INDUSTRIALIZATION

ii. The Mohammad Reza Shah Period, 1953-79

Industrialization in Iran in the postwar period evolved in three distinct phases. These are: 1953-59, known as the semi-liberal phase; the short period of 1960-62, which was beset by crisis and recession; and finally the one and half decades between 1963 and 1979, which witnessed the longest period of sustained industrial accumulation in Iran (see ECONOMY ix.).

THE SEMI-LIBERAL PHASE

After the 1953 coup (q.v.) and the resumption of concessionary oil agreements in 1954, revenues from the oil sector grew at an unprecedented pace: during the five year period of 1956-60, government oil revenues amounted to $1,228,000,000 compared to only $483,000,000 during the entire thirty-six years between 1913 and 1949. Foreign capital (in the form of official aid and grants), too, began to flow to Iran during the 1953-60 period. Aid from the U.S. government alone amounted to more than $890,000,000 at this time (Bharier, 1971, p. 119). Available data suggests that those new external resources were immediately translated into government expenditure, and they had a highly expansionary impact on the economy. One such effect was the rise in the General Cost of Living Index, which rose by 65.1 percent between 1953 and 1960 (Bank Markazi Iran, 1964).

Public sector investment in this period started from a very slender base but soon witnessed an annual growth rate of 25 percent in real terms. According to the development expenditure data from the Plan Organization, more than 68 percent of government investment went into economic infrastructure, which was mainly composed of transportation and water. Allocations for water went mainly into bulky investments on three dams, which were not completed until the mid-1960s. More than 90 percent of the government expenditure on transport and communications went into the construction of inter-city roads and railways and the expansion of ports, which principally facilitated the connection between main urban centers and foreign trade ports. Such large-scale projects were also favored by foreign consultants and contractors; in the absence of any indigenous know-how, they were mainly in charge of the planning and implementation of the projects (Mahdavy, 1970; Plan Organization, 1964). The only field in which government investment directly contributed to expanding productive capabilities in a significant way was the manufacturing sector. More than 77 percent of government direct investment in the manufacturing sector was allocated either to traditional light industries, such as textiles and sugar, or to cement. The latter was to cater for the needs of the massive construction projects of the government, and the former two industries were to substitute for imports, which by the mid-1950s constituted a large share of supplies in these industries. The concentration of government investment in large infrastructural projects laid the foundations for the rapid and sustained, manufacturing-led industrialization Iran would see, but the projects’ long gestation lags played a not insignificant role in intensifying the inflationary pressures and balance of payments disequilibrium in the latter half of the 1950s.

At the same time as an increase in the government’s resources and expenditure, a spurt in private investment was occurring: the private sector’s share of fixed investment as a proportion of GDP (Gross Domestic Product) doubled between 1955 and 1960, overtaking public investment in 1958. Before 1955, foreign manufacturing enterprises were practically non-existent in Iran; the enactment in November 1955 of the Law for the Attraction and Protection of Foreign Investment presented a landmark for the inflow of foreign capital into the Iranian economy. The main provisions of the 1955 law were as follows: (a) to set up a board to examine proposals by foreign investors, which would report its decisions to the Council of Ministers; (b) to give legal protection to imported capital and accord it equal status with private domestic capital; (c) to guarantee repatriation of profits and in the case of nationalization to provide for compensation (Nowshirvani and Bildner, 1973).

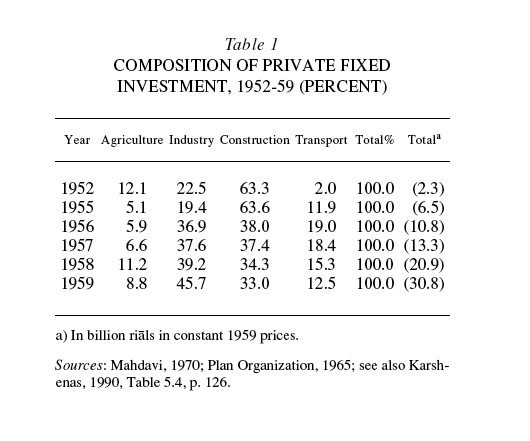

Table 1 shows that between 1952 and 1955, growth of private investment was more biased toward construction and transportation, which increased their share from 65.3 percent to 75.5 percent at the expense of industrial and, in particular, agricultural investment. After 1956, however, with the appearance of government industrial finance provisions there was a sharp reversal in this process, whereby the industrial sector increased its share from 19.4 percent in 1956 to 45.7 percent in 1959, and construction witnessed a drastic decline of almost 30 percent in its share. About 80 percent of industrial loans went into food processing, textiles, and construction material industries, in which the market conditions and technological possibilities open to Iranian industrialists were conducive to rapid growth of modern, mechanized factories. Modern cotton textiles, sugar, and cement factories were the principal absorbers of private investment. The rest of the funds were distributed in the form of small loans amongst numerous small- to medium-sized producers in various manufacturing activities (Benedick, 1964, chaps. 10-11; Plan Organization, 1964; Baldwin, 1967, chap. 6).

{kind=link}

The 1953-59 was a period of mutual support between the newly established authoritarian regime of the shah and the traditional propertied classes, namely the coalition of landlords, merchant bourgeoisie of the bazaar, and factions of the high clergy. The semi-liberal trade and industrial policies of the government ushered in a period of rapid inflows of external resources and were highly beneficial to this traditional coalition. Nevertheless, they led to severe imbalances in the economy, which brought about the crisis of the early 1960s.

