarbons and fluids and solids, and sweetening of ‘sour gas’ to ‘sweet gas’—that is, reducing possibly existing high mole percent acid gases H2S and CO2 and mercaptans (methanethiol compounds), which are very corrosive, to predefined acceptable levels. Thus is produced what is known as ‘pipeline quality’ ‘dry’ natural gas, also called ‘lean gas’ or ‘sales gas.’ This is in contrast to ‘rich’ or ‘wet’ gas, a term that refers to the higher content of heavier hydrocarbons that is usually condensed and separated from raw gas. ‘Wet’ gas could also mean non-dehydrated gas.

In the course of gas processing, its possibly existing undesirable contents of water vapor, H2S, CO2, mercury, nitrogen, sulfur, and oxygen are reduced to predefined, contractually specified levels. Major transportation pipelines usually impose restrictions on the make-up of the natural gas that is allowed into the pipeline. This means that, before the natural gas can be transported and priced, it must be purified, and its heating value (KJ/kg [kilo Joules per kilogram] or BTU/lb [British thermal units per pound] or BTU/ft3) must be adjusted to the required levels. Since there is a maximum ‘heating value’ and a maximum ‘dew point’ temperature at a given pressure (the latter both for hydrocarbon content and water vapor content), the heavier hydrocarbons, such as ethane, propane, butane, and pentanes, as well as water vapor, must be removed from natural gas in order to (1) meet the required heating range (e.g., 1,035 BTU/ft3 +/- 50 BTU) specification, and (2) prevent condensation of the pipeline gas, since liquid formation and freezing in low temperatures along the route can clog the line or prevent the steady flow of gas. This does not mean that separated hydrocarbons are all ‘waste products’ (Manning and Thompson pp. 14-15; EIA, 2006; NGSA, “Processing” and “History”).

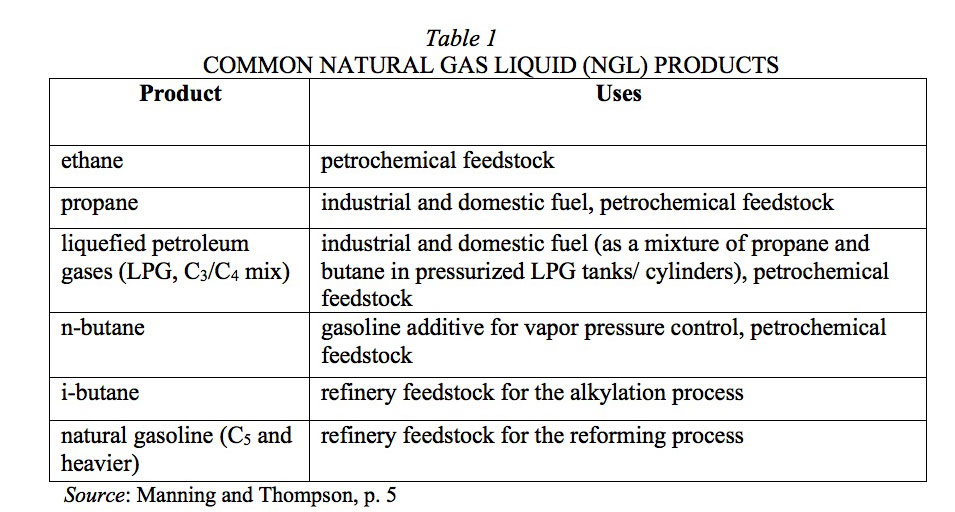

Often a portion of the heavier hydrocarbons can be profitably recovered in a field gas processing plant as one or more liquid products. These liquefiable components (or condensate/natural gas liquid [NGL]) can be recovered as a single liquid stream, which is transported to a separate plant for fractionation into salable products. Alternatively, in very large field units, fractionation is performed in the field. Common natural gas liquid (NGL) products are summarized in Table 1 (Manning and Thompson, p. 5). The reduction in volume of a gas stream by removal of some of its constituents, such as for recovered products, fuel, or losses, is called ‘gas shrinkage.’

{kind=link}

Also, natural gas itself can be liquefied to produce liquefied natural gas (LNG) in liquefaction plants to allow for transport by ocean-going vessels, whenever that is techno-economically preferable to pipeline transport, or in smaller liquefaction units for ‘peak shaving’ storage to supply natural gas during expected shortage of peak demand in cold seasons (Manning and Thompson, p. 5; Devold p. 71; USDOT, p. 1).

Natural gas storage. Apart from costly cryogenic storage (at a very low temperature of about -160 degrees C at atmospheric pressure) of liquefied natural gas (LNG), natural gas storage could be accomplished by using underground natural storage, such as in depleted gas reservoirs, and salt caverns (NGSA, “Storage”). ‘Line packing’ is another method for temporary increase of the gas storage (capacity increase) in a pipeline by maintaining a higher inlet gas pressure at the time of lower demand (Keyaerts et al., 2010). One may also mention very small storage of ‘compressed natural gas’ (CNG) in pressurized cylinders as an alternative engine fuel source for motor vehicles (Paykani).

Natural gas transportation and distribution (and re-injection). Land transportation of natural gas (as opposed to LNG sea transportation [see above]) is achieved via natural gas compressor stations feeding pressurized gas into the cross-country pipeline (trunkline) network and maintaining the required transportation pressure along the pipeline. Subsequent distribution of the gas is at reduced pressures, as fuel to the local domestic (home), commercial, and industrial users, and as both fuel and feed to some petrochemical plants. The produced natural gas could also be exported to other countries via pipeline (NGSA, “Transportation”).

Natural gas in untreated (or treated) condition may be re-injected at very high pressures, through injection wells, into an oil reservoir for ‘Enhanced Oil Recovery’ (EOR), or directly re-injected into production well casing (‘gas lift’) for facilitating oil flow (Devold, pp. 25, 35-37).

2. FROM THE OUTSET UP TO CONSTRUCTION OF THE FIRST GAS TRUNKLINE

Historical perspective. Delphi, the ancient Greek shrine of Apollo and seat of his priestess, the oracle, which existed from the late 2nd or early 1st millenium BCE, is associated with a natural gas seepage. The phenomenon is mentioned in later classical literature, described as, for example, “breath [pneuma] that inspires divine frenzy” (Strabo, 9.3.5) or “prophetic exhalation” [anaθumiasis] (Plutarch, “Obsolescence of Oracles,” sec. 41; cf. 42, 49-50). In Iran, the first discoveries of natural gas seepages must have been made between 6000 and 2000 BCE. Natural ‘eternal fires,’ which could have been fueled by natural gas escaping from cracks in the ground and being ignited by lightning, may have existed at such sites as Masjed Soleyman, Kirkuk in Iraq, and Baku in the Republic of Azerbaijan. After the Battle of Gaugamela (331 BCE), Alexander the Great, in Plutarch’s account (Alex. 35.1), was amazed by the sight of a continuous fire and a naphtha spring; this was in the general area of the Kirkuk oilfields, as he headed south to Babylon (cf. Strabo, 16.1.4: “a spring of naptha and fires”). In China, written sources from 500 BCE describe how the Chinese used natural gas to boil seawater for desalination (Encyclopedia Britannica, “Natural Gas”; NGSA, “History”; USDOE, “History”).

In 19th-century England, ‘coal gas’ was generated by heating up carbonated coal (‘town coal’) and transferring the generated gas by wooden, and later on metal, pipes to streets and homes; this was the first use of gas for lighting purposes. Nāṣer al-Din Shāh Qājār in his first journey to Europe and England (1873) was highly impressed by this new invention. After his second trip to Europe, he had his palace and one nearby Tehran street, to be called ‘Cheragh Gaz’ (Čerāḡ Gāz “Gas Light”) Street, equipped and lighted with this facility. The new, limited lighting was inaugurated in October 1881 (Maḥbubi-Ardakāni, III, pp. 382-83, cited in Floor, 2005). The system initially used heated coal gas, and some years later, acetylene gas (C2H2), which was produced by mixing calcium carbide with water (CaC2 +H2O = C2H2); it was generated in a nearby factory and transferred by pipe to the users (Šahri, p. 222; “Čerāḡ-e gāz”).

Despite attempts at gas transportation as far back as 1821, it was not until after World War II that welding techniques, pipe rolling, and metallurgical advances allowed for the construction of reliable long distance pipelines, creating a natural gas industry boom (NGSA, “History”).

As recently as 1960, associated gas was a nuisance by-product of oil production in many areas of the world. The gas was separated from the crude oil stream and eliminated as cheaply as possible, often by flaring. Only after the crude oil shortages of the late 1960s and early 1970s did natural gas become an important world energy source (Encyclopedia Britannica, “Natural Gas”).

First industrial use of natural gas in Iran. In 1908-1912, when oil was discovered in the Iranian southwestern region of Masjed Soleyman (Soleymān) and then processed in the newly built Abadan refinery, and until the early 1960s, the associated gases of produced oil were mainly flared, and the recoverable natural gas liquids (NGL) were under the control of the Iran Oil Consortium formed by the British, American, Dutch, and French oil companies. These were the largest foreign oil companies at the time in charge of Iranian oil production, refining, and export, according to the 1954 post-coup d’état Consortium Agreement with General Zahedi’s government (Movaḥḥed, p. 53; Elm, pp. 331-32).

The Consortium would interpret liquids separated from raw natural gas as a kind of crude oil; hence its recovery and sale, unlike that of the mostly flared natural gas, would fall under the Consortium Agreement for oil production in the designated oil fields of Iran and out of the scope of Iranian government control (Širāzi [Shirazi], pp. 22-23, 57-58; Mina, 2004).