CRISIS AND RECESSION

The 1955-59 boom was followed by the economic recession, which did not fully abate until mid-1963. Though the recession was triggered by the 1960-61 balance of payments crisis, and other deflationary measures taken by the government to stabilize the foreign exchange situation, the period signified adjustment processes of important long-term consequences. The balance of payments crisis was caused by the over-expansion of commodity imports during the boom up to 1959, with heavy reliance on foreign borrowing. During the three years of 1958-60 there was a cumulative drain on foreign exchange reserves of more than $210,000,000 (Baldwin, 1967).

By 1960, the share of oil revenues allocated to development expenditure had declined to 49 percent, significantly down from the 80-90 percent envisaged in the Second Plan law. Accordingly, a high degree of utilization of domestic and, in particular, foreign borrowing had to be made to finance the massive investment program of the government at the time. Free access to foreign and domestic borrowing had allowed various government ministries and agencies, including the Plan Organization, to initiate new investment projects independently from each other and in an uncoordinated manner. At the micro-economic level, this flurry of undirected investment led to several instances of duplication and waste (Plan Organization, 1965), while at the macro-economic level it contributed to the severe internal and external imbalances which appeared in the economy towards the close of the 1950s. Despite the duplication and waste evident from having separately organized but overlapping investment projects and businesses, a mission from the International Bank for Reconstruction and Development (IBRD) could find little evidence of overstaffing or inefficiency at actual factory level in state plants vis-à-vis private industry (in 1960, ninety-eight factories were wholly or partially state-owned, in spite of the fact that during the semi-liberal period, the government had taken steps to offer its factories for sale to the private sector; Bharier, 1971; IBRD, 1963). It was not until the foreign exchange situation attained crisis proportions—when in September 1960 the country was left with foreign exchange reserves barely sufficient to finance one or two weeks’ value of essential imports—that the government was forced to take action through the introduction of an IMF-prescribed stabilization program.

During the last two years of the government’s Second Seven-Year Plan (1961-62), no new investment projects were initiated by the government, and real private investment dropped by more than 16 percent. Since the bulk of imports consisted of final consumer products and investment goods, the slowdown in the pace of investment and restrictions over luxury consumer goods’ imports appeared as the only practical means of averting the foreign exchange crisis. The impact of these measures on the growth of output in the industrial sector, which as yet did not heavily depend on imported inputs, was minimal: real output in manufacturing and mining, relying on the expanded capacity during the recent investment boom, continued to grow by an annual rate of 11 percent over the 1960-62 period. From the point of view of domestic economic activity, it was the construction sector and domestic trade and related services such as transportation which were most adversely affected.

The stabilization program was officially terminated in March 1962. One important area of restructuring that followed this period was the increasingly direct intervention by the state aimed at the industrial sector. This involved directing private and public investment into new lines of manufacturing production, which were in greater conformity with the structure of domestic demand. In this way, the groundwork for a new phase of the import-substitution method of industrial accumulation was being laid.

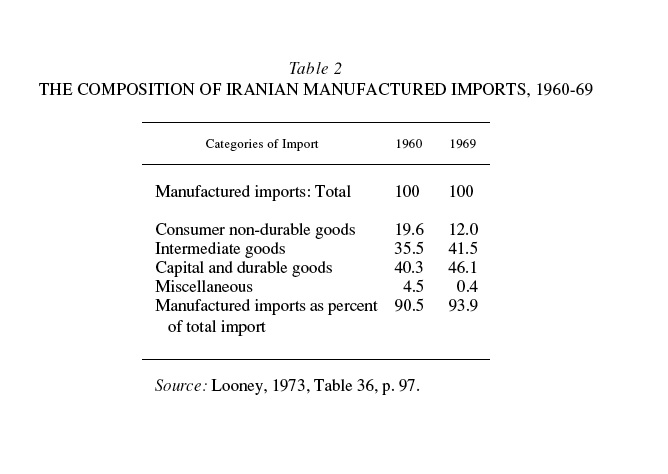

The change in the composition of Iranian imports can be seen in Table 2 below. This shows a greater emphasis on intermediate goods, and capital and durable goods also rising in prominence, in Iran’s imports by the end of the 1960s (Plan Organization, 1964, 1965).

{kind=link}

SUSTAINED INDUSTRIAL ACCUMULATION (1963-78)