The first industrial use of natural gas in Iran, apart from its limited use by the Consortium as fuel in local oil production facilities and the Abadan refinery (about 90 million cubic feet per day: Širāzi, p. 23), dates back to 1961-62. The separated ‘associated gas’ in the Gachsaran (Gačsārān) oilfield, would receive the required processing in the Gachsaran gas refinery (the first Iranian gas refinery), which had a capacity of 20 million cubic feet per day for acid gas (H2S and CO2) removal and dehydration. Next, it was transferred via a 275-km, 10-inch (and 6-inch) diameter pipeline to Fars (Shiraz) Cement Mill, and then for further distribution to Marvdasht (near Shiraz) Sugar Mill, among other industrial users in the area (Eṭṭelā’āt, 1961; Mehrvarz, p. 357; Razmkhah, ed., p. 23).

The French-built Marvdasht ammonia-urea (fertilizer) plant was inaugurated as the first Iranian petrochemical plant by General de Gaulle and the shah of Iran in 1963, and started to use the gas supplied by the pipeline as its feed and fuel. To increase gas transfer capacity in the late 1960s, the old pipeline was replaced with a higher capacity pipeline from the newly built Bid Boland Gas Refinery, which also received Gachsaran gas on its route to Shiraz. The old pipeline was used for crude oil transfer from Gachsaran to a new oil refinery at Shiraz (Širāzi, pp. 23, 52).

The construction of this fertilizer plant, initially, was the subject of a heated dispute in the late 1950s between Ja’far Sharif Emami (Jaʿfar Šarif Emāmi), the minister of industries and mines (Vezārat-e ṣanāye’ va ma’āden), and Abul-Hasan Ebtehaj (Abu’l-Ḥasan Ebtehāj), managing director of the Plan Organization (Sāzmān-e barnāma). The latter argued against the uneconomical nature of constructing a gas pipeline solely for a small 85,000-ton/year fertilizer plant (urea and ammonium nitrate, among other products) that could had been built profitably in Khuzestan province due to the short distance to natural gas resources and to potential markets, as well as the availability of railroad/sea transportation (ʿAliḵāni, pp. 166-67;Šarif Emāmi).

In 1965, the National Iranian Oil Company (NIOC/Šerkat-e melli-e naft-e Irān) held protracted negotiations to reach an agreement with the Oil Consortium on different issues, including the right to exercise its sovereignty over the associated gas—not even its liquids‑—beyond the designated volume for the oil fields and Abadan refinery fuel (Faḵimi [Fakhimi], p. 271; Mina, 2004).

In 1967 out of 1,400 million ft3/day associated gas produced in the oil fields, about 90 million ft3/day was used as fuel in the oil fields and in the Abadan refinery, and 20 million ft3/day was used in the Marvdasht petrochemical plant, while about 1,300 million ft3/day (17 billion cubic meters per year) was burnt (flared) in the oil fields. Iranian crude oil had a range of 480-1,000 ft3 associated gas per barrel of produced oil. In 1966 Iran oil production was about 2 million barrels per day; that means that an average of 650 ft3 gas per barrel of produced oil was flared. This was equivalent in terms of average heating value to 224,000 bpd of crude oil or about 12 percent of the produced oil each day in 1966 (Nāmeh-ye sanʿat-e naft, Dey 1346 Š./December 1967, p. 13; Širāzi, p. 23; BP, “Energy Charting Tool”).

However, in January 1967 NIOC signed an agreement with the Consortium on a $50 million dollar joint project in Mahshahr Port (Bandar-e Māhšahr) to fractionate up to 48,000 bpd of the Consortium-produced NGL into LPG and other products for export as a petrochemical investment project (Bartsch, p. 260; Nāmeh-ye sanʿat-e naft, Tir 1349 Š./June 1970, p. 10, and Mehr 1351 Š./October 1972, pp. 11-13).

In the mid-1960s, as a result of discovery of five gas wells with non-associated, highly sour gas (25% H2S and 10% CO2) in the Masjed Soleyman area, it was decided to send part of the produced gas (175-230 million ft3 out of 350 million ft3/day) via a 170-km 20-inch diameter pipeline to the newly built Mahshahr plant. Constructed during 1967-70 by a 50-50 joint venture of NIPC and the U.S. firm Allied Chemical-Kellogg, Shāpur Chemical Plant (today’s Rāzi Plant) had gas sweetening and ammonia-urea, sulfuric acid, sulfur, and di-ammonium phosphate units. This plant was run by the nascent NIPC (National Iranian Petrochemical Company) (Nāmeh-ye ṣanʿat-e naft, Mordad-Amordad 1351 Š./August 1972, p. 6).

In 1965 Kharg Petrochemical Complex was established as a 50-50 joint venture between NIPC and the American AMOCO using 150 million ft3/day of the associated gas produced in the Persian Gulf offshore oil rigs that were out of the Consortium control. The Kharg Complex produced sulfur, propane, butane, pentane and heavier components for export (Mehrvarz, p. 201).

The Iran-USSR Gas for Steel Mill Agreement of January 1966. In January 1966, Iran and the Soviet Union signed an agreement (see “Iran-U.S.S.R. Steel Mill and Gas Pipeline Agreement”; CIA, p. 1) which provided that the USSR would advance credits of $289 million at 2.5 percent interest over a twelve-year period for the construction of a steel mill, a gas pipeline to the Soviet Union and a machine tool plant, within the framework of a barter deal. The gas pipeline first phase was to go into operation in 1970, the steel mill in 1971. Both of these projects were to be repaid, with interest, by exporting natural gas to the USSR over a 15-year period ending in 1985 (Yeganeh, pp. 38-47; CIA, pp. 1, 5-7; Wolfe; Yusefi).

Soviet experts after comprehensive studies selected Dasht-e Tabas, 45 Km to the south west of Isfahan city, as the steel mill optimum location. The mill was to receive natural gas as its source of energy through a branch of the above nearby gas trunkline (Isfahan Steel Mill).

The formation of NIGC in March 1966 and its first tasks and achievements until the early 1970s. Right after the Iran-USSR Agreement, the National Iranian Gas Company (NIGC, Šerkat-e melli-e gāz-e Irān) was established in March 1966 (Esfand 1344 Š.) as an affiliate of the National Iranian Oil Company (NIOC) with a capital of 700 million Rls. (about $10 million). In 1972 the Iranian parliament passed the “Gas Industry Development Law,” according to which NIGC was allowed to make joint ventures with qualified foreign and domestic companies in public and private sector projects. In November 1977, a new statute was approved, and NIGC’s paid up capital was increased to 25.5 billion Rls.—–the equivalent of about $365 million (Mehrvarz, pp. 93-95; Širāzi, p. 28; NIGC, 2014a, p. 6; NIGC, “NIGC,” “Iran's Gas Industry History”).

According to the Statute of NIGC, the NIOC (at the time actually through the Oil Consortium of foreign companies) was nominally in charge of upstream oil/associated gas production, and NIGC jurisdiction would start after the field production units, which were separating natural gas from produced crude oil and then separating its gas liquids (NGL). In other words, NIGC was in charge of gathering, refining, transportation, and internal distribution, as well as export of ‘lean’ natural gas and not its separable liquids (Širāzi, pp. 138-140, 21) .

Liquid petroleum gas (LPG) safety standards and the distribution by private companies for domestic and commercial users that was in practice since the mid-1950s also came under NIGC jurisdiction and regulation (Širāzi, pp. 118-19). Major tasks of the NIGC immediately after its formation and afterwards were the following:

Organization. Definition of organization structure and staffing was based on the usual ‘staff functions,’ such as engineering and development planning, safety, financial, contracts, procurement, administration, and security, as well as ‘line functions’ or operations covering gas gathering, refining, storage, transfer and distribution. The NIOC was the sole share holder of NIGC, but the General Assembly of Share Holders, or Majmaʿ, as the superior body of NIGC, was headed by the prime minister, just like the NIOC Assembly (Širāzi, pp. 137-40).

However from the very beginning there was a rivalry and disagreement between NIOC and NIGC regarding operational control of the natural gas resources and their development and allocation planning that has lasted until today (Širāzi, p. 136; ʿArāqi: interviews with Jarrāḥi and Ḥasantāš, pp. 47 and 68, 402-3, respectively).

The required staff were supplied through NIOC transferred personnel and foreign consultants as individuals or companies. Also, a training program was set up both inside and outside Iran, including the then Soviet Union, to make the required skills available during construction and running operations. (Širāzi, pp. 52, 123-28).

Export gas price adjustments. Export gas price to the Soviet Union, as well as the capacity and location of the steel mill to be built by the Soviets, were among the issues to be negotiated with the latter after the Agreement of 1966 (Yeganeh, p. 123).

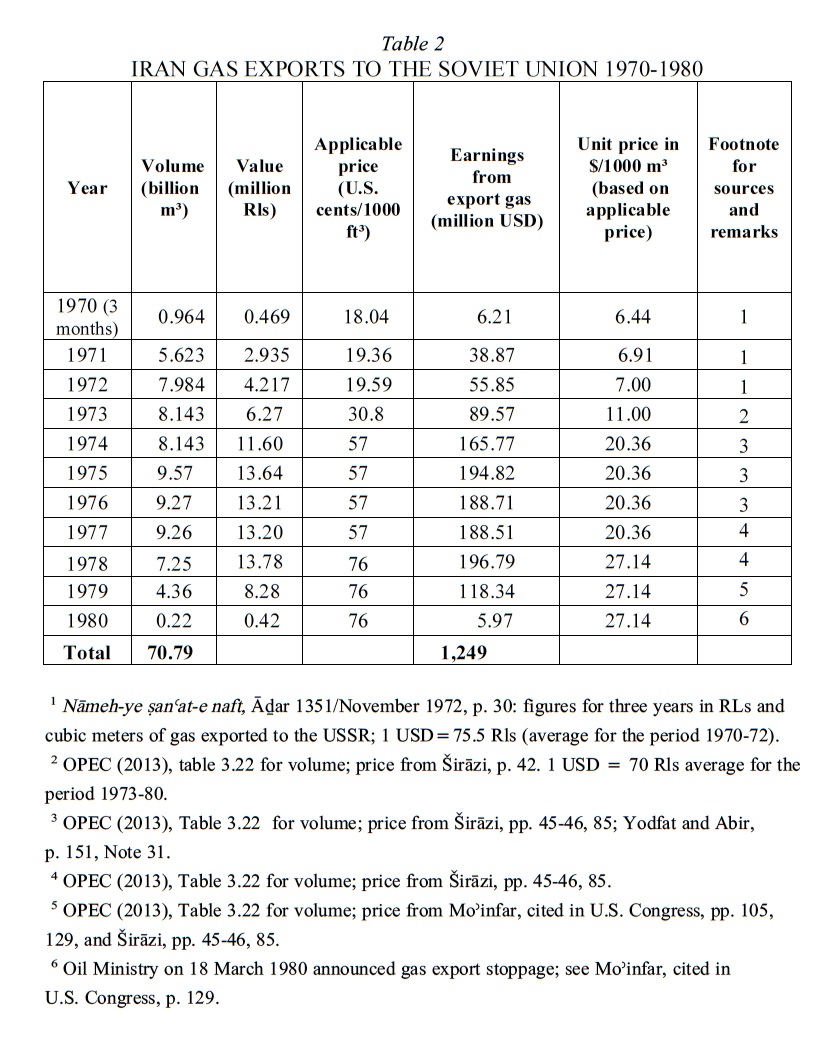

To reach a final price escalation agreement detailing price and other contractual matters, issues such as duration, quantity, quality, price escalation, metering at Astara (Āstārā) border station, invoicing, payments, force majeure, liabilities, take-or-pay (obligation for paying a certain percentage of the price for the contracted export gas capacity in case gas was not actually imported to that amount by the buyer for reasons other than force majeure), penalties for non-delivery of gas, and other matters were to be negotiated with the Soviets in the late 1960s before the actual startup of the gas export in October 1970. In these negotiations Iran succeeded in obtaining the right to 80 percent of the non-received gas price with no liability for any non-delivery of gas to the Soviet Union (Širāzi, pp. 37-38).

As for the original gas price basis of the 1966 Agreement, there are two differing versions—6 Rubles versus 4 Rubles per 1,000 cubic meters; but the following two accounts are consistent in other details of the Agreement.

According to Mohsen Širāzi, a top NIGC official at the time, the original, unchangeable Agreement Protocol price was 6 Rubles (about 6.60 USD at 1965 official, gold-based exchange rates) per 1,000 cubic meters of natural gas (or about 18.71 cents per 1,000 ft3 with a predefined fixed heating value). As a result of the unavoidably reduced heating value caused by dew point adjustments of the wrong figure cited in the 1966 Agreement, the actual price, one might conclude, could had been reduced by 15 percent to about 16 cents per 1,000 ft3. It must be noted that the date of actual gas export was four years after the Protocol price basis was signed and made the gas price subject to any applicable price escalations (Širāzi, pp. 32-33, 41; CIA, p. 6).

However, according to the U.S. Embassy dispatch of 10 April 1973, Taghi Mosaddeghi (Taqi Moṣaddeqi) , the NIGC second managing director since 1969, had explained:

Protocol to 1966 Agreement on gas barter deal provided basic price of four Rubles per thousand cubic meters with possible add- on of maximum of two Rubles more. (for purposes of Protocol Ruble pegged to a gold value equal to $1.11). Actual amount of add-on based on index of Persian Gulf light fuel oil at Abadan or Mahshahr with increase in index between 10 and 30 percent determining percentage of 2 Rubles add-on. With increase of more than 30 percent, automatic Renegotiation of price was to take place. Since early 1971 (after [OPEC’s] Tehran Agreement), when PG light fuel index was increased about 40 percent, Iranians had been pressing for these negotiations. Soviets finally agreed to send a negotiating team during recent Kosygin visit (U.S. Embassy, 1973a; for actual price developments and gas export earnings, see below, Economics of IGAT-1 and Table 2)

{kind=link}

According to the new, negotiated escalation for exported gas price, which took eleven months to negotiate, because of up to 30-percent price linkage of gas with Mashahr light fuel oil price (which was a very positive provision for Iran in the original agreement with the Soviets), its price gradually increased to an average 19.5 cents during 1970-72 (with heating value corrections: see Table 2 for officially published figures for the price and volume in this period) and reached 30.8 cents per 1,000 ft3 in mid-1973 after the OPEC oil price hike of 1971 (Širāzi, pp. 40-42, and p. 85; Amuzegar, p. 257; also see Table 2).

3. THE FIRST GAS TRUNKLINE (IGAT-1)

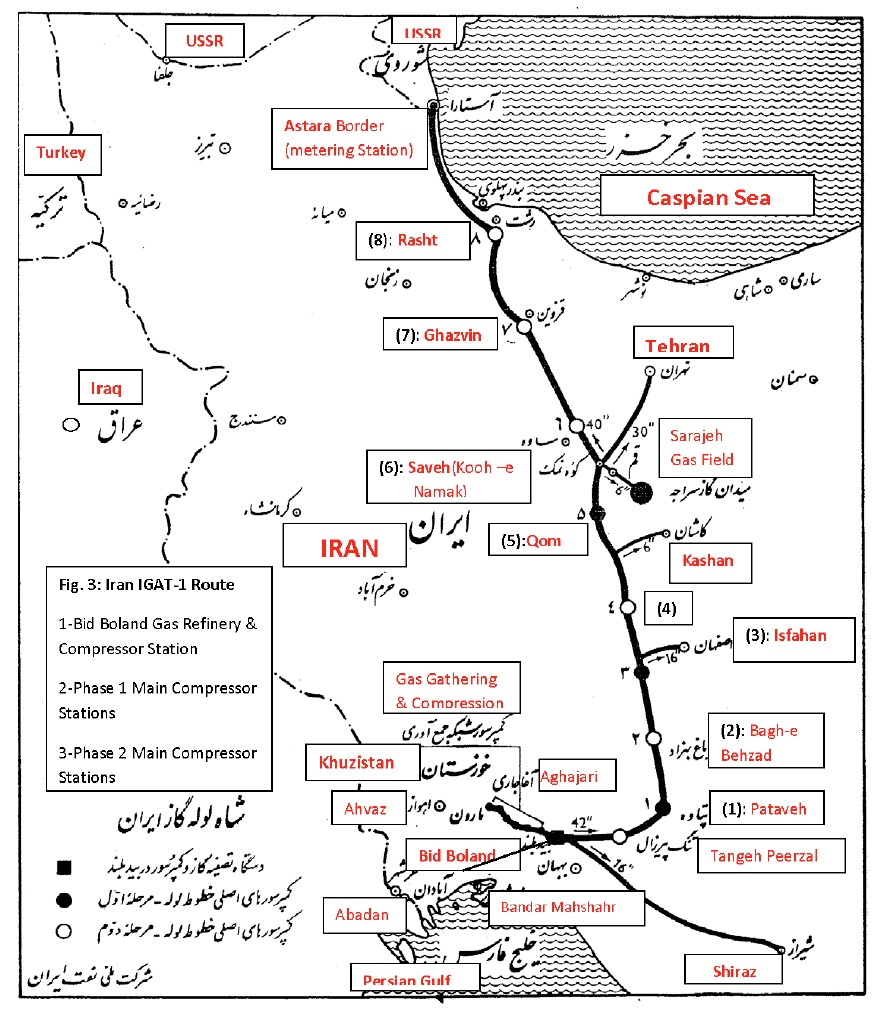

Trunkline design and construction. The Iran-Soviet Union pipeline under a 15-year contract was to carry up to ten billion cubic meters of natural gas annually to the Soviet Union and up to about 7 billion cubic meters for internal uses. It was 1,100 kilometers long (consisting of two segments of 42 and 40 inches in diameter) and was called the First Iran Gas Trunkline ‘Shah-Louleh’ or IGAT-1.

Its first, 600-km-long, 42-inch segment from Bid Boland Gas Refinery in southern Khuzestan Province to Saveh (near Tehran) was designed and supervised during construction by the NIOC/NIGC engineers and the British consulting company Iranian Management and Engineering Group (IMEG). IMEG was established in 1964 as the Oil and Gas Division of Sir Frederick Snow and Partners for Iran projects—presumably with the Imperial Court’s blessing (Faḵimi, p. 687; Širāzi, p. 99; IMEG Ltd.).

The second, 40-inch segment from Saveh to the Soviet border—as well as a 30-inch branch to Tehran—was designed and constructed (with the help of Iranian construction companies) by the Soviets (Nāmeh-ye ṣanʿat-e naft, Āḏar (Azar) 1349 Š./December 1970, pp. 4,5,10; Širāzi, pp. 55-56; Bid Boland; IMEG Ltd.).

The total capacity of the first 42-inch segment (600 km) of this pipeline from Bid Boland Gas Refinery in Khuzestan Province to Saveh was about 16-17 billion cubic meters per year, of which 6-7 billion cubic meters was designated for distribution through 667 km of branch lines in various central cities and industries inside Iran (Shiraz, Isfahan, Kashan, Qom, Tehran, and later, Alborz Industrial Town). The second segment (40-inch diameter) of IGAT-1 extending from Saveh to Astara border between Iran and the Soviet Union could carry the remaining 10 billion cubic meters per year upon gradual completion of all the compressor stations by 1975 (Nāmeh-ye ṣanʿat-e naft, Āḏar 1351 Š./November 1972, pp. 8-9; Širāzi, pp. 47-48).