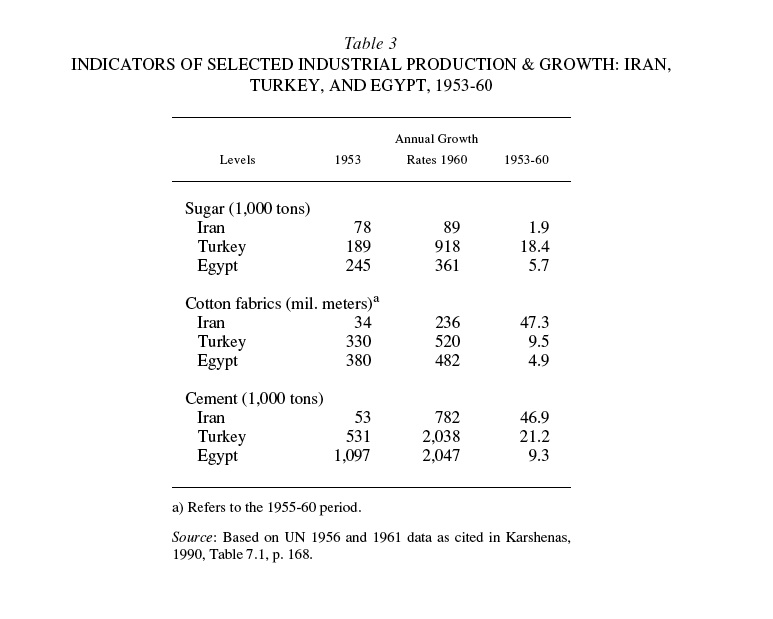

The various elements which contributed to the industrialization strategy of the government after the recession of the early 1960s were gradually shaping up. The rapid diversification of demand for industrial products during the 1950s, combined with the sluggish growth of new domestic industries due to the liberal trade policy of the government, had created an immense gap between the structure of domestic demand and supply for industrial products. In a few traditional industries, relatively high growth rates were achieved during the 1950s, though even in these old, established industries production capacity in the early 1960s was still very limited. Table 3 draws a comparative picture of the performance of selected branches of Iranian industry over the 1950s with two other Middle Eastern countries of comparable size, namely Egypt and Turkey. As the table shows, despite the impressive growth rates in certain industries in Iran during the 1950s, by 1960 the level of production even in the old, established industries, such as cotton fabrics and cement, was only between 30 and 50 percent of the other two countries.

{kind=link}

The apparent backwardness of Iranian industry even by regional Middle Eastern standards may to some extent explain the vigorous industrialization drive which was initiated by the government in the post-recessionary period. This happened mainly through massive public sector investment and a high degree of reliance on foreign capital to renovate the industrial base. The recession of the early 1960s, which was the culmination of the chaotic and uncoordinated growth of the economy during the previous decade, acted as a catalyst in shaping the new import-substituting industrialization drive by the government. Given the infancy of Iranian industry in the early 1960s, an initial phase of industrialization based on a protected home market appeared inevitable. This, it was hoped, would allow the buildup of necessary industrial skills and know-how for a later stage of export-led industrialization. Politically also, the government would have favored the import-substituting industrialization strategy, as it was bound to show impressive results at least in the medium term, while at the same time accommodating a relatively high wage and salary policy.

The import restrictions and high tariffs which were imposed during the balance of payments crisis of the early 1960s induced the growth of a host of new industries catering to the highly protected and rapidly expanding home market. The availability of cheap finance and ample supplies of labor and foreign exchange made a relatively long period of sustained and rapid industrial accumulation possible. This new phase of industrialization was characterized by important changes in the structure of both public and private investment.

A distinct feature of the structural shift in the government’s development expenditure in the post-1963 era was an increasing concentration of government investment in the industrial sector and related activities. The share of government investment allocated to the industrial and energy sectors grew from about 16 percent to 41 percent between the Second (1956-62) and Fifth (1973-77) Plan periods. Over the same period, the share of physical infrastructure, such as transport and communications, and water and agriculture, declined from 71.0 percent to 28.1 percent. The growing direct involvement of the state in industrial production in the post-1963 period was accompanied by a clearer definition of the public and private spheres of industrial investment. Government investment was confined to heavy industries such as basic metals, exploration and exploitation of natural resources (apart from oil) that were vital to the domestic industries (such as copper), mechanical engineering, chemicals, and petrochemicals, which were beyond the investment capacity of the private industrialists. The share of government investment allocated to traditional light industries fell from 77.3 percent during the 1956-62 period to 3.8 percent by the Fifth Plan period, while the share allocated to heavy industry over the same period grew from 5.7 percent to 80.0 percent (Table 4).

{kind=link}

The role of the state as the supplier of heavy industrial goods in this new phase of industrialization opened up new areas of government investment and led to a rapid acceleration in the pace of public sector investment. Real gross fixed investment in the public sector grew by an average annual rate of 22 percent over the 1963-77 period, surpassing, by 1967, the level of private investment. Such rates of growth were fueled by the rapid increase in oil revenues of the government. The possibilities of financing government investment through domestic resource mobilization, either by taxation or other forms of government intervention, were not instrumental in determining the size of the government’s development expenditure. It was rather the availability of external finance, namely oil revenues and foreign credits, which determined the magnitude of government investment. Since foreign credits were by and large a function of expected future oil revenues, the latter became the main determinant of planned investment.

The rapid growth of government investment over this period produced a strong impetus for private investment, both from the demand and the supply sides. On the demand side, it contributed to the rapid expansion of the home market, both directly and indirectly through the multiplier effect. The fact that government investment was mainly financed by external resources substantially increased its domestic multiplier impact. Private investors were encouraged to increase their investment with the highly buoyant conditions of demand and the availability of resources for investment, namely labor, foreign exchange, and capital. On the supply side also the growth of government development expenditure contributed to the profitability of private investment through direct cost reduction and other indirect, positive externalities. Government investment in infrastructure such as transport, communications, energy, and irrigation, and its development expenditure on social overheads such as education and health, had obvious positive effects in this respect. Even government investment in heavy industry was conducive to the growth of private investment on the supply side through its positive externalities (e.g., on-the-job training of labor, diffusion of new technology, etc.).

Such complementary and dynamic interactions between public and private investment were particularly strong in Iran with its ample supply of labor and substantial possibilities for increasing the productivity of labor through the introduction of advanced technology at the time. Moreover, externally financing government investment ruled out the possibility of financial “crowding out” of private domestic investment.