The 42-inch segment was partly constructed by the Will Bros (Williams Brothers) firm of the UK and Will Bros of Germany, as well as U.S.-British Neil Price, which together completed the system piping for oil field gas gathering and the initial 170 kilometers of the 42-inch trunkline passing through the tough, rocky terrain of the Zagros mountains. The French Entrepose construction company was the sub-contractor for the remaining 430 km of the 42-inch trunkline, as well as the supplier of phase one gas-gathering, turbine-driven compressors made by the French Dresser Clark company. Entrepose was also the sub-contractor for IGAT-1 off-take branches to Isfahan, Kashan, Sarajeh, and Qom. The German Mannesmann construction company, with the help of Iranian construction companies, was the subcontractor for construction and installation of four of the trunkline compressor stations in its central sections (see the IGAT-1 detailed route map in Figure 3; Nāmeh-ye ṣanʿat-e naft, Tir 1347 Š./June 1968, p. 5; Tir 1348 Š./June 1969, p. 5; Tir 1349 Š./June 1970, pp. 8-9; and Āḏar 1349 Š./ November 1970, pp. 4, 5, 10).

{kind=link}

A total of about 750,000 tons of pipe and equipment and structural steel were used in the IGAT-1 project. An average of 7,000 people (20,000 at the peak) were working in the construction companies involved in the project, 900 of them foreign nationals (Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, p. 10).

The coated and wrapped pipeline had impressed, current cathodic protection and was buried about one meter underground except in very rocky terrains, where this could be reduced to 30 cm. Along the route of IGAT-1 there were seven underriver crossings and one overriver, bridged crossing at Sefid Rud near Rasht. The sectionalizing (line break/line block) valves were installed at 30-km intervals in certain sections and at all river crossings or other potentially hazardous locations (Froozān et al., p. 32; Nāmeh-ye ṣanʿat-e naft, Bahman 1348 Š./January 1970, p. 10).

To provide for ‘peak shaving’ capacity during cold seasons, studies were undertaken on the economics of utilizing underground storage along the route of IGAT-1 in the Kuh-e Namak salt cavern as well as at the Sarajeh (Sarāja) sweet gas reservoir, both near Qom (Froozān et al., p. 37), but neither one materialized before 1979.

The telecommunications system for phase one of IGAT-1 and its local branches was based on 47 radio stations, which would make communications possible among eight compressor stations and related facilities in Bid Boland, Isfahan, Kāshān, Alborz, Tehran, and Astara (Nāmeh-ye ṣanʿat-e naft, Ordibehesht 1348 Š./May, 1969, p. 20).

Also, in 1975 CFS Thomson S.A. of France was awarded a contract to build 35 microwave sites, connected by PABX systems, for the National Iranian Gas Company (NIGC) on Iran’s IGAT-I gas line to the Soviet Union. This project, valued at $12 million, was slated to be completed by 1978. It was expected that by 1980, with the completion of Iran’s IGAT-2 gas line, another similar contract would be awarded for that gas line project (U.S. Department of Commerce, 1977, p. 60; Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, p. 10).

The gas gathering network and Bid Boland Gas Refinery. In the gas/oil separation plants (or production units – GOSP or PU) located in the oil fields, raw associated gas received along with oil from a number of related oil wells was first separated from the extracted oil. Then the rich gas from the high-pressure, first stage separator was directed to nearby NGL plants. In these plants, natural gas liquids (LPG and heavier hydrocarbons), called NGLs, were separated by chilling the gas; then they were pumped to Mahshahr Port NGL fractionation (NF) plants for subsequent production of propane, butane (called LPG when mixed together), pentane, and heavier hydrocarbons, mainly for export by the Consortium, but also increasingly for domestic use of LPG distributed in gas cylinders. All these facilities were managed and controlled by the Oil Consortium until 1974-75 (Širāzi, p 30).

The produced lean sour gas (with high H2S and CO2 content) was gathered from the oil fields NGL plants through a gas gathering network and was sent by gas gathering compressors and pipelines to Bid Boland Refinery (Širāzi, p. 30).The Refinery was designed by the American Pritchard Corp. for lean sour gas sweetening and dehydration and was constructed by the British firm Costain & Press Ltd. under supervision of the British IMEG between 1968 and 1970 at a total cost of $44 million (daily Eṭṭelāʿāt, 25 Āḏar 1350 Š./16 December 1971). Also three British gas compressor units were installed by Costain & Press, each having 8,700 hp (6,500 KW), for running the produced gas into the pipeline.

Bid Boland Gas Refinery had a nominal refining capacity of 32 million cubic meters per day (with future expansion capacity to over 57 million m3/day or 20 billion m3/year), presumably upon full build-up of planned internal consumption (see Figure 4). The gas product was to be in accordance with IGAT-1 required gas specifications in terms of heating value and dewpoint temperature and exit pressure (Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, pp. 4-5, 10; Bid Boland; Širāzi, p. 57).

{kind=link}

The export gas output of Bid Boland had the following approximate specifications (Nāmeh-ye ṣanʿat-e naft, Dey 1346 Š./December 1967, p. 42; see also Froozān et al., p. 31):

|

Component Name |

Mole percent |

|

Methane (CH4 ) |

83% |

|

Ethane (C2H6) |

12% |

|

Propane (C3H8) |

3.5% |

|

Butane (C4H10) |

1.5% |

|

Out of a Total |

100% |

|

Specific gravity: |

0.66 |

|

Dew point max. temp. |

-10° C (at approx. 55 barg for hydrocarbons and 44 barg for water) |

|

Heating value |

1060 BTU/ft3 |

|

CO2 |

Max. 1 mole percent |

Actual gas export at a free flow lower capacity—before the gradual start-up of the pressure boosting compressor stations along its route—started in October 1970 (Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, pp. 4, 5, 10). However, the official inauguration and handover of the completed phase one of the IGAT-1 pipeline facilities (except for several remaining compressor stations that were defined as phase two), including Bid Boland Gas Refinery, was in mid-December 1971 in a ceremony attended by the shah in Bid Boland Refinery. This pipeline would provide natural gas to the southwestern Soviet republics, as well as some Iranian cities and industries along its route (Širāzi, pp. 51, 60; see also Figure 2).

Gas compressor stations. There were 10 gas turbine-compressor (turbo-compressor) stations along the route of IGAT-1; these were gradually brought into service between 1971 (five stations completed) and 1975 (five more stations completed). Also, a metering station was installed at the Astara border to measure the exported gas volume and its heating value and composition, and other characteristics. Except for the Bid Boland Gas Refinery compressor station (3X 8700 hp; see above), and Tange Pirzal (Pirzāl Mountainpass, Tanga-ye Pirzāl: 4X8700 hp), 8 stations were equipped with 34 Russian-made turbo-compressors, each having 11,400 hp.

The IGAT-1 10 compressor stations had a total installed power of about 450,000, hp (for a flow rate of about 1,650 million ft3/day or 46 million m3/day or 16.9 billion cubic meters per year) and maintained a pipeline pressure of about 750-1,100 psig (pounds per square inch gauge) between the stations (Nāmeh-ye ṣanʿat-e naft, Tir 1349 Š./June 1970, pp. 6-8; Āḏar 1349 Š./November 1970, p. 10; Summer 1354 Š./Summer 1975, p. 21).

During the phase two (1971-75) development of IGAT-1, in order to increase the trunkline capacity to its design value (from 10 to about 16-17 billion cubic meters per year), two more gas gathering compressor stations were installed near Maroun field’s NGL No. 3 (100 million ft3/day delivery rate using 2X6,000 hp reciprocating compressors) and Ahvaz. These provided a total of 600 million ft3/day (6 billion m3/year) additional gas input to Bid Boland refinery. The Ahvaz compressor station (500 million ft3/day delivery rate) was equipped with 4X8,000 hp reciprocating compressors supplied by the U.S. firm Worthington Industries in 1972. The compressed gas in Ahvaz was transferred via a newly built 117-km, 40-inch diameter pipeline to Bid Boland Gas Refinery (Nāmeh-ye ṣanʿat-e naft, Summer 1353 Š./Summer 1974, pp. 16-17; Esfand 1351 Š./ February 1973, p. 15).

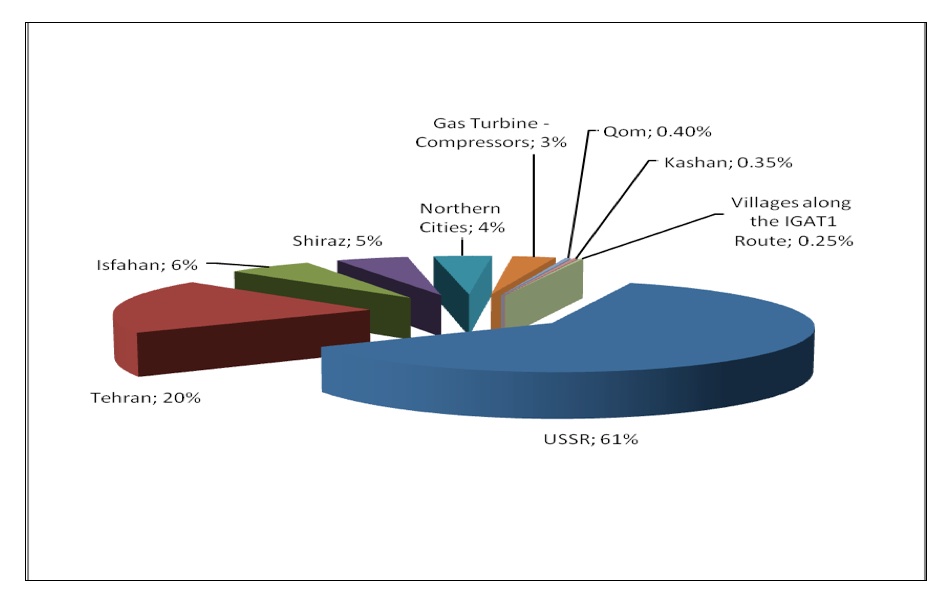

The field gathering compressor stations that were pumping gas from Aghajari (3 stations having 8 Dresser Clark reciprocating compressors with a total installed power of 48,000 hp), Maroun (3 stations), and Ahvaz (1 station) oil fields in Khuzestan province to Bid Boland Gas Refinery were all Western-made and had a total installed power of about 90,000 hp (after completion of phase two). The total installed power of all the turbo-compressors serving IGAT-1 was 450,000 + 90,000 = 540,000 hp or approximately = 400 MW. By excluding the stand-by compressors and assuming a ratio of 0.7 for the operating compressors, we come up with 280 MW gas turbine power generation, which was almost equal to one-half of the Dez (Khuzestan) Hydro-electric Dam’s considerable power generation capacity of 520 MW at the time. The gas consumption of the gas turbine drivers of the compressors was about 3 percent of the gas transported by IGAT-1. For comparison, that is one-half of the total Isfahan (6 percent) off-take, as shown in Figure 4 (“Ṭarḥ-e Šāh Luleh Gāz,” Nāmeh-ye ṣanʿat-e naft, Tir 1349 Š./June 1970, pp. 6-9; Āḏar 1349 Š./November 1970, p. 10; Daneshju-club.com; Kuhn, pp. 228- 29; Mehrvarz, pp. 344-45).

Manpower of NIGC. NIGC in spite of IMEG’s strong interest in becoming the operator of IGAT-1 used its own well-trained personnel to run the trunkline operation and maintenance with limited support of foreign specialists (Russian, European, and American). The number of employees at NIGC in 1972 before completion of phase 2 was as follows (Nāmeh-ye ṣanʿat-e naft, Āḏar 1351/November 1972, p. 32; Širāzi, pp. 55-56):

|

engineers , technicians, and administration |

1,159 |

|

workers |

1,239 |

|

foreign employees |

30 |

|

Total |

2,428 |

The total number of NIGC employees by 1979 had increased to about 4,000 (Širāzi, p. 125).

Ahvaz Pipe Mills Co. The large diameter pipes used in IGAT-1 (42/40 inches in diameter, API 5L, X60 material with 0.500 and 0.600/0.477-inch wall thickness and 60,000 psig minimum yield strength, Froozān et al., p. 31) were partly produced and tested in Ahvaz Pipe Mills by plate rolling and seam welding. The plant was established by NIOC in 1966-67 in a $14 million contract with the U.S. firm Torrance Machine and Engineering, Inc., and was intended to fabricate 400,000 tons out of a total of 500,000 tons of the needed pipes by using imported flat plates and coiled plates from Europe. The balance of needed pipes was planned to be imported from Europe and Japan. However, because of lack of proper training of the workers and start-up and weld testing problems (Mosaddeghi, cited in Faḵimi pp. 698-99; U.S. Bureau of Mines, 1967, p. 371) only 70,000 tons of the Ahvaz mill products were actually used in the IGAT-1 project, and the balance was imported from Europe and Japan (Dr. Eqbal’s Pipemills ‘ground breaking ceremonies’ report to the shah on 12 Āḏar 1346 Š./20 November 1967, in Nāmeh-ye ṣanʿat-e naft, Dey 1346 Š./December 1967, p. 44; his IGAT-1 inauguration speech before the shah and the Soviet President Nikolai Podgorny on 28 October 1970, printed in Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, pp. 4, 5, 10; Bartsch, p. 260, fn 98; Mosaddeghi, cited in Faḵimi pp. 697-700).

Taghi Mosaddeghi a prominent NIOC official in the southern oil regions heading non-Consortium-related activities such as residential and administrative buildings, parks, hospitals, warehouses, and roads, soon became the Pipemills managing director, in 1967, and two years later in 1969 he became the second managing director of NIGC, replacing Houshang Farkhan, the first managing director. He kept this post until the last months before the revolution of February 1979 and continued with his Pipemills position as well (Širāzi, p. 53; Faḵimi, p. 698; Šamsa).

The first of two units at Iran’s first Pipemills was completed during 1967. This unit had a 20,000 ton capacity per month (in two daily work shifts per 25-day month), producing 18 to 42-inch pipes. The second unit, completed in 1968, was scheduled to produce 10,000 tons (in two shifts) per month of 6 to 16-inch pipes used in oil and gas projects. Therefore, the total capacity of the two plants was 360,000 tons per year. The Pipemills equipment was financed jointly by NIOC and Torrance, and the National Iranian Oil Company (NIOC) was responsible for all the utilities, access road, railroad to Bandar Mahshahr, and buildings and amenities for the plant employees (Nāmeh-ye ṣanʿat-e naft, Dey 1346 Š./December 1967, pp. 8, 40, 44; U.S. Bureau of Mines, 1967, p. 371).

To speed up the pipe production and to provide for increasing needs of the country, two more plants, Nos. 3 and 4, were established in 1975 to fabricate small and large-diameter pipes. The plants’ machinery was supplied by the U.S. companies Torrance and Kaiser Steel at a cost of $45 million. In the same year, Pipemills dispatched a number of experts abroad in order to improve its technical potential and to update its industrial knowledge. The following year, to supply needed pipes for the second gas pipeline to the Soviet Union (IGAT-2), the company succeeded in producing pipes up to 56 inches diameter by upgrading the equipment of large-diameter pipe plant and by importing plates from Japan, Italy, and West Germany (Mosaddeghi, cited in Faḵimi pp. 698-99; Ahvaz Pipe Mills; Nāmeh-ye ṣanʿat-e naft, Autumn-Winter 1356 Š./Autumn-Winter 1977-78, pp. 14, 34, 35; U.S. Embassy, 1976, p 3).

Economics of IGAT-1. The revised estimate (in 1967) of the total cost of the pipeline to reach its full capacity of 16-17 billion cubic meters per year in two phases (planned for 1971 and 1975) was about $450 million (CIA, p. 6; World Bank, p. 27); that was $100 million above the initial estimate of $350 million by IMEG as NIOC consultant. An increase in less than a year, which moved the estimate even further up to about $650 million infuriated the second Pahlavi shah (‘Alam, Yāddašt-hā-ye ‘Alam I, for 17 Esfand 1347 Š./8 March, 1969; cited in Faḵimi, p. 365) and led to rumors about replacement or retirement of some top officials of NIOC/NIGC in 1969 (Faḵimi, pp. 686-88; Širāzi, pp. 51-52).

It must be noted that after the first instance of cost estimate escalation of the gas trunkline, its economic feasibility was questioned by the Plan Organization. In a meeting in the presence of Dr. M. Eqbal and S. ‘Asfia, the managing directors of NIOC and the Plan Organization, respectively, apparently convincing arguments were made by NIGC representatives regarding the economic feasibility of the pipeline construction (projecting a 15-percent calculated annual return on investment), which received the approval of the attending officials (Širāzi, p. 50). But in 1968, the French Sofregaz (an affiliate of the state-owned Gaz de France) gave 10-percent lower estimated prices for comparable equipment costs in proposing a 4,000-km pipeline from Ahvaz (southern Iran) passing through Turkey, Greece, and Yugoslavia to Trieste in Italy. This might have been another reason for a second look at the escalated costs of the IGAT-1 for comparison (Širāzi, p. 79; NIGC, 1968; comparative analysis of the Sofregaz proposal in 1968 with IGAT-1 cost estimates at that time, internal report in Persian dated 4 Tir 1347 Š./25 June 1968, p. 16).

However, according to Dr. M. Eqbal, in his welcome speech to the shah and President Podgorny in October 1970 (see above), the final actual outlay was to be about $700 million ($458 million already expended for phase one and about $240 million expected for phase two), which was twice the original estimate (Nāmeh-ye ṣanʿat-e naft, Āḏar 1349 Š./November 1970, pp. 4, 5, 10; Majalleh-ye Oṭāq-e bāzargāni va ṣanāyeʿ va maʿāden-e Iran, Āḏar1349 Š./November 1970, p. 89; Širāzi p. 60; Froozān et al., p. 32). This total figure was cited by a credible source in 1992 (APS).

The Soviets would provide a $50 million credit for 8 Russian-equipped gas-turbine driven compressor stations, with a total of 34 gas-turbine compressors, each having 11,500 hp = 8.6 MW power or $130 per hp; this price was about one-third that of the $350/hp compressors offered by the Western companies, which were much smaller in size and weight. The Soviets also would provide $20 million for their related engineering services. The credit was all to be paid back by gas exports. Also, a $264 million credit was provided by France, Germany, and the UK for purchase of material and construction services, and its repayment with interest in hard currency was a heavy burden on the Iranian government at a time when the total annual revenue of oil exports, as almost the only source of hard currency earnings, was, for example, about $900 million in 1967 (Bartsch, pp. 260-61; Faḵimi, p. 364).

On the other hand, during the 15-year contract for gas export to the Soviet Union (1970-85), which was extendable for 5 more years, Iran was expecting to have accumulated a credit on its account with the Soviets of more than $500 million dollars. On average, that amounted to about $40 million per year at the then agreed-upon prices (CIA, pp. 6-8). The export gas price was in Rubles, which were to be used for import of goods and services from the Soviet Union, but its equivalent in Rials was paid to NIGC by the Iranian Central Bank (Širāzi, p. 79).

The escalated costs of IGAT-1 presumably made the internal gas market a major compensating source for the project’s economic viability. According to a paper jointly presented by three NIGC officials to the 11th International Gas Conference in Moscow in June 1970:

Since the tariffs for the sales of gas to households, commercial concerns and industrial consumers are higher than those for export, it will be found that the total revenue from domestic sales will soon exceed that obtainable from exports—even though the volume exported will be nearly twice the volume sold on the domestic market.