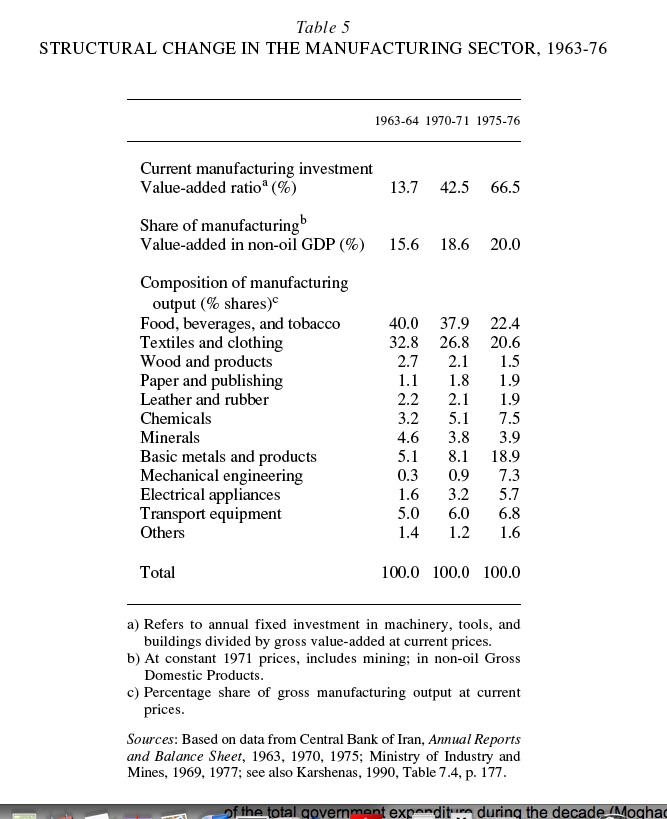

There is little reliable data on the structure of private investment over this period, but the available evidence indicates that a relatively large part of private investment was channeled into new import-substituting industries, which together with government industrial investment gave rise to a rapid change in industrial structure. Private sector fixed investment in the manufacturing sector is estimated to have had an annual rate of growth of about 14 percent in real terms over the 1965-77 period, accounting for about 60 percent of total investment in the sector over the period as a whole (Bank Markazi Iran, 1965-77). The availability of external finance, channeled through the industrial banks and the Plan Organization, contributed to a rapid acceleration in the rate of manufacturing investment over this period. As Table 5 shows, the rate of investment in the manufacturing sector increased from about 14 percent of manufacturing value-added in the early 1960s to over 65 percent by the mid-1970s. If one considers that the investment figures in the table do not include working capital investments, these figures indicate extremely high investment rates, which clearly could not have been sustained without the contribution of external funds. In particular during the oil-boom years of the early 1970s, when due to the overheating of the economy there was a spurt of speculative activity similar to that of the late 1950s, the channeling of funds through the specialized banks and the Plan Organization played a crucial role in accelerating the rate of manufacturing investment.

{kind=link}

The high rates of capital formation in the manufacturing sector brought about a rapid change in the structure of production. As is shown in Table 5 (above), manufacturing production in the mid-1960s was dominated by the light consumer goods industries such as food, textiles, clothing, and wood products, which accounted for more than 75 percent of total output. By 1976, however, the manufacturing sector had achieved a much higher degree of diversification, with the new consumer durables, intermediate, and capital goods industries claiming about 50 percent of total output.

Government investment in heavy industry made an important contribution to structural change in intermediate and capital goods industries, while the private sector contributed to the diversification of the industrial structure by investing in consumer goods branches and in particular in the new consumer durable goods. The government played a major role in determining the overall size and pattern of private industrial investment by controlling, for instance, the size of industrial credits, or by operating an industrial licensing policy, which effectively closed several sectors to new investors. This was especially true in the earlier parts of the period. However, the pattern of investment in the private manufacturing sector was ultimately left to the profit motives of the individual industrialists. There was no conscious policy to direct private investment into selected industries through a selective application of government import protection policy or of the numerous subsidies which it granted to the private investors. Protection from competitive imports was granted across the board for all the major products in the final consumer market. The pattern of investment in the private manufacturing sector thus became crucially dependent on the growth and structure of domestic consumer demand.

There were, however, other important structural changes, taking place through the introduction of new products and technology within each branch of the manufacturing sector, which are not reflected in the overall sectoral composition of output shown in Table 5. An important aspect of structural change in the manufacturing sector concerned the size composition of establishments and the nature of the new technology embodied in the manufacturing investment in this period. A striking feature of Iranian manufacturing in this period was its extreme duality. As Table 6 shows, in the mid-1960s Iranian manufacturing, in terms of employment, was dominated by small artisan workshops, which on average barely employed more than one wage laborer each. More than 65 percent of the entire manufacturing labor force in the urban areas was employed in these small workshops with extremely low labor productivity and wages (Ministry of Labor, 1964). The growth of output in this small subsector mainly took place in the form of duplication of workshops with similar conditions of production and the same level of labor productivity. The really dynamic manufacturing enterprises, which absorbed almost all of the new investments and generated the structural changes, fell within the large-scale manufacturing subsector. As Table 6 (above) shows, in 1964 this large-scale subsector employed 34 percent of the urban manufacturing labor force and produced 56 percent of the value-added.

{kind=link}

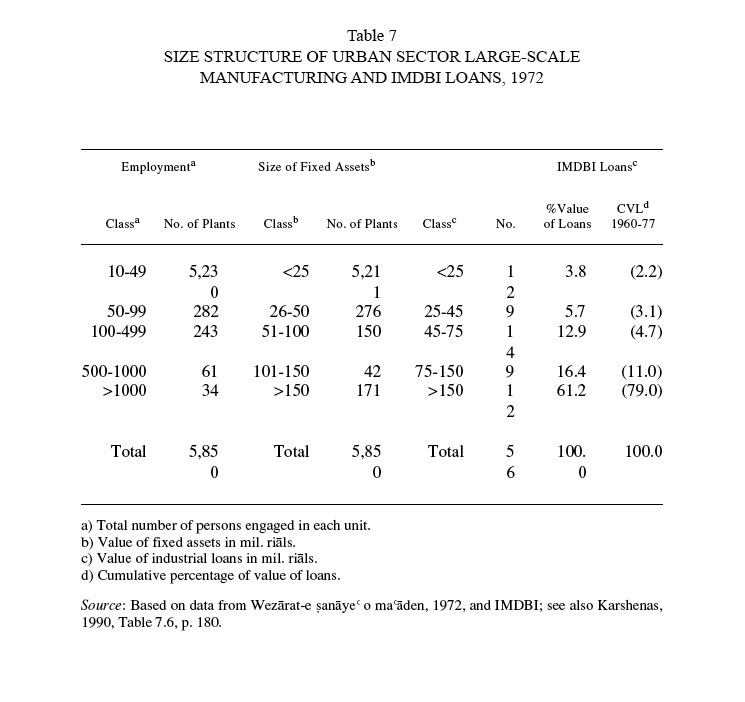

A more detailed differentiation of “large-scale” manufacturing is necessary for a better understanding of the nature of accumulation and technological change in the subsector over this period. Table 7 gives a breakdown of the large-scale manufacturing sector according to the number of persons employed and the size of the fixed assets, and compares it with the size of industrial loans granted by the Industrial and Mining Development Bank of Iran (IMDBI, the first private industrial credit bank in Iran established in 1959; Baldwin, 1967; Benedick, 1966). The IMDBI loans constituted more than 70 percent of the total long-term industrial credits granted to the private sector over the 1963-77 period. As Table 7 shows, about 90 percent of large-scale manufacturing establishments fell within the lowest bracket, employing between ten to fifty workers and with fixed assets of less than 25 mil. riāls in value. This group, however, received only 2.2 percent of the value of IMDBI loans over the 1960-77 period. More than 95 percent of the IMDBI’s lending over this period went to a relatively small number of large factories, which comprised the modern, “corporate” manufacturing sector, employing more than fifty workers and with a capitalization of above 25 million riāls each. This corporate sector formed the dynamic core of Iranian manufacturing, which absorbed the major share of manufacturing investment and was the main beneficiary of the preferential credit, foreign trade, and fiscal policies of the government over this period.

{kind=link}

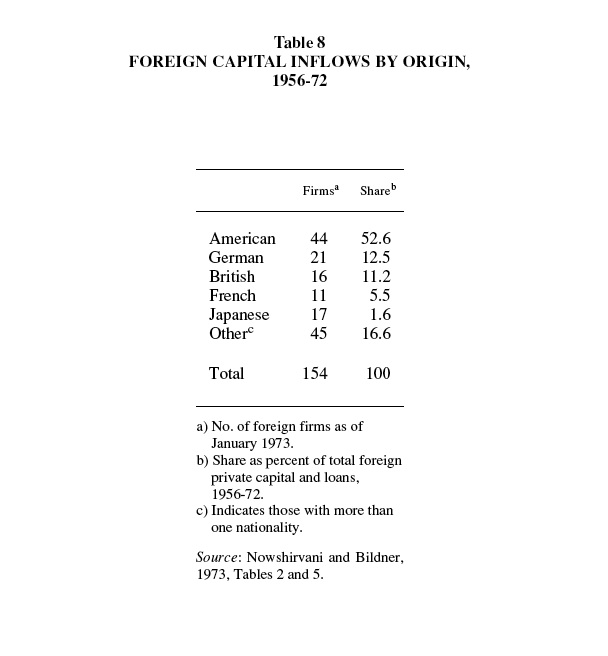

These years also saw a steady rise in foreign capital inflows into Iran’s economy. The aforementioned 1955 Law for the Attraction and Protection of Foreign Investment was an important stimulus in this respect. Table 8 exhibits the number of foreign firms by origin and their share of total foreign private capital (plus loans) to Iran for the periods specified. According to this table, U.S. companies had by far the largest share, followed by German, British, and French corporations (the same picture emerges from an examination of the number of foreign firms by origin). The share of Japanese investment was low, but in actual fact grew quickly through the period from a low starting base. Government policies aiming at the expansion and growth of manufacturing industry were, undoubtedly, a major factor explaining the growth of foreign capital inflows, and in this respect the protection granted to these industries was an outstanding example. A study by the World Bank found that, on average, rates of custom duties in 1970 were 4.8 times their level in 1960. In addition, a whole host of import restriction and quotas were imposed during this period, and by 1970 about 70 percent of the value of goods produced in Iran was protected by quantitative restrictions, which often meant outright prohibition of imports (IBRD, 1971). The influx of foreign capital thus went hand in hand with increasingly protective policies of the government towards industry.