Thus, although the economic feasibility of the IGAT project is dependent upon export sales, the project relies rather heavily on internal sales in order to speed up debt retirement and shorten the payout period. Based on present programs, the payout period is conservatively calculated to be about 10 years. (Froozān et al., p. 33)

In this paper, the range of anticipated internal natural gas tariffs defined based on consumption location, type, and volume had a range of $8/1,000 m3 for the largest industrial consumers (above 2,000,000 m3/month) in Khuzestan province in the south to about $30/1,000 m3 for the smallest commercial and domestic consumers (up to 1,000 m3/month) in Tehran in the north (Froozān, Table 7, p. 39). These internal prices were significantly higher than the export gas price of maximum $6.60/1,000 m3 in the 1966 contract with the Soviets (see above).

However, following the Arab-Israeli war of October 1973, which led to a quadrupling of oil prices, and subsequent demands by the Iranian government for proportionate gas price hikes, which caused temporary stoppage of gas deliveries in July 1974, finally a compromise was reached, according to which the price of Iran gas exported to the USSR was raised from 30.8 to 57 cents per 1,000 cubic feet, and the new price was declared on Tehran Radio on 17 August 1974. This new price was not quite half the original demand of Iran (120 cents), but it was sanctioned by the shah with the argument that “we should look at gas price in a broader context; since our gas pipeline to the Soviet Union is as effective as several armies stationed in our common borders we should not insist for more than what we have already achieved” (Rubinstein, pp. 77-82; Yodfat and Abir, p. 151, n. 31; Širāzi, pp. 45-46).

The 57-cents price remained unchanged until 1978, when there was an increase to 76 cents. However, following the Islamic Revolution of 1978-79, Ali Akbar Mo’infar, first holder of the new office of oil minister in the Islamic Republic of Iran and the second NIOC managing director, declared on 14 February 1980 that “gas shipments to the Soviet Union would be reduced to between 25-30 percent of the current level of 27.4 million cubic meters per day and that the price would be increased from 76 cents to $3.80 per 1,000 cubic feet.” This fivefold price hike was not agreed to by the Soviets (Mo’infar, cited in U.S. Congress, 1981, pp. 105, 129; Širāzi, p. 46; Mamedova, 2009).

One month later, on 18 March 1980, the Iranian Oil Ministry announced that gas deliveries of Iran to the Soviet Union had been stopped after price negotiations broke down the day before. Iran had asked for $164.50 per 1,000 cubic meters ($4.60 per 1,000 ft3), while the Soviets offered $112.60 per 1,000 cubic meters ($3.15 per 1,000 ft3) (Mo’infar, cited in U.S. Congress, 1981, p. 129).

Therefore, gas exports to the Soviet Union were completely stopped in April 1980 for a decade and then were resumed for a short time in a much lower volume in 1990-91, before being stopped for good after disintegration of the USSR in 1991 (see below).

On 5 July 1980, the Iranian oil minister stated that the Soviet Union refused to pay a fair price for Iranian natural gas, i.e., $4 per 1 million BTUs (about $3.80 per 1,000 cubic feet or $136 per 1,000 cubic meters). This, he said, was the same price as that of gas purchased by the United States from Canada and Mexico. The Soviets had said that the price was too high and that Iran should try to sell its gas to the United States. The Soviets had offered $2.20 per 1 million BTUs, or about $75 per 1,000 cubic meters (Moʾinfar, cited in U.S. Congress, 1981, p. 228; see also Segal and Niering, pp. 373-79 for a discussion of the world export gas prices ‘divergent arrangements’ in the second half of the 1970s).

Table 2 shows the developments in gas export volume and its price during 1970-80 and demonstrates a better outcome than earlier expected for gas export incomes in an even shorter period. This all became possible thanks to the dramatic oil price hikes in the 1970s, which resulted in demands by the Iranian governments for a higher gas price before and after the shah’s downfall.

The total gas export volume was about 70 billion cubic meters, and the total income (accounted in Rubles) was $1.2 billion, which on average for the 10-year period means 50 cents per 1,000 cubic feet or about $18 per 1,000 cubic meters. (Note: Figures cited in U.S. Department of Commerce, 1977, p. 209, Table 8, for natural gas export volume and earnings seem relatively valid only for the years 1973 and 1974 and otherwise are inconsistent with volumes and price hikes cited by reliable official sources.)

4. THE GAS INDUSTRY IN THE FIFTH NATIONAL DEVELOPMENT PLAN (1973-77)

Gas exports and internal consumption by IGAT-1. During the Fifth Development Plan (1973-77), and according to the upwardly revised budgetary targets upon the oil price quadrupling of 1973, natural gas development plans were to absorb about $2.5 billion in capital investment. Of this, $775 million would be provided by national development budget, over $1 billion by the National Iranian Gas Company (NIGC), and $700 million by foreign investments (U.S. Department of Commerce, 1977, p. 209 [rounded figures]).

Before oil industry strikes that occurred during the Islamic Revolution, the rate of gas export to the Soviet Union in 1975 (see Table 2) had reached its near maximum of 9.5 billion cubic meters (340 billion cubic feet) per year. In 1978 the internal consumption rate was about 4 billion cubic meters (Širāzi, p. 60). This was some 3 billion cubic meters lower than the anticipated IGAT- I delivery rate for internal consumption of about 7 billion cubic meters (see Figure 4), presumably due to the uncompleted state of distribution networks planned for the cities and industries.

In the final months of 1978, when the striking workers of Bid Boland gas refinery were forced by the regional martial law commander in Khuzestan Province to resume their work, they asked their colleagues in Qom compressor station, some 500 km to the north, to shut down their operation, and thus gas export was disrupted (ʿArāqi: interview with M. Motlagh p. 465).

As described above, as a result of the revolution and price disputes with the Soviets that began in 1979 during the Mehdi Bāzargān government, the export of gas to the Soviet Union was first reduced and then was totally stopped in April 1980 (see above). This was at a time that there was no alternative market for Iranian gas exports. Also, as a consequence of the reduction of oil production to about 25-40 percent in the immediate post-revolutionary years and during Iran-Iraq War in the 1980s, there was actually much less associated gas available for export through IGAT-1 (Kuhn, p. 229).

Interestingly, in 1987 at the height of Iran-Iraq ‘Tankers War’ in the Persian Gulf and the possibility of blockage of the Strait of Hormuz, the Iranian government instructed NIGC and NIOC to cooperate in converting the IGAT-1 gas pipeline (which was no longer being used for gas exports to the Soviet Union) to an oil export pipeline. They were to install the required oil pumping equipment along its route in order to bring about 700,000 barrels of oil per day to Astara, which would then be transported by the Soviets to the Black Sea for export. This plan was not put into effect in view of the cease-fire between Iran and Iraq in 1988 (IOPTC).

In the late 1980s and early 1990s, some attempts were made to resume gas export by IGAT-1, and agreements were reached. But, because of concurrent political upheavals leading to the independence of the former Soviet republics and price disputes with the Republic of Azerbaijan ($84.50 vs. $75 per 1,000 cubic meter proposed by the latter), there was no real progress in this regard (Kuhn, pp. 229-30; Mamedova, 2009). Therefore, IGAT-1 gas was used entirely for increasing internal consumption.

Development programs in the Plan. The general goals of the Iranian gas industry were defined in the Fifth Five Year Development Plan as: (a) more use of gas in the petrochemical industry; (b) more gas share in internal energy consumption; (c) more gas export and increase of the gas income; (d) more profitability for gas industry investments.

The specific development programs were declared as follows: (1) completion of the IGAT-1 phase 2; (2) study and construction of a second trunkline to meet the demands of power plants, petrochemical plants, and gas-based steel mills, among others, along the route of this pipeline; (3) development of Qeshm Island gas resources and construction of a Qeshm-Bandar Abbās pipeline to meet the local demands for power plants, gas-based direct reduction steel mills, the copper industry, and other consumers in the southeast of the country; (4) establishment of an integrated gas system in Khuzestan province; (5) development of Kangan gas field; (6) implementation of plans for gas distribution to the cities, such as Tehran, Ahvaz, Shiraz, Isfahan, and Mashad; (7) implementation of gas distribution to the villages on the route of the trunkline; (8) implementation of important projects such as Gachsārān-Khārg and the Kangan project, in order to increase gas export capacities and earned income.

Investment plans for the gas industry during the five year plan were defined with a total estimate of $2.4 billion (167.5 billion RLs; average exchange value: $1= 70 RLs.), to be provided from the following sources (Markaz-e pažuhešhā-ye Majles-e šurā-ye eslāmi [Majles Research Center], The Fifth Development Plan, revised version, 1973-1977):

|

public (government) funds |

$720 million |

(51billion RLs) |

|

NIGC |

$985 million |

(69 billion RLs) |

|

foreign investors |

$680 million |

(47.5 billion Rls) |

|

Total (rounded) |

$ 2.4 billion |

(168 billion Rls) |

According to the plan, the share of natural gas in total primary energy sources (such as oil refinery products, natural gas, hydro-electric power, nuclear power, coal, charcoal, rural products, and possibly other renewable energies) during the fifth plan was to rise from 18 percent in 1972 to 23 percent in 1977, and its use as fuel would triple. This growth was to be implemented by gradual substitution of natural gas for mid-distillate products (especially gasoil and kerosene). Internal gas consumption was expected to reach 9 billion cubic meters per year in 1977. The forecast for overall IGAT-1 gas transfer allocations for 1975 (17 billion cubic meters) is shown in Figure 4.

In the following sections, other developments in the Iranian natural gas industry during the 1970s are described.

5. THE SECOND GAS TRUNKLINE (IGAT-2)

Background. In April 1967, following preliminary meetings between a high-level Soviet trade delegation and Iranian officials, a communiqué was issued that discussed, in deliberately vague terms, possible additions to the original Agreement of 1966. The USSR had suggested that the IGAT-1 delivery rate for gas that was scheduled for 1974 (10 billion cubic meters per year) be advanced to 1970. Iran could do this if it was willing to commit to phase two expenditures four years sooner than planned. For expansion of the pipeline’s transfer capacity, the envisaged complementary compressor stations of phase two would need to be installed (see above). The USSR, for its part, offered to purchase an additional 10 billion cubic meters per year, but that would require a second pipeline, which neither the USSR nor Iran was yet willing to finance and construct.