{kind=link}

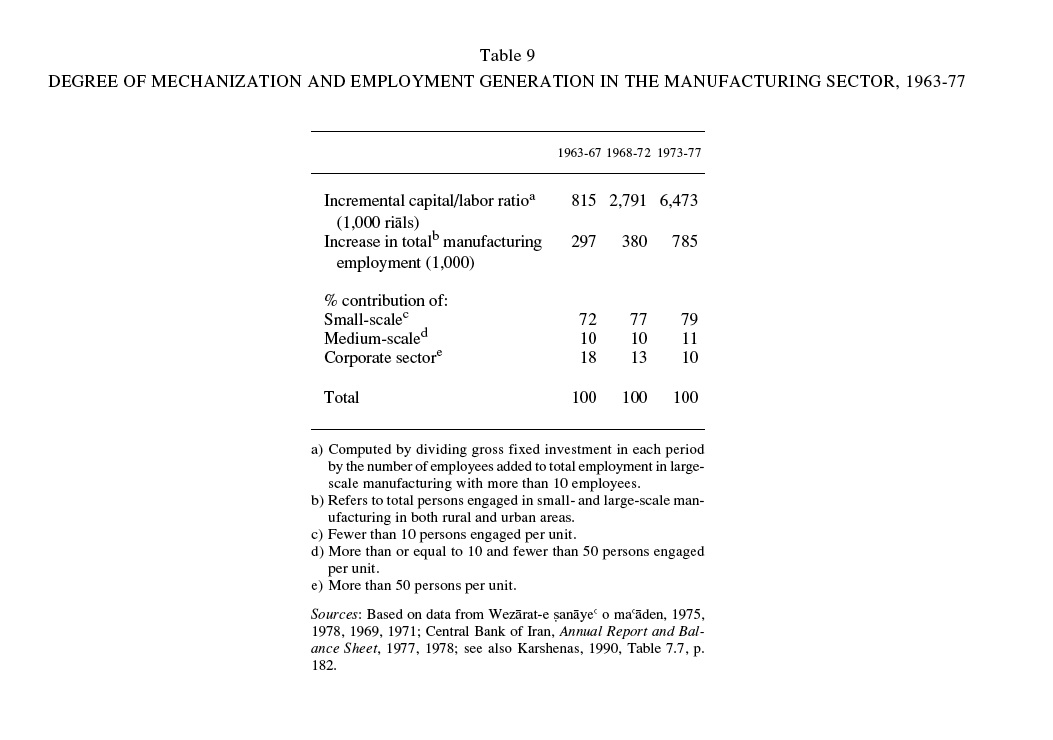

While the availability of abundant supplies of cheap credit and foreign exchange created the conditions for rapid accumulation and technological change in the corporate sector, at the same time it encouraged an increasing degree of mechanization of the manufacturing sector, exacerbating the duality within the sector. There was a seven-fold increase in the incremental capital/labor ratio of manufacturing investment between 1963 and 1977 (Table 9), a trend that was particularly intensified during the Fifth Plan period (1973-77). This was a period of severe shortages of skilled labor brought about by an over-expansion of investment activity and leading many firms to resort to increasing automation.

{kind=link}

The modern corporate manufacturing sector exhibited impressive growth rates in terms of output, productivity, and employment (Table 9, above). The extremely high rates of growth of output allowed a rapid expansion of employment to take place—by about 7 to 8 percent per annum—despite the relatively high rates of growth of labor productivity. High labor productivity growth rates in turn allowed a rapid increase in real wages, which grew by about 4 percent per annum over the 1960s and accelerated to the extremely high rate of 11 percent per annum over the 1970s, in line with productivity growth. The modern corporate sector, however, embraced only a very narrow section of manufacturing employment. Despite the relatively high rates of employment growth in the corporate sector, because of its narrow base its contribution to the increase in manufacturing employment was relatively low. As Table 9 shows, the contribution of the corporate sector to the increase in manufacturing employment declined from 18 percent over the 1963-67 period to 13 percent during 1968-72, and to merely 10 percent during 1973-77. Throughout the 1960s and 1970s, it was the small-scale manufacturing subsector which absorbed the bulk of the new entrants into the labor market. These numbers multiplied rapidly due to high rates of population growth and transfer of surplus agricultural labor through rural-urban migration (Hakimian, 1990). The contribution of small-scale manufacturing to the expansion of manufacturing employment increased from 72 percent during the 1963-67 period to 79 percent over 1973-77 (Table 9).

A notable aspect of the process of industrialization was that the 5,000 or so medium-sized firms (with 10-50 employees) contributed no more than nine percent to employment generation in the sector throughout the period (Table 10). The combination of desirable features such as labor intensity in production together with reasonable levels of labor productivity in these medium-sized firms made them ideal for generating some productive and gainful employment in a labor surplus economy like Iran. There were, however, various aspects of the industrial policy of the government which militated against the growth of the medium-sized manufacturing subsector. Firstly, the medium-sized firms were deprived of long-term subsidized finance, as almost the entire supply of long-term credits by the specialized banks was absorbed by very large-scale enterprises. Secondly, the government provided no technical assistance to the medium-sized firms. The Industrial Development and Renovation Organization (IDRO)—a government organization which was officially charged with the task of providing technical assistance to industry—effectively acted only as a mediator between the very large-scale domestic enterprises and the multinational companies in establishing joint ventures and licensing agreements (IDRO, 1974, 1975). Thirdly, the medium-sized firms had slender ties with the large-scale enterprises, either directly through subcontracting or indirectly through market-mediated, backward or forward linkages. The large-scale enterprises in the corporate sector formed technological enclaves within the manufacturing sector, depending for their raw material supplies and technology largely on imports. This not only prevented the large-scale enterprises from acting as a vehicle for the diffusion of modern technology into the rest of the manufacturing sector, but also prevented the generation of demand for the rest of the sector through inter-industry linkages. Finally, and related to this point, the growth of the medium-sized sector may have been handicapped due to the competition in the final product market from the highly subsidized and technologically dynamic corporate manufacturing sector.

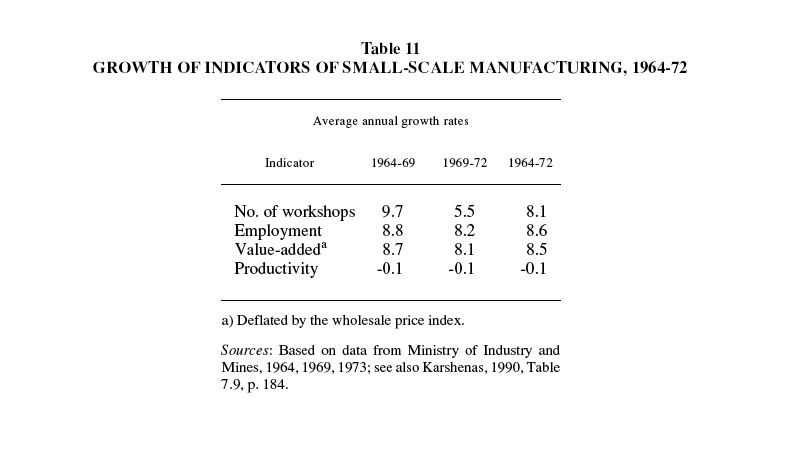

Under these circumstances it fell upon the small-scale workshops (fewer than five employees) to provide the bulk of the new employment in the manufacturing sector. Ease of entry into this subsector and the possibility of work sharing through increasing employment of family labor made it a repository for labor supply which could not find employment in the large-scale modern manufacturing sector. The growth of this small-scale or informal manufacturing subsector therefore assumed an “extensive” character—in the sense that it took the form of multiplication of the small workshops without major changes in their technology of production and productivity of labor. As is shown in Table 11, employment in the small-scale manufacturing sector grew pari passu with output and the number of workshops, with productivity of labor remaining stagnant. This is in sharp contrast to the “intensive” character of growth in the technologically dynamic corporate sector, which was characterized by rapid growth of labor productivity and real incomes. As long as there existed surplus labor in the economy, growth in the informal sector would be expected to continue, with its output growing with more or less the same pace as real incomes in the urban economy.

{kind=link}

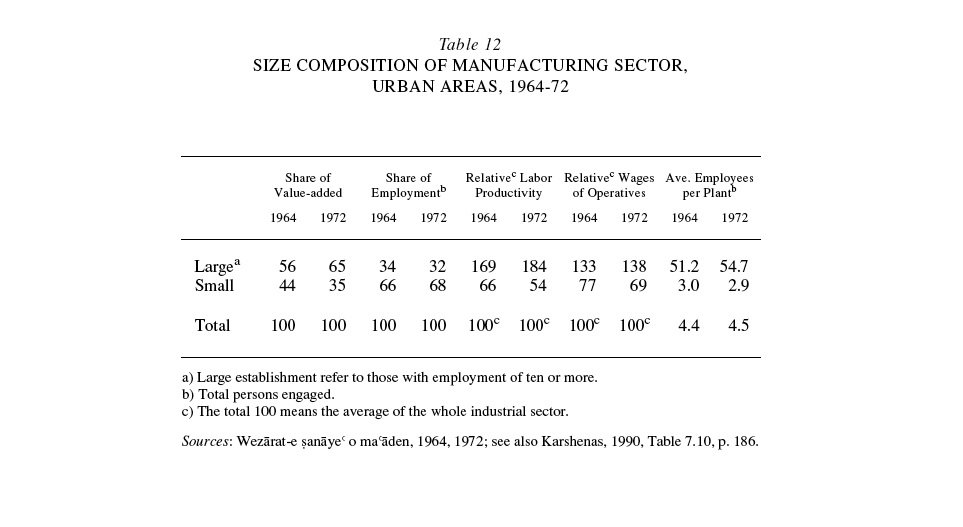

Table 12 shows how the process of industrialization intensified the duality within the manufacturing sector. This was manifested by the widening gap between productivity and wages in the small-scale or informal manufacturing, and the rest of the sector. Increasing share of employment in the former signified, on the one hand, the fact that over the 1970s a general shortage of labor could have hardly been a constraint to industrial growth. If anything, the problem as it presented itself in 1972 was how to generate sufficient employment in the economy in step with the growth in the supply of labor. What appeared as a general shortage of labor during the 1974-76 period, however, was a short-term phenomenon which occurred as a result of the abrupt and extremely large expansion in investment activity during the oil-boom years. On the other hand, the growing industrial duality was an indication of the fact that the income gains from productivity growth were concentrated in the hands of a small section of the population consisting of the industrialists and workers in the corporate manufacturing sector. The growing concentration of income in turn reinforced the prevailing pattern of structural change in the industrial sector by expanding the market for new products, in particular the new durable consumer goods, which originated in the rapid growth and diversification of consumer demand among high income groups.

{kind=link}

OVERALL ASSESSMENT

Following the semi-liberal phase of 1953-59 and the inherent imbalances that arose during that period, a significant restructuring and rethinking of the process of industrialization in Iran was required, and the recession of 1960-62 provided that opportunity. Along with this shift towards an import-substitution strategy, various favorable factors on both the supply side and demand side contributed to bringing about the rapid process of industrialization over the period 1963-78. The abundant supply of foreign exchange proceeds from the fast growth of oil exports helped to finance the imports of capital goods and raw materials necessary for sustained industrial accumulation. The channeling of sizeable volumes of funds through industrial banks ensured the availability of large concentrations of money capital to enable private industrialists to take advantage of the vast investment opportunities provided by the protected home market. This was complemented by direct government investment of a large part of the oil revenues in heavy industry. On the demand side also, the high rates of growth of government expenditure, largely financed by oil revenues, led to a rapid expansion of the domestic market which helped to sustain the momentum of industrial investment throughout this period.