The Soviet delegation also offered to “cooperate” in the search for oil in the “free areas” of Iran, presumably the parcels recently relinquished by the Oil Consortium (CIA, p. 3).

Also, as mentioned above, in 1968 Sofregaz had made a proposal to the Iranian government regarding construction of a new 48-inch diameter gas pipeline from Iran to Trieste that, compared to IGAT-1 escalating costs at the time, seemed more economical in respect to comparable pipe diameters and turbo-compressors. This project never materialized (Širāzi, p. 79; NIGC, 1968, pp. 18-22).

On the other hand, in the early 1970s the Iranian government was highly interested in receiving hard currency for its exported gas (Širāzi, p. 79). In view of the limited availability of associated gas in proportion to crude oil production and its increasing use inside the country, it was necessary to have a new and reliable gas resource to justify another costly export pipeline (Širāzi, p. 86).

At first, the “C” Structure in the Persian Gulf newly discovered by Shell Oil Company (then called Pars Field, 100 km to the southwest of Bushehr) was considered as a possible source for the second pipeline; it would also supply the newly conceived Kangan LNG Plant (Širāzi, pp. 111-12; also see below). But later, estimates of its reserves were revised dramatically downward, and it was no longer regarded as a reliable source (U.S. Embassy, 1976, p. 4).

NIGC then focused on using non-associated gas from the Kangan and Nār on-shore fields in the south of Fars Province near the shores of the Persian Gulf, which were discovered by EGOCO (European Group of Oil Companies). Three wells were drilled by EGOCO on Kangan and Nār, which proved the existence of very large gas reserves capable of producing in excess of the anticipated gas transfer rate for a 56-inch second trunkline—amounting to about 30 billion cubic meters per year (see Kangan Refinery, below).

Development drilling had stopped because of a dispute between EGOCO and Iran over contractual terms. EGOCO apparently maintained that it was entitled to continue developing its discoveries and to share in the earnings generated by sale of the gas. NIOC/NIGC apparently maintained that EGOCO was not in a position to exploit its discoveries (i.e., buy the gas) and that IGAT-2 was a project in which EGOCO had no interests (U.S. Embassy, 1976, pp. 4-5).

At this point in time all sorts of gas projects were under study or in preparatory stages for further negotiations (U.S. Embassy, 1974a, pp. 2-3).

According to a U.S. Embassy dispatch dated 29 September 1973, the NIGC managing director T. Mosaddeghi had confirmed to David Housego (Financial Times correspondent in Tehran) the latter’s information, heard from Prime Minister Amir ʿAbbās Hoveydā, regarding a forthcoming meeting in Moscow in a couple of weeks to discuss the possibility of a gas pipeline from Iran through the Soviet Union to Europe. Mosaddeghi had said that he was not sure the Germans would be present, but the Iranians and Russians would certainly be discussing the project (U.S. Embassy, 1973b, p. 2).

Contractual negotiations. Against the above background, and with previous consent of the Soviets, preliminary negotiations started in January 1974. first with Ruhr Gas of Germany, which was the largest importer of natural gas from the Soviet Union. Soon the French Gaz de France and OMV of Austria, as well as the Soviets (and later on the Czechoslovaks in a separate but similar deal) joined the negotiations. The parties arrived at, in essence, a triangular “swap deal” based on delivery of 17 billion cubic meters per year of Iranian non-associated gas from Kangan/Nār gas fields to the Soviet border at Astara, to be used mainly in the southwestern Soviet republics.

For their part, the Soviets would deliver a total of 13 billion cubic meters of gas per year (adjusted for its calorific value) from their own resources and pipelines to the above European companies at two major custody transfer stations at the Czechoslovakia borders with West Germany and Austria. Also, the Czechoslovaks would receive about 4 billion cubic meters per year with the same conditions as the Western Europeans (Širāzi, p. 86). The Soviets would receive an imputed ‘transit fee’ in hard currency from the European Consortium, and Iran would receive its gas price in hard currency from the European buyers. This scheme would make the project feasible by avoiding construction of a 4,200-km pipeline from Iran’s Astara border running through the Soviet Union and Czechoslovakia to the Western European borders (Širāzi, pp. 79-80, p. 84; Kuhn p. 231).

The 22-month negotiations to make the project feasible were mainly centered on pricing of the imported gas by the European Consortium (of the abovementioned parties, headed by Ruhr Gas). Also, the amount of the so-called ‘transit fee’ that the Soviets would receive in hard currency from the Europeans for this presumed Iranian gas transfer to Europe was an important, sometimes heated, topic of discussion (Širāzi, p. 84).

This mega-project brought the parties together for both the economics and the geopolitics involved, in terms of establishing a long-term, clean energy source for the energy-thirsty Europeans in return for hard currency badly needed by both Iran and the Soviets in the context of detente in the mid-1970s. At the same time, the Soviets were counting on a stable source of gas supply from Iran for their southwestern republics of Azerbaijan, Armenia, and to some degree Georgia, as well as on gas imports from Afghanistan for the gas grid of their southeastern republics (Victor and Victor, pp. 132, 202-233; Hannigan, p. 131; Stern, p. 32).

The Iranian delegation convinced the Europeans to accept its offered ‘floor price’ of 80 cents per 1,000 cubic feet of gas in order to guarantee a 14-percent rate of return on its large investments. However, Iran did not accede to the European demand for having a ‘ceiling price.’ The contract price was about $1.20 per 1,000 cubic feet to be paid in West German Marks. The escalation (or de-escalation) of this base price was linked to a price basket of 80 percent heavy fuel oil and 20 percent light fuel oil (Širāzi, pp. 84-85; see also Amuzegar’s price description, below).

The trilateral understanding was embodied in three contracts signed on 30 November 1975 by the highest officials of all the main parties involved, namely, NIOC/NIGC, Suyuzgazexport, Ruhr Gas, Gaz de France, and OMV. The three contracts were: (1) the contract for gas delivery at the Astara border to the Soviets; (2) the contract for gas transit from Astara to the European border; and (3) the contract for gas delivery to the European Consortium (Širāzi, p 88).

One year later, on 12 November 1976, Iranian and Czechoslovak (Metalimex Company) officials signed an agreement in Prague for the sale by Iran of 3.6 billion cubic meters per year of natural gas. The Czechoslovaks would pay their gas off-take price in hard currency to Iran (at the same rate as the Europeans) by balancing their account with their own deserved share of the transit route fee to the European border (U.S. Embassy, 1976, p. 2; Širāzi , p. 93; Mehrvarz, p. 346).

Take-or-pay and non-delivery clauses, in non-force majeure conditions (see IGAT- 1, above), were among the most complicated of the 20 clauses of the contracts. Non-delivery penalties were finalized with the Germans three months after signing the above contracts and did include the Iranian side demand for a ceiling on Iran penalties (Širāzi, pp. 90-93).

In the European Consortium, Ruhr Gas had a 50-percent share, and the French and Austrian partners had 33.33 percent and 16.67 percent shares, respectively (daily Eṭṭelāʿāt, 9 Āḏar 1354 Š./30 November 1975).

The total transfer capacity of IGAT-2 inside Iran was about 28 billion cubic meters per year, of which about 11 billion cubic meters was to be used inside Iran, and the balance (17 billion cubic meters per year) was to be exported to the Soviet Union. The project’s first phase was to be completed on a very tight schedule in five years, by January 1981; and three years later, in 1984, it would reach its full export capacity. Internal delivery of IGAT-2 gas was also to start in 1981, but it had an eight year build-up period to reach its full capacity of 11 billion cubic meters per year.

The contract duration was 20 years. It was estimated that the annual income generated from the exported gas in the first phase (about 9 billion cubic meters per year) in prevailing prices was 1 billion German Marks or about 27 billion Rls ($385 million) (daily Eṭṭelāʿāt, 9 Āḏar 1354 Š./30 November; Širāzi, p. 87).

Project costs. Iran’s investment in the project was a major concern for the government. Iran was to develop the Kangan/Nar gas fields and gas gathering systems, build a new gas refinery in two phases with design capacity of 42+38= 80 million cubic meters per day (2,850 million cubic feet per day) or 29.2 billion cubic meters per year (see below), as well as a 1,400-km (48-56 inches in diameter) pipeline with required compressor and metering stations, telecom., telemetry, and supervisory control (SCADA) systems. Also there were costs for infrastructure such as housing, roads, etc. at Kangan and along the transmission system.

Earlier in 1975, when the IGAT-2 project had been discussed in a cabinet meeting, Mansur Ruhani, the minister of agriculture, objected to the high cost of the project (then estimated at $1.6 billion, presumably mainly for pipes and turbo-compressors procurement and not construction and facilities costs [see below]); he said that by using 42-inch pipes instead of 56-inch diameter pipes the project cost could be halved— obviously by using a much higher transmission pressure, which would lead to more gas compression horsepower. This position was sent by Prime Minister Hoveyda to arbitration by the minister of industries, and after two months of studies and discussions among the parties, it was concluded that, in terms of first capital expenditures (CAPEX), the proposed scheme could be somewhat beneficial. However, in terms of operating expenditures (OPEX) during the 20-year life cycle of the project, by taking into account the cost of a higher rate of natural gas consumption as fuel for the larger turbo-compressors needed by the 42-inch operation, the NIGC scheme using 56-inch pipe was more economical, on balance (Širāzi, pp. 93-97).

The IGAT-2 design and construction cost in 1975 prices, and without allowance for interest charges, was expected to be $2.5 billion, of which $1.5 billion was allocated for material and equipment (largely imported), while $1 billion was expected to be needed for engineering services and construction costs. The foreign component of engineering and construction was to be very high, since NIGC recognized the need to rely heavily on foreign skilled labor, specifically including even welders (U.S. Embassy, 1976, pp. 2- 3).