Despite the lessons of the boom of the late 1950s and the ensuing crisis in the early 1960s, the industrialization strategy that followed until 1978 exhibited major weaknesses too. The same factors which contributed to the rapid process of industrial accumulation, namely the abundant supply of foreign exchange and external funds, also led to a neglect of certain aspects of the industrialization process that impinged on the eventual sustainability of the development process itself. The shortsighted policy stances adopted regarding the structural aspects of industrial growth gave rise to a process of “perverse growth” with serious questions over its viability over the long run, and subject to sharp cyclical fluctuations in the medium run. Heavy reliance on capital-intensive technology in the modern manufacturing sector, and a lack of an adequate technology policy by the government aimed at a more widespread diffusion of benefits of advanced technology, led to a growing concentration of industrial employment in low-productivity and technologically stagnant sectors. A heavy degree of geographical concentration of industrial output could also be observed, with the Central Province of Iran (Tehran and the provincial towns) being greatly favored: in 1972, the Ministry of Industry and Mines attributed 55 percent of industrial value-added to the Central Province, while in terms of employment, 36.2 percent of the total number of industrial workers were employed in this region (Ministry of Industry and Mines, 1973; Avramovic, 1970; Bharier, 1971; Looney, 1973). The industrial credit policy for the government, which showed a near-total neglect for the small- and medium-sized firms, also exacerbated this problem by stifling any initiatives which may have originated in the private sector in this regard. It was believed that the fast rate of growth of the modern sector would be adequate to gradually absorb the labor force engaged in the low-productivity sector. With the high rates of population growth and fast rates of rural-urban migration, however, this assumption proved wrong; concomitant with the widening duality in the manufacturing sector, the share of employment in the low-productivity sector also increased. Given the import substitution strategy of the government and the fact that various lines of manufacturing were still at relatively early stages of their development, low magnitudes of non-oil exports at the beginning of the 1963-78 period were not surprising. In later stages of import substitution industrialization, when the manufacturing sector achieves the necessary maturity to compete in the international markets, export ratios can rise rapidly. However, with the continuation of non-oil export trends over the period under investigation here, the long-term viability of the growth path after the exhaustion of oil resources was under question. Though in the long run the success of the import substitution strategy depends on the ability to export, the medium-term viability of the strategy depended on the possibility to bring about the necessary adjustment in the import ratios. These adjustments were not made in Iran in the period prior to the 1979 Revolution.

Bibliography

Dragoslav Avramovic, “Industrialization of Iran: the Records, the Problems and the Prospects,” Tahqiqat-e Eqteṣādi (Quarterly Journal of Economic Research), Tehran, Spring 1970, pp. 14-47.

George B. Baldwin, Planning and Development in Iran, Baltimore, 1967.

R. E. Benedick, Industrial Finance in Iran, A Study of Financial Practice in an Under-developed Economy, Cambridge, Mass., 1964.

Julian Bharier, Economic Development in Iran 1900-70, London, 1971.

Bank Markazi Iran (Central Bank of Iran), Annual Report and Balance Sheet, Tehran, various issues, 1963 to 1978.

Bank Markazi Iran, Quarterly Bulletin, Tehran, various issues. Hassan Hakimian, Labour Transfer and Economic Development, Hemel Hempstead, U.K., and Boulder, Colo., 1990.

Industrial and Mining Development Bank of Iran, Annual Report, Tehran, 1972.

Industrial Development and Renovation Organization (IDRO), Annual Report, Tehran, 1974, 1975.

International Bank for Reconstruction and Development (IBRD), Industrial Policies and Priorities: Iran IV, Washington, D.C., 1971.

Idem, The Development of Iran—an Appraisal (a monograph), Washington, D.C., 1963.

Massoud Karshenas, Oil, State and Industrialization in Iran, Cambridge, 1990.

Hossein Mahdavy, “The Patterns and Problems of Economic Development in Rentier States: The Case of Iran,” in M. A. Cook, ed., Studies in the Economic History of the Middle East, London, 1970, pp. 428–67.

Robert E. Looney, The Economic Development of Iran, New York, 1973.

Vahid F. Nowshirvani and R. Bildner, “Direct Foreign Investment in the Non-oil Sectors of the Iranian Economy,” Iranian Studies 4/2-3, Spring/Summer 1973, pp. 66-109.

Plan and Budget Organization of Iran (PO), Report on the Implementation of the Second Seven-Year Plan, Tehran, 1964.

Idem, Outline of the Third Plan: 1962-67, Tehran, 1965.

UN, “Economic Development in the Middle East, 1955-56,” World Economic Survey, Washington, D.C., 1956.

Idem, “Economic Development in the Middle East, 1956-61,” in World Economic Survey, Washington D.C., 1961.

Wezārat-e eqteṣād (Ministry of economy), Tawseʿa-ye ṣanʿati-e Irān (Industrial development of Iran), Tehran, 1967.

Wezārat-e kār o omur-e ejtemāʿi (Ministry of labor and social affairs), Sāl-nāme-ye āmārhā-ye ešteḡāl VII (Yearbook of Employment Statistics), Tehran, 1964.

Wezārat-e ṣanāyeʿ o maʿāden (Ministry of industry and mines), Āmārhā-ye ṣanʿati-e Irān (Iranian industrial statistics), Tehran, 1964, 1969, 1971-73.

Idem, Ravand-e zamāni-e tawlidāt-e ṣanʿati-e Irān (Time trends of Iranian industrial products), Tehran, 1977.

Idem, Ravand-e āmārhā-ye ṣanʿati o bāzargāni (Trends in industrial and commercial statistics), Tehran, 1975 and 1976.

Idem, Ravand-e tawlidāt-e ṣanʿati-e Irān (Trends in Iranian industrial production), Tehran, 1978.