The total investment cost for IGAT-2 in the Soviet Union, Western Europe, and Czechoslovakia was estimated as 40 billion German Marks ($15.4 billion) (Širāzi, p. 88). The Soviets had to build a 2,480-mile (4,000-km) pipeline from Siberia to the Czechoslovak border and their gas price charged to the Europeans had a range of $1.43-$1.60 per 1,000 ft3. The difference between their price and the price paid to Iran, i.e., 96 cents per 1,000 ft3 at delivery time in 1981 (based on the price of fuel oil at the German border) was considered their transfer fee (Amuzegar, p. 258).

NIGC plannedto purchase all the equipment and materials with suppliers credit, and the two new production lines for Ahvaz Pipe Mills, one from Torrance and the other from Kaiser, were among the first purchases of capital equipment, at a cost of $45 million (Mossadeqi cited in Faḵimi, p. 699; see also Ahvaz Pipe Mills, above). NIGC had contracts also with suppliers from Japan, West Germany, and Italy for steel plates. Total cost of steel for pipe fabrication would reportedly approach $350 million. Cost of engineering services and construction was expected to be paid for by Iran from its current income (U.S. Embassy, 1976, p. 3).

As gas markets yielded low profits, while investment cost were rather high even before the Islamic Revolution, the Pahlavi regime began to review its natural gas policy with the aim of promoting internal utilization at the expense of export projects (Kuhn, p. 231).

Announcements by industry officials at the end of 1976 indicated that Iran was to try to conserve most of its gas reserves that were not needed for development projects. Several factors were cited in the policy decision. One was the income differential between oil and gas. In October 1976 the Deputy Managing Director of NIOC stated:

The price of gas at consumption points is calculated on the basis of crude oil with equivalent calorific content, but transportation costs of gas are up to 10 times that of crude due to the requirement of capital intensive pipelines and special tankers. Therefore, Iran will increase its exports only when oil sales fall off and at such a time as new uses for gas drive up its price. Iran would not consider any new agreements for the export of its natural gas although present agreements and commitments will be honored. (U.S. Department of Commerce, 1977, p. 212)

At that time, NIGC also announced that it was cancelling a major LNG project (its biggest export gas contract) with a consortium made up of El Paso Natural Gas Company (U.S.) and Sopex and Distrigaz S.A. (Belgium) for the exploitation, liquefaction, and export of natural gas. This project would have produced 2,000 to 3,000 million cubic feet of liquid natural gas per day from the Pars gas fields located near the port of Bushehr and would have required a total investment of about $5.9 billion (U.S. Department of Commerce, 1977, p. 212). This field is now called North Pars Field, as distinct from South Pars Gas Field, which is shared with Qatar (Mehrvarz, p. 137).

Design and construction. The detailed design and engineering of IGAT-2 was awarded in a $30 million contract to Snamprogetti (Italy)/Sofregaz (France) in June 1976. At the same time NIGC was studying tender proposals for: (1) material procurement and handling; (2) supervision and inspection; and (3) project management (U.S. Department of Commerce, 1977, p. 213; U.S. Embassy, 1976, p. 3).

In March 1978 three construction companies started work on IGAT-2: Saipem of Italy for the 632-km Kangan-Isfahan section, Spie-Capag of France for the 301-km Isfahan-Qom section, and Soyuz-Zafram of the USSR for the 487-km Qom-Astara section (Mehrvarz, p. 346; Kuhn’ p. 231; Širāzi, p. 87).

Interestingly, the Germans had tried at least on two occasions to involve their own companies in handling of the Iranian section of the IGAT-2 project. First, in Moscow in 1975 during contract negotiations, they specifically lobbied for their Mannesmann Construction Company and brought into a meeting the company representative. The presence of this ‘uninvited guest’ was strongly objected to by Mosaddeghi, who asked him to leave (Širāzi, p. 88).

Also, as narrated by Asadallah ‘Alam, the shah’s imperial court minister and his very close confidant, during his briefing with the shah on 15 April 1976 he conveyed the West German ambassador’s requests regarding Leopard tanks and the German-led IGAT-2 European Consortium taking charge of the engineering, procurement, and construction, as well as finance of the Iranian section of the project. The shah told ‘Alam to inform the ambassador that he rejected their tanks offer but would instruct that IGAT-2 execution by the European Consortium be studied (‘Alam, VI, p. 52).

The construction of the pipeline continued with 30 percent progress until December 1978, when it was stopped because of the revolutionary atmosphere of the time. Up to the revolution, 46 billion Rls ($657 million) had been spent on the project (Širāzi, pp. 87-88).

After the victory of the Islamic Revolution in February 1979, the IGAT-2 contract, among other gas export contracts, was cancelled, and subsequently the pipeline construction work was stopped as a result of the Iran-Iraq War (1980-88). After the war, the Kangan-Isfahan section of the pipeline was completed, and then the Isfahan-Qom section, which was put into service for internal consumption. All the pipes used in IGAT-2 were made in Ahvaz Pipe Mills (Mehrvarz, p. 346; Kuhn, p. 231).

The development of the Kangan/Nar gas gathering systems that feed the Kangan (now Fajr-e Jam) Gas Refinery was completed in later years (see below). However, most of the equipment for phase one (processing the relatively sweet gas of the Nar field) were purchased before the revolution and were kept in Bushehr warehouses—some suffering corrosion—until 1985 (see below).

Economics of IGAT-2. According to NIGC analysis, the project’s economic justification was derived as follows:

Based on the contract price (without escalation) of the full capacity exported natural gas Iran would earn 42 billion Rls annually [for export of 14 billion m3/y, and excluding the Czechoslovak off-take volume of about 3 billion m3/y]; while by using 11 billion cubic meters per year inside the country 8 more billion Rls was gained according to the prevailing gas rates. Even more important, 11 billion cubic meters of natural gas would replace 71 million barrels per day (bpd) of oil that was worth 60 billion Rls in the prevailing prices at the time. On top of all this, Iran would save the investment for annual refining of 70 million barrels of oil that was equivalent to a 200,000 bpd refinery. (Širāzi, p. 88)

6. OTHER PLANS AND ACHIEVEMENTS

Kangan (Fajr-e Jam) Gas Refinery (phases 1 and 2). This refinery was designed and constructed in two phases to treat (sweeten) the sour gases received from Nar and Kangan gas fields located 300 km to the southeast of Bushehr and 200 km to the south of Shiraz near the shores of the Persian Gulf. In this plant the gas coming out of the raw gas wells was separated from both water and gas condensate in the field, and then gas and condensate were transferred by separate pipelines to the plant for further gas/condensate separation and stabilization. The next steps in the plant operation were gas sweetening and dehydration, NGL extraction, and its fractionation into propane, butane, and pentane. The sweetened lean dry gas was to supply the gas needed for the IGAT-2 pipeline, and the condensates were sent via pipeline to the nearby Taheri (Siraf) port for export (NIGC, 2014b, p. 14).

These separate fields together being 60 km long and 6 km wide, were discovered in 1973 by the EGOCO consortium of the European companies, led by the French state-owned Entreprise de recherches et d'activités pétrolières (ERAP), which held a 32-percent share (Mehrvarz, p. 336; U.S. Embassy, 1976, p. 5).

The first phase of the Kangan Refinery, which had a design capacity of 38 million cubic meters per day (14 billion m3/y) and used feed from the relatively sweet Nar gas field with 260 billion cubic meters recoverable gas reserves, was designed by the British branch of the American Parsons company; its construction was by Daelim of South Korea. Both firms had left Iran by the mid-1980s.

The Iranian engineering and construction companies under NIGC management and with reduced support by the Korean company, which lost several of its staff during Iraqi bombings, succeeded under very harsh conditions to complete and inaugurate the plant during 1983-90. The gas gathering and compression from the field to the refinery was offered for tender and was completed parallel with the phase one refinery. An airport and a residential town for the plant employees and their families were constructed near the refinery (Mehrvarz, p. 413; ʿArāqi interviews: Ṣāleḥiforuz, pp. 128-30, and Kerāčiān, pp. 85-87).

The Kangan phase of the refinery with a design capacity of 42 million cubic meters per day (15 billion m3/y), using 460 billion cubic meters of recoverable Kangan field highly sour gas, was again designed by the UK Parsons. The detail engineering, procurement, and construction of it, along with the related gas gathering systems, was carried out in the post Iran-Iraq War years and was inaugurated in 1995 (Mehrvarz, p. 413).

After 2010 in order to provide enough feed and to compensate for pressure drop of the Kangan/Nar gas fields, part of the sour gas of South Pars phases 6-7-8 was delivered to this refinery by the IGAT-5 trunkline, and its gas production capacity was increased to 125 million m3/day, while producing 38,000 bpd (barrels per day) of condensate and 200 ton/day of LPG (NIGC, 2014b, p. 14).

Khangiran (Sarakhs) gas field development and gas supply to Mashhad and Neka power plant. The first explorations in Khangiran (Ḵāngirān) gas field, 30 km to the west of Sarakhs city in the northeast corner of Iran near the Turkmenistan border, dates back to 1952. The first well reaching the sweet cap gas reserves of Shourijeh (Šuriča) formation (layer), with estimated reserves of about 100 billion cubic meters, dates back to 1962. The gas dehydration (dewatering) plant for receiving this sweet gas started operation in 1973 and provided 35 million ft3/day (about 1 million m3/day) of natural gas to Mashhad by a 120-km, 16-inch diameter pipeline. This amounted to a small part of Mashhad industrial (mainly two nearby cement and sugar mills), commercial, and home needs (Khangiran; Nāmeh-ye ṣanʿat-e naft, Tir 1352 Š./June 1973, pp. 4, 6, 8, 9, 28